Pete Hudson is one of the OGs of digital health. As an emergency room doc he was fed up with his friends bothering him with their medical problems and he created a tool called iTriage, which helped patients figure out what condition they had, and where to go to deal with it. This was fifteen years ago and we’re now starting to see the evolution of that. Pete is now a venture capitalist and an investor in Transcarent–the sponsor of a new video series on THCB. We had a long conversation about the evolution of digital health, what went right, what opportunities got missed, and what to expect next. This is part one of our conversation, and allows two guys who were there close to the start of this world to survey what’s happened since–Matthew Holt

Can Someone Actually Be Responsible?

By MATTHEW HOLT

I was having a fight on Twitter this week and it hit me. America 2024 is Japan 1989.

The topic of the fight was right-wing VC Peter Thiel. In 2001 he put a ton of Paypal stock allegedly worth less than $2,000 into a Roth IRA. The Roth IRA was designed so that working stiffs could put post tax cash into an IRA, grow it slowly and take out money tax-free. (For traditional IRAs you put in pre-tax money and get taxed when you take it out). You may have read the story in ProPublica. Magically Thiel earned less that year than the max allowable income limit (around $100K) to contribute to a Roth IRA, and magically that stock was within weeks worth much more and then, later, hundreds of millions more. Since then Thiel has invested those Paypal returns in Facebook, Palantir and much more, and that Roth IRA has billions of dollars in it that can never be taxed.

My twitter adversary was saying that Thiel obeyed the law. I doubt it, but that’s not really the point. When the Roth was introduced it wasn’t meant to be a loophole that Silicon Valley types could use to hide billions from tax. But neither my twitter “friend” nor Peter Thiel want to take responsibility or pay their fair share.

Japan in 1989 was wealthy and successful and heading off a speculative cliff which it’s since taken 3 decades to dig out of. There were numerous academics pointing this out, but the most interesting analysis was The Enigma of Japanese Power written by a Dutch journalist named Karel van Wolferen. Here’s a summary from wikipedia with my emphasis added

Van Wolferen creates an image of a state where a complicated political-corporate relationship retards progress, and where the citizens forgo the social rights enjoyed in other developed countries out of a collective fear of foreign domination….Japanese power is described as being held by a loose group of unaccountable elites who operate behind the scenes. Because this power is loosely held, those who wield it escape responsibility for the consequences when things go wrong as there is no one who can be held accountable.

In Thiel’s case a collective network of tax accountants, junk philosophers, and purchased politicians like JD Vance ensure that no one has to be accountable. Ultimately Thiel doesn’t feel responsible for paying what he owes. Of course the exposure of Trump’s tax cheating shows that he doesn’t either. And many people find this OK.

Meanwhile I got into it a little with Jeff Goldsmith on last week’s THCB Gang about why hospitals are still paid per transaction when it would be much better for them to be paid some kind of global budget for the services they provide and for doctors to be paid a salary to exercise their best judgment rather than be tempted into providing care just because they get paid for it. Both COVID and the recent Change Healthcare outage put health care providers in a terrible situation financially because they depend on being paid fee-for-service via claims for individual transactions. Did the leadership of America’s hospitals and doctors come out asking for a change to the system? No, they just got a government hand out and begged for a return to standard operating procedure. No one can rationally look at how we pay for health care in America and say “give us more of the same” but there’s no leadership to change it at all.

Talking about lack of leadership, Amber Thurman died in Piedmont Henry Hospital because no-one on the medical team was prepared to give her the D&C that she desperately needed. They were scared of going to jail under Georgia’s draconian anti-abortion law. There are many, many guilty parties here.

Continue reading…What will Harris mean for Health Care? – Not much

By MATTHEW HOLT

The Democratic convention wrapped with a fine speech from Kamala Harris, star power from the Obamas and Clintons, and a bunch of Republicans telling their ideological brethren that it was better to be a Democrat than a Trumper. More importantly no Beyonce/Taylor Swift duet–as we were promised by Mitt Romney.

There was a lot of talk about some aspects of health care. But overall if Harris wins, don’t expect much change to the current health care system.

Why not?

First there’s the pure politics. The Dems need to win back the House (probable but not certain) and hold the Senate to pass legislation. Right now they have a 51-49 edge in the Senate. Most likely that goes to 50-50 as the Republicans will definitely pick up Joe Manchin’s seat in West Virginia. There’s a series of seats the Dems currently hold in close races (Montana, Ohio, MIchigan, Nevada, Arizona) that they’ll need to keep to maintain it at 50-50, and it’s hard to see any pickups from Republicans (perhaps Florida or Texas if you squint really hard). The good news is that Manchin (WV) and Sinema (AZ) will soon both be gone, so the Dems that will be there won’t be as difficult to persuade to follow a Presidential agenda. But that will still leave Walz as VP to do what Harris did and pass a bunch of deciding votes under reconciliation, which massively limits what the legislation can do–it has to be “budget related.”

