House Energy and Commerce Committee Republicans seemed surprised last week when representatives of the insurance industry reported that they didn’t have enough data yet to forecast prices for next year’s health insurance exchanges, the market was not about to blow up, and that so far at least 80% of consumers have paid for the health insurance policies they purchased on the exchanges.

House Energy and Commerce Committee Republicans seemed surprised last week when representatives of the insurance industry reported that they didn’t have enough data yet to forecast prices for next year’s health insurance exchanges, the market was not about to blow up, and that so far at least 80% of consumers have paid for the health insurance policies they purchased on the exchanges.

The executives also reported there are still serious back-end problems with HealthCare.gov––particularly in being able to reconcile the people the carriers think are covered and the people the government thinks are covered.

These are all things that you have read about a number of times on this blog.The insurance companies are doing their best to make Obamacare work.

Why?

Because if they want to be in the individual and small group markets, Obamacare is the only game in town––it has a monopoly over these markets. The same rules that apply to the individual market also apply to the even larger small group health insurance market.

Unless Obamacare is repealed this is the business reality insurance companies have to deal with. So, you make the best of it.

Republicans are right to think Obamacare is unpopular. The latest Real Clear Politics average of all major polls taken since open-enrollment closed still has 41% of those surveyed favorable to the law and 52% opposed to the law––about as bad it is always been.

But Obamacare is not going to be repealed. The sooner Republicans come to understand that the better for them.

I really think Democrats have the potential to take back, or at least neutralize, the health care issue by the November elections if Republicans aren’t careful.

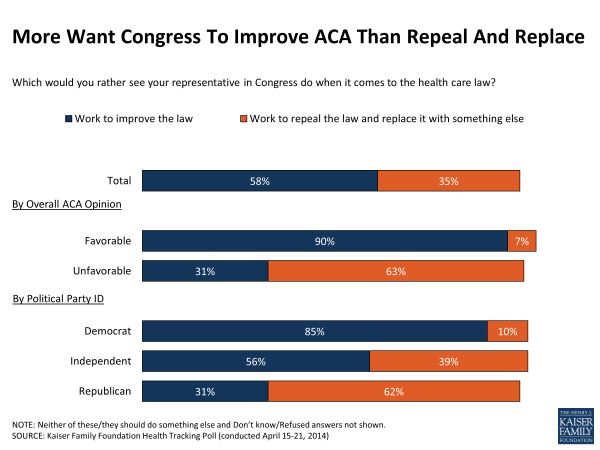

Most voters are still very unhappy about Obamacare. They hate the individual mandate and they find the health plans––with their after subsidy premiums still too high, the deductibles and co-pays way too big, and the narrow networks too confining––unattractive.But most don’t want it repealed, they want it fixed. In the latest Kaiser poll 58% want the law improved and only 35% want it replaced.

But, the Republicans’ challenge is that they have painted themselves into a political corner by convincing their base Obamacare has to be repealed––Republicans want the law repealed and replaced by a margin of 62% to 31%. That means any Republican running in a contested primary has to continue the repeal and replace line.

But once in the general election, the tables turn on this argument.

Independents want the law improved by a margin of 56% to 39%. Repeal and replace is a loser issue in the general election.

Looking at what the independents have to say, the Republican repeal and replace strategy could well run into trouble come November IF Democrats are able to convince voters they are the party that understands Obamacare needs fixing and they are the ones to do it.

Obamacare will certainly have to be fixed.

Amid all of the Democratic euphoria over “eight million enrollments” (which are really about 6.5 million enrollments once all of the premiums are finally paid) is the fact that onlyabout a third of those eligible to purchase subsidized health insurance on the exchanges did so.

That means two-thirds did not.

In an earlier post, I recounted the old marketing story about the dog food company that pulled out all of the stops to create the best dog food ever. But the product didn’t sell––because the dogs didn’t like it.

Obamacare is a product that is a monopoly––you can’t buy individual health insurance anywhere else. It is a product that about everyone would agree you are much better off to have than not have. It is a product that the government will pay a big part of most people’s cost. And, if you don’t buy it the government will fine you.

And only a third of the subsidy eligible signed up?

I will suggest that lost in the celebration over “eight million enrollments” is the fact that two-thirds of the consumers who were eligible for a subsidy didn’t buy it. And, according to my travels in the market, about half that did buy it in the insurance exchanges already had insurance.

A just released McKinsey survey done during April estimates that 74% of those who bought coverage inside and outside the insurance exchanges had been previously insured––which would be consistent with my finding.

Obamacare’s two biggest problems come down to this: Not enough people are signing up for it to be sustainable in the long-term because the products it offers are unattractive.

The polls and the market’s response to Obamacare are all consistent: The program is not attractive and needs some serious fixing but it isn’t going to be repealed.

Republicans can continue to exploit this issue only if they understand this.

And, Democrats can win the issue back, or at least neutralize it, if they can get beyond their current euphoria over “eight million” and get real about how unhappy people are with the program and the plans it offers––and come up with a plan to fix Obamacare.

I feel like I’m watching a football game here. The ball (Obamacare) has been fumbled. It’s bouncing down the field up for grabs. The Republicans are saying they don’t have to chase the fumble because, “We’re are so far ahead we’re going to win the game anyway.” The Democrats are saying, “What fumble?” They’ve got “eight million reasons why the ball hasn’t been fumbled.”

Going into November, Obamacare as a major political issue, is up for grabs.

It’s going to be interesting to see which side, if any, gets past its overconfidence by figuring that out and jumps on the ball first.

Robert Laszewski has been a fixture in Washington health policy circles for the better part of three decades. He currently serves as the president of Health Policy and Strategy Associates of Alexandria, Virginia. You can read more of his thoughtful analysis of healthcare industry trends at The Health Policy and Marketplace Blog, where this post first appeared.

Categories: Uncategorized

I hope you’re just being innocent here, and not intellectually dishonest.

You may not have been able to keep your plan, however, I’ll bet you kept very similar coverage across all of those changes. I’ll bet you kept your doctor, your hospital and prescription drug choices, much of your network. “Losing your plan” was merely a technicality.

Contrary to you, people on Obamacare lost their plans and got back plans that were vastly inferior to what they had before. Yeah, the plans cover all the “essential services,” but they don’t cover them very well at all. High deductibles, poor networks. That is the name of the game on Obamacare.

I work at an academic medical center. I have had employer-provided health insurance for the 24 years I have worked here. However, I have not been able to keep my plan either, whether I liked my plan or not. My employer, like many, has been changing plans all the time, especially over the last decade.

President Obama was unfortunate to use those words about getting to keep your plan if you liked it. But the reality is that none of us is getting to keep our plans, and it has little to do with Obamacare.

Don’t get me wrong; I prefer to be in the large-group insurance market, despite my employer nibbling away at the benefits each year. I am just making the points that (a) none of us truly gets to keep our plans if we like them, and (b) a good deal of the bad things happening in healthcare have nothing to do with the ACA.

“Obamacare’s two biggest problems come down to this: Not enough people are signing up for it to be sustainable in the long-term because the products it offers are unattractive.”

The other problem is, Americans don’t like being told what to do, or what product they have to buy. They like to think they have plenty of choices. This is why the statement still rankles many “if you like your doctor (plan) you can keep it), for better or worse.