Which leads us to what we have been hearing from Harris and her campaign about health care? We’ve heard a lot about issues that have impacts on health, specifically creating affordable housing and fighting child poverty, but little that is directly related to health care itself. Really only two issues stand out. Abortion and reproductive rights, and drug prices.

Clearly Harris will take a swing at reversing Dobbs and passing a national right to abortion. This will need either a packing of the Supreme Court (my favorite) or ending the filibuster or both. Either of these will be incredibly tough to pull off constitutionally and politically and will take huge amounts of political oxygen. Of course the cynics would say, the Democrats are better off leaving this as an issue to use to beat up the Republicans on. But if it gets done, womens’ and reproductive rights will only be back where they were in 2022.

Regarding the cost of drugs, there will continue to be much justified bashing of big pharma, but the extension of insulin price controls is something that (eventually) the market via CivicaRX and others is getting to anyway. Meanwhile the IRA gave Medicare the right to negotiate drug prices and the results are not exactly earth shattering. For example, CMS says it’s negotiated the cost of blood thinner Eliquis from about $6,000 a year to under $3,000 This sounds good until you realize that the price is only that high because of patent games the manufacturer BMS plays in the US, and the price in the rest of the world is under $1,000. We’ll hear more about this as the price cuts come into effect, (although not till 2026!) and more drugs get negotiated, but overall this isn’t exactly an earth-shattering change.

Finally there’s already a guaranteed fight about extending the premium subsidies for ACA plans. These were first in the pandemic American Rescue Act, then extended in the IRA, but they currently are scheduled to end in 2025. It’s hard to imagine them not being extended further whatever the makeup of the Senate, assuming a Democratic House of Representatives. (A Marjorie Taylor Greene speakership does give me pause!). But again there’s nothing new here and the overall flavor of expensive premiums and high deductibles in the current ACA marketplace won’t change.

So what’s not going to happen? Virtually all the interesting stuff we were promised by Harris and for that matter Biden in 2020. You may have missed the one actual “policy-first” speech at the convention which came from Bernie Sanders. To be fair a lot of his agenda was already in the Biden legislation. That was no accident as Biden deliberately reached out to him in 2020 and 2021 and enacted a pretty radical agenda on infrastructure, climate, industrial policy and more. And when I say radical I mean milquetoast social democrat by European standards! But what wasn’t in that agenda? No Medicare for all, which Bernie ran on in 2019/20 and brought up again at the convention. Who else proposed that in 2019? Why, a certain Kamala Harris. That never made it into the Biden agenda. We didn’t even get legislation introduced about lowering the Medicare age to 60, which was a campaign promise. There’s been no conversation about any of this from Harris or from Biden before he withdrew. It’s just a bridge too far.

Which leads to the stuff that gets debated about in THCB and elsewhere as to how the system actually works. There’s been nothing about Medicaid expansion (or its continued contraction). No talk about reining in hospital consolidation. No mention even of insurers gaming Medicare Advantage or private equity buying up physician practices. Nothing about the expansion of value-based care.

What we can expect in a Harris administration is more of the same from CMS and potentially a slightly more aggressive FTC. That will mean continued efforts to veer slightly away from fee-for-service in Medicare, a few more constraints on the worst behavior in Medicare Advantage, and possibly some warning shots from the FTC about hospital monopolies. But the trends we’ve seen in recent years will largely continue. We’re not getting a primary-care based capitated system emerging from the wreckage of what we have now, and unlike the Clinton and even Obama administrations, there’s not even any rhetoric from Harris or Biden about how that would be a good idea.

So politically I don’t think the Harris administration will be very exciting for health care. And if the other guy wins, as Jeff Goldsmith wrote on THCB last month, expect even less.

Phil Fasano, Recuro Health

Phil Fasano is CEO of Recuro Health. Phil was CIO at Kaiser Permanente in the glory years when it rolled out Epic/Health Connect, which was at the time the biggest roll out of an EMR and was instrumental in creating Kaiser’s system of virtual care. A decade+ later the concept of telehealth and virtual care has been battered around, notably in the stock price of Teladoc and others. However, Phil is now leading a smaller organization called Recuro Health which is delivering extensive primary hybrid care to small & medium employers, has more then 1 million lives on the system, and is profitable. Is this the future of digital health? Maybe, and it’s well worth listening to his approach–Matthew Holt

Non-profit health systems driving income inequality

If you follow along with my rantings on THCB, Twitter and Linkedin you’ll know that I am unhappy with America’s growing inequality, both in wealth and income. Now, there are a few signs that so long as we have full employment the income picture for the lowest paid is getting a little better. But wealth inequality is clearly not getting better.

You may remember this video explaining wealth inequality. Worth a watch if you haven’t seen it.

Well that was made in 2011. Back then Elon Musk was barely a billionaire, and more than a decade of massive stock market appreciation later, we know that the rich have gotten a lot richer, and their taxes went down following the Trump tax cuts in 2017.

Meanwhile, something similar has been going on in health care. The health economy has amazingly not taken much more of the overall economy since 2010. It went from 13% to 17% of GDP between 2000 and 2010 but has amazingly stayed around there–only popping up during the Covid recession and then heading down again. But the amount of money flowing into health care has stayed at a constant rate. And the American people continue to hate their experience with the health system.

They’re aren’t many selfless heroes. Payers, providers, doctors, pharma, equipment suppliers are all doing well. Wendell Potter has continued to show how health insurance companies have consolidated and gotten richer over the past decade plus. Big Pharma has managed the translation away from the mass market blockbusters of the 1990s to the high priced niche drugs of today, and now with GLP-1s is managing to keep those high prices. Despite lots of whining by the AHA, hospitals–which got massive handouts from the CARES Act during Covid–are all doing well again. But it’s always good to check in with the big non-profit systems. This isn’t the first time I’ve written about this. Early this year in a larger rant I wrote:

Over the last 30 years America’s venerable community and parochial hospitals merged into large health systems, mostly to be able to stick it to insurers and employers on price. Blake Madden put out a chart of 91 health systems with more than $1bn in revenue this week and there are about 22 with over $10bn in revenue and a bunch more above $5bn. You don’t need me to remind you that many of those systems are guilty with extreme prejudice of monopolistic price gouging, screwing over their clinicians, suing poor people, managing huge hedge funds, and paying dozens of executives like they’re playing for the soon to be ex-Oakland A’s. A few got LA Dodgers’ style money.

One of the things that the non-profits have to do is file the 990 form with the IRS. Among other things it shows how much money the organization’s executives make. Now it’s not like non-profit health system execs are the only ones coining it. In 2022 the biggest for-profit chain HCA’s CEO made $20m and 4 others there made over $5m. But at least HCA is a nakedly capitalist organization, and it pays taxes.

Recently one of the bigger hospital systems, UPMC put out a new 990. Unlike the previous version they put out, the 990 on their website is a photocopy that can’t be searched. Maybe that’s an accident, although any non-profit can put out an easily searchable document. For instance here’s the one from a teeny non-profit that I control. You can search the words “Reportable Compensation” and find that sadly I got paid zilch for my efforts. Not sure why UPMC can’t do the same.

Luckily for those of us who care, Propublica is a little more aggressive. They reproduced a searchable version. The way ProPublica did it was to download an xls from the IRS. One reason it’s worth looking at was that this year as opposed to 2022, UMPC didn’t post its compensation in $$ order.

I’m not knocking UPMC too much. Very few other big non-profit health systems put anything like as much effort into detailing who makes what amount on their 990s. They usually stop after the first 10-20 employees. UPMC goes down to 220+

So I copied and repasted the compensation information from ProPublica and did the necessary editing of 230 cells to be able to sort by compensation. You can find the spreadsheet here. (Feel free to copy & paste and do your own edits).

So what does it tell you?

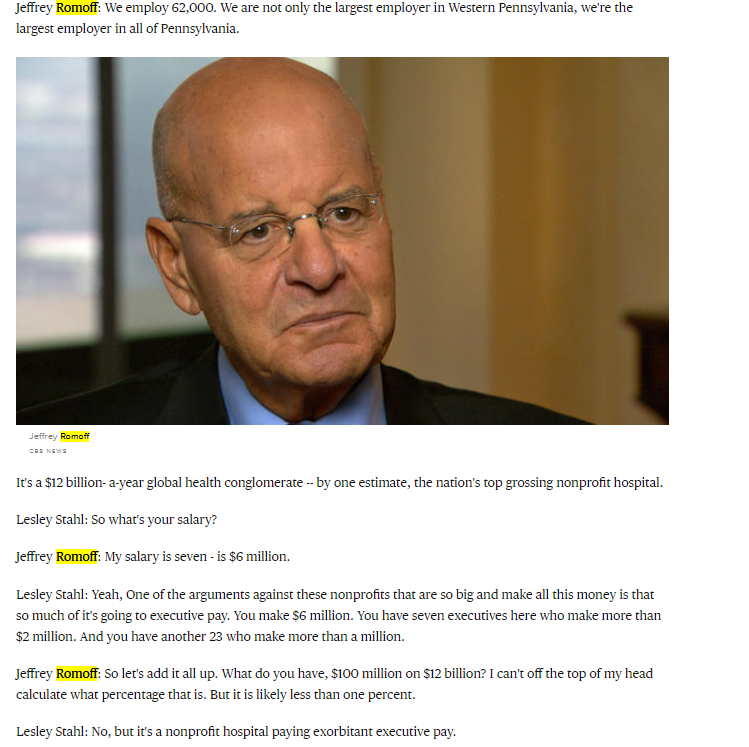

UPMC had a CEO called Jeffrey Romoff who worked there his whole career. Romoff became President in the 1990s and took over as CEO in 2006. Using aggressive M&A, and some very sharp elbows including against the unions, Romoff essentially created the massive local monopoly that is the modern UPMC. His biggest moment in the national spotlight was when he went on 60 Minutes in 2011 and forgot his salary (he said it was $7m but then corrected it to $6m). Ten years later Romoff’s salary was a tad under $13m. If you are wondering, the median annual wage in the US in 2011 was $34,460. By 2022 it was $45,760. So the average salary increased 34% in nominal terms over that time. Romoff’s went up by more than 100%.

But that’s all well and good. Romoff retired at the age of 75 in August 2021 and was replaced by Leslie Davis.

So for the period covering July 2022 to June 2023, who was the highest paid person at UPMC?

Continue reading…Digital Health: There is No Exit

By MATTHEW HOLT

All of a sudden we are back in 2021.

You digital health fans remember that halcyon time. In 2019 a few digital health companies went public, and then somehow got conflated in the pandemic meme stock boom, with the harbinger event being the August 2020 sale of Livongo to Teladoc that valued it at $19bn and early in 2021 rather more, as Teladoc itself got to a market cap of $44bn in February 2021

Venture money poured into digital health as a fin de siecle for the ZIRP, that had been going for a decade, combined with the idea that Covid meant we would never leave our houses. The vaccine that became generally available at the start of the Biden Administration in 2021 put paid to the idea that telehealth was the majority of the future of care delivery.

Nonetheless between mid 2021 and early 2022 Jess DaMassa and I were reporting on VC funding in a show called Health in 2 Point 00 (later Health Tech Deals) and every week there were several deals for $100m and up going into new health tech companies.

Things don’t look so pretty now. Even while venture money was flooding into digital health, those public companies, as exemplified by Teladoc, started to see their stock price fall. While it was actually a good year for the stock market overall, in 2021 the digital health sector fell by around 60%. It kept going down. 2022 was worse and although one or two individual companies have recovered (Hi Oscar!), nearly two years later the market cap of the entire sector remains in the toilet.

Of the list that I’ve been following for years there’s only 11 broadly defined digital health companies with a market cap of more than $1 billion–that is only 11 public unicorns

What’s worse is that only one company on that list is decently profitable, and that’s Doximity. It made over $170m profit on revenue of less than $500m last year and trades at 10 x revenue. But Doximity always was profitable, going way back to 2014 (long before its IPO), and although it’s doing cool stuff with AI and telehealth, it’s basically an advertising platform for pharma.

There is no such thing as a profitable public digital health company in the mainstream of care delivery or even insurance–unless of course you count Optum. Which means there’s almost certainly no profitable VC-backed private company either.

Which leads me to this month. You remember those huge rounds that Jess & I used to report on and make fun of? They’re back.

I get it. The stock market is hot and all those pension funds are trying to put their winnings from Nvidia somewhere. VC looks a reasonable bet and there have been a few tech IPOs. If you squint really hard, as STAT’s Mario Aguilar did, you can pretend that Waystar & Tempus are health tech IPOs, although a payments/RCM company and a diagnostics company which are both losing a ton of money wouldn’t give me confidence as an investor.

But the amounts being thrown around must give anyone pause. Let’s take a few examples from the last month. Now these aren’t a knock on these companies, which I’m sure are doing great work, but let’s look at the math.

Digital front door chatbot K-Health raised at a $900m valuation. This round was a $50m top-up but it has raised nearly $400m. It says it’ll be profitable in 2025, and has Elevance as its biggest client. Harmonycares is a housecall medical group, presumably pursuing the strategy that Signify and others followed. It raised $200m, so presumably has a $500m+ valuation–Centene bought an earlier version of the company for $200m a decade ago and sold it to some investors two years back. Headway is a mental health provider network that uses tools to get providers on their system and markets them to insurers. It raised $200m at a reported $2.3bn valuation.

You can look at that list of public companies, including ones taken private like Sharecare, and see that there are lots of telehealth chatbots, medical groups and mental health companies on the list. Any of which probably have similar technology buried inside them. I’m sure if you shook Sharecare hard enough all those technologies would fall out given the number of companies it acquired over its decade plus of expansion.

But let’s take mental health.

Amwell acquired a mental health company called Silvercloud, and a chatbot called Conversa. Its market cap is bouncing around between $250m & $350m and it has more than that in cash–which means the company itself is worth nothing! The VCs who put money into K-Health and Headway could literally could have bought Amwell for about what they invested for a fraction of those companies. Is Headway doing more than the $250m a year in revenue Amwell is putting up? Headway’s value is nearly 6 x the value of Talkspace which is bringing in about $150m a year in revenue. And if you consider BetterHelp to be 50% of Teladoc — which it roughly is — Headway is 3 x the value of BetterHelp which is doing $1bn a year in revenue. Is there any chance that Headway is doing close to those numbers? Maybe somone who saw the latest pitch deck can let me know, but I highly doubt it.

Now of course these new investments could be creating new technology or new business models which the previous generation of digital health companies couldn’t figure out. They might also have figured out how to grow profitably–although as far as I know Doximity stands alone as a profitable company that took VC funding it never needed and never used.

But isn’t it more likely that they are in the market competing with the public companies and those private companies that got funding in 2020-22, have similar pitches, similar tech and are similarly losing money?

I am a long time proponent of digital health and really hope that technology can change the sclerotic health care sector. I want all these companies to do well and change the world. Maybe those VCs investing in those mega rounds are more sensible than they were in 2022. But given the state of the digital health sector on the current stock market–which is otherwise at all time highs–I just don’t know what the exit can be, and it pains me to say it.

Blue Shield CA, CVS Caremark & the mystery of the extra $116, with 2 UPDATES (at the end)

By MATTHEW HOLT

Today we’re going to have fun with show and tell. I’m going to show you how a little corner of American health care is making my life as a consumer worse and more expensive–hopefully someone can tell me why.

The cast members are: me, my MD, the (sort of) independent pharmacy that delivers, Alto, and my insurer Blue Shield of California and its PBM CVS Caremark, which also owns a mail order pharmacy.

The brief backstory: For some years my doctor has been whining about my high cholesterol, and a few years back I went on a statin called Rosuvastatin Calcium. Older readers may remember Jean Luc Picard himself advertising the branded version Crestor, but it’s been off patent for about a decade. About 50 million Americans now take a statin, almost all of them a generic, including many 60 year old males like me. My cholesterol has come down, but my MD told me it could come down more, so a few months ago we boosted the dose to 40mg from 20mg.

Until recently I’d been insured by BCBS Massachusetts, and you might recall a little over a year ago I wrote a piece on THCB about the fun and games to be had trying to figure out what their PBM (CVS Caremark) was doing with the pricing of my kid’s ADHD medication. But they’d never messed with my medication as my statins are cheap. At least I thought they were. In fact as recently as April last year, they were free. You can see the price from the delivery from Alto Pharmacy below.

How BCBS Mass came up with $0.00 as the price I pay I don’t know, but presumably they think it’s a good thing to have me on statins in the hope I don’t have an (expensive) heart attack instead.

Then for some reason my price for the statin later the same year went up to $23. No longer $0 but at $8 a month not really worth making a fuss about.

At the end of the year, COBRA expired and I went to buy insurance on the California exchange. And in order to keep access to my family’s doctors at One Medical, I chose the only plan they were in, the Blue Shield of California HMO.

My next 90 day supply was the first one which went from 20mg to 40mg, but it’s still a common generic. Blue Shield of California also uses CVS Caremark (although it’s been talking a good game of ditching CVS Caremark and setting up its own PBM) and the cost at Alto barely budged. Now it was $28.

What happened next: So all was going normally until late last week when my next 90 supply was delivered. Except it wasn’t. Alto delivered me a 30 day supply and charged me $19.

Continue reading…Want to get rich in health care? Ditch the startup and run a hospital

By MATTHEW HOLT

Given that I ran a health technology conference for many years, I tend to run in a circle of people who have some ambition to get rich in health care. After all, billions of dollars of VC money have been dropped in lots of startups over the last decade, and a few prime examples have done very well. For example Jeff Tangey of Doximity, Glen Tullman of Livongo, Chaim Indig of Phressia and many others did fine when their companies IPOed in the late 2010s. But the truth is that many, many more have either started a health tech business that didn’t make it, or were foot soldiers in others that died along the way (Olive, Babylon, Pear, etc, etc). Which has been leading me lately to thinking about whether that’s the right approach to take if you want to make money in health care. Hint: it’s not.

There’s still tremendously little transparency about which health care organizations have what amount of money and what people earn. There is though one sector that by law has to publish information about revenue, profits, investments and executive compensation. That is the non-profit hospital/health system sector. Nonprofits are required to file Form 990 with the IRS that has that information and more on it. Having said that, most hospitals are frequently late in filing them, and file them in a very confusing way. The wonderful journalism organization ProPublica maintains a database of all 990 filings and it’s instructive to look around in it.

Some health systems make it relatively easy. UPMC, the huge western PA conglomerate files one 990 for the whole group. Others, not so much. I know that Providence, the huge west coast system, has overall revenue of $28bn but only because Fierce Healthcare told me. Had I tried to piece that together from its 990s, I’d have started with its Washington filing ($6bn), moved on to its Oregon filing (~$5bn) and then started getting confused..

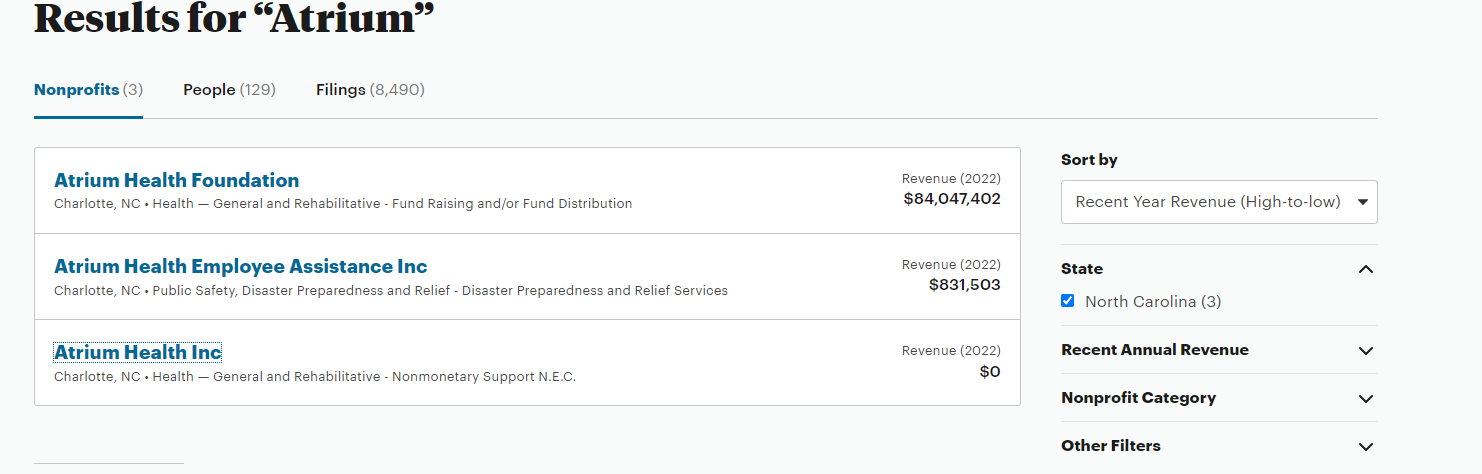

Let’s say you wanted to easily figure out Advocate, the system that was the merger of the huge midwestern system with Atrium, the North Carolina-based one. Good luck. You can find Advocate but Atrium’s seems to be missing. Ditto for Carolinas Health, its previous name. There is a page calling itself Financial Information on the Atrium website, but it doesn’t have any, and tells you to go to a website set up for municipal bondholders. In fact I couldn’t find any evidence of the IRS auditing any large system, or fining them for non-compliance in filing.

The good news is that last year the North Carolina State Employees plan, i.e. a pissed off purchaser, dug into all the N. Carolina hospital systems and found out that Atrium’s CEO pay went up nearly five-fold over six years. But even the state had real trouble finding out the truth:

“It is important to understand that these figures are significant underestimates for three reasons. First, a legal loophole denies the public the right to see how much publicly owned hospitals reported paying their top executives on their tax filings. This failure of oversight hides the tax filings of more than three in 10 nonprofit hospitals in North Carolina, including Atrium and UNC Health. UNC Health did not answer a public records request for executive compensation data until February 13, 2023, two days before this report’s publication and almost three months after its receipt of the request. UNC Health’s system wide data is therefore not included in this report.”

So the very top dogs are doing well. At UPMC it turns out that seven made more than $3m including the CEO Jeff Romoff –the same one who forgot on 60 Minutes whether he made $6m or $7m. Turns out he didn’t have to remember that number for long as by 2021 he was making $12m.

But the munificence is spreading down the executive ladder. To demonstrate, let me introduce you to Tracey Beiriger Esq. There’s almost no information about Tracey on Linkedin or anywhere else on Google other than it appears he or she is an IP lawyer at UPMC. So why do I bring them up?

Because in 2021–the last year for which UPMC filed a 990 –Tracey was the 118th highest paid executive at UPMC and had the misfortune to only make $499,446.

Which means that 117 executives working at UPMC made more than $500,000. It’s a little tricky figuring out the similar numbers at Providence because of the multiple 990s in 2021 but there are 38 in Washington (not including CEO Rod Hochman who made $9m in 2020 and then vanished from the 2021 990!), 18 in Oregon and another 21 in Southern California. So call it 80+.

I bring this up because $500,000 is a pretty decent individual income. When I asked ChatGPT it estimated about 1.2 million Americans earned that much or more. Given the workforce is 167m, that puts those several hundred hospital execs way into the top 1%.

Now I have no objection to people earning good money. I’m sure they have all worked very hard for it. But if you look at these organizations, they do not seem to be spreading the wealth very far.

Last year UPMC was accused by unions of suppressing staff wages. There is yet to be an outcome from that complaint to the DOJ, but last week there was one from a formal class action complaint about Providence shortchanging employees by rounding down their pay to the nearest half-hour, even though they were clocking on and off by the minute. Providence was fined $200m which probably isn’t much split between 33,000 employees but at least indicates that their senior management acts just like any other aggressive business in terms of cutting costs on the backs of their employees. And it’s not just their employees. They also just got fined $137m for aggressively suing patients.

Which leads me to two final points.

The first is, is it more likely you’ll make that $500K+ in a hospital system or in a tech startup? Blake Madden at Hospitology has been tracking systems that have more than $1bn in revenue. He’s found 113 so far. Second bottom of the list is Atlanticare in NJ, which has 16 execs making more than $500K. Which by my wild guess means that the average system has about 50 employees making $500k+ which rounds up to something like 5,000 hospital execs making at least $500K and many of them are making a whole lot more.

Compare that to a successful health tech startup that actually makes it. Take Phreesia, a VC-backed start-up that went public in 2019 having started way back in 2007. (I know the year because CEO Chaim Indig launched at Health 2.0 in 2008. He was nice enough to let me buy some stock at the IPO and I made a few bucks). Chaim made $300K the year it went public and as CEO of a public company that’s bounced around at being worth between $1Bn and $4Bn, he made $750K last year. No one else made more than $500K. Now yes, he owned 4% of the company at the IPO and got awarded more stock. He is doing very well, but the point is that there were dozens of companies launching at Health 2.0 in 2008 and the vast majority don’t get close to an IPO or making any money for the founders, let alone the staff.

My conclusion is, it’s not a rational bet to go the health tech route if instead you can find a regional hospital chain and brown-nose your way up into the exec ranks!

The second point is more fundamental. Remember UPMC and its 117 execs making $500K+? What would a comparable government agency be paying out? I looked at the state of California salaries.There look to be about 50 state employees making more than $500k a year, almost all working for the state investment fund CALPERS. But the top paying one only makes $1.6m a year. I’m not saying that CALPERS should be paying out that much even if it is competing with Wall Street, after all members of the Senate only make $205,000 a year and the state could just put the whole pension into an S&P index fund. But what I am saying is that we should be thinking about paying our big non-profit systems similarly to government employees because they essentially are government employees.

Beckers posted UPMC’s payor mix last year. I highly suspect you’ll find something similar at almost every big system.

- Medicare 48%

- Medicaid 17%

- UPMC as Insurer 11%–(60% of whom are Medicaid/Medicare patients)

- Commercial, Self Pay, Other 24%

More than 70% of the money comes from the government, and the rest from the suckers who have to buy their insurance on the “open market”–which includes those buying via the ACA exchange, receiving government subsidies, and government employees.

So while these huge systems act like Fortune 100 companies and reward their executives accordingly, almost all the money comes from the taxpayer.

I wish I could say we are getting good value for it.

And yes, I didn’t even mention the for-profits and the big insurers, but that will have to wait for another day….

Matthew Holt is the founder & publisher of THCB

What Walmart said & What Walmart Did: Not the same thing

Walmart surprised us all and changed its mind about primary care yesterday. It’s out.

Because so few people have seen it I want to show what Walmart‘s head of health care said just 18 months ago (Nov 2022). Today they are finally killing off the 6th different strategy they’ve had (maybe it was 4). I guess (unlike CVS & Walgreens) they don’t have to write down investment in Oak Street or VillageCare, but they never worked out that primary care is only profitable if it’s 1) very low overhead 2) a loss leader for more expensive services (as most hospitals run it) or 3) getting a cut of the $$ for stopping more expensive services (Oak Street, Chenmed, Kaiser).

At HLTH 18 months ago I interviewed Cheryl Pegus who was then running Walmart and I asked why anyone should trust them, given how often they changed. Sachin H. Jain, MD, MBA Jain answered for her and said, “because they have Cheryl!” — Cheryl then said, “at Walmart the commitment to delivering health care is bigger than anywhere I have ever worked”. “Right now I have 35 centers in 3 years I’ll have 100s” see 11.00 onwards in the video below, although the whole thing is worth a look

Cheryl though left Walmart THE NEXT WEEK!

What’s behind all these assessments of digital health?

By MATTHEW HOLT

A decent amount of time in recent weeks has been spent hashing out the conflict over data. Who can access it? Who can use it for what? What do the new AI tools and analytics capabilities allow us to do? Of course the idea is that this is all about using data to improve patient care. Anyone who is anybody, from John Halamka at the Mayo Clinic down to the two guys with a dog in a garage building clinical workflows on ChatGPT, thinks they can improve the patient experience and improve outcomes at lower cost using AI.

But if we look at the recent changes to patient care, especially those brought on by digital health companies founded over the past decade and a half, the answer isn’t so clear. Several of those companies, whether they are trying to reinvent primary care (Oak, Iora, One Medical) or change the nature of diabetes care (Livongo, Vida, Virta et al) have now had decent numbers of users, and their impact is starting to be assessed.

There’s becoming a cottage industry of organizations looking at these interventions. Of course the companies concerned have their own studies, In some cases, several years worth. Their logic always goes something like “XY% of patients used our solution, most of them like it, and after they use it hospital admissions and ER visits go down, and clinical metrics get better”. But organizations like the Validation Institute, ICER, RAND and more recently the Peterson Health Technology Institute, have declared themselves neutral arbiters, and started conducting studies or meta-analyses of their own. (FD: I was for a brief period on the advisory board of the Validation Institute). In general the answers are that digital health solutions ain’t all they’re cracked up to be.

There is of course a longer history here. Since the 1970s policy wonks have been trying to figure out if new technologies in health care were cost effective. The discipline is called health technology assessment and even has its own journal and society, at a meeting of which in 1996 I gave a keynote about the impact of the internet on health care. I finished my talk by telling them that the internet would have little impact on health care and was mostly used for downloading clips of color videos and that I was going to show them one. I think the audience was relieved when I pulled up a video of Alan Shearer scoring for England against the Netherlands in Euro 96 rather than certain other videos the Internet was used for then (and now)!

But the point is that, particularly in the US, assessment of the cost effectiveness of new tech in health care has been a sideline. So much so that when the Congressional Office of Technology Assessment was closed by Gingrich’s Republicans in 1995, barely anyone noticed. In general, we’ve done clinical trials that were supposed to show if drugs worked, but we have never really bothered figuring out if they worked any better than drugs we already had, or if they were worth the vast increase in costs that tended to come with them. That doesn’t seem to be stopping Ozempic making Denmark rich.

Likewise, new surgical procedures get introduced and trialed long before anyone figures out if systematically we should be doing them or not. My favorite tale here is of general surgeon Eddie Jo Riddick who discovered some French surgeons doing laparoscopic gallbladder removal in the 1980s, and imported it to the US. He traveled around the country charging a pretty penny to teach other surgeons how to do it (and how to bill more for it than the standard open surgery technique). It’s not like there was some big NIH funded study behind this. Instead an entrepreneurial surgeon changed an entire very common procedure in under five years. The end of the story was that Riddick made so much money teaching surgeons how to do the “lap chole” that he retired and became a country & western singer.

Similarly in his very entertaining video, Eric Bricker points out that we do more than double the amount of imaging than is common in European countries. Back in 2008 Shannon Brownlee spent a good bit of her great book Overtreated explaining how the rate of imaging skyrocketed while there was no improvement in our diagnosis or outcomes rates. Shannon by the way declared defeat and also got out of health care, although she’s a potter not a country singer.

You can look at virtually any aspect of health care and find ineffective uses of technology that don’t appear to be cost effective, and yet they are widespread and paid for.

So why are the knives out for digital health specifically?

And they are out. ICER helped kill the digital therapeutics movement by declaring several solutions for opiod use disorder ineffective, and letting several health plans use that as an excuse to not pay for them. Now Peterson, which is using a framework from ICER, has basically said the same thing about diabetes solutions and is moving on to MSK, with presumably more categories to be debunked on deck.

Continue reading…