Tom Kelly is the CEO of Heidi Health, another of the many ambient AI scribes that is spreading its wings to other roles, including bringing its own AI Open Evidence competitor! He calls it an AI care partner. Heidi started in Australia, and quickly moved to the UK and Canada, but now are in over one hundred countries. More recently they have come to the US and have now four major health systems and a lot of other mid market users. Tom think’s Heidi will soon do all the “work around the work”, and he doesn’t think it has to be deeply integrated with the EMR. He sees that as a superpower as doctors don’t want to be in the record. Is he right? Are scribes and ambient AI going to be separate? Does the scribe have to be a medical device, as it does in the UK? Will patients use it? Lots of questions about the future and Tom has lots of answers. Some might even be right!–Matthew Holt

Today’s April Fool is me in 2011

I randomly found this interview I had completely forgotten about on Youtube from 2011. I was younger and thinner then, even though I didn’t have much hair. And I was very optimistic that tech was going to change health care in 10 years……and that it was going to take a long time. Guess we are still waiting!

Kevin Wang, Suki

Suki is one of the original Ambient scribing, now Ambient intelligence, companies. They’re selling both to providers and to other partners using their tech in their tools and services (think telehealth, other EHR providers like Athena, and more). Kevin Wang is the Chief Medical Officer, and he told me about the evolution of ambient documentation, how it makes doctors happy, and how it’s now moving into improving coding (and billing) but will soon be moving into improving clinical decision support. We haggled a little about the ROI from Ambient and where that comes from (remembering codes), and discussed how the EMR v Ambient plays out. And we talked a little about what the impact of ambient and AI will be on medicine…–Matthew Holt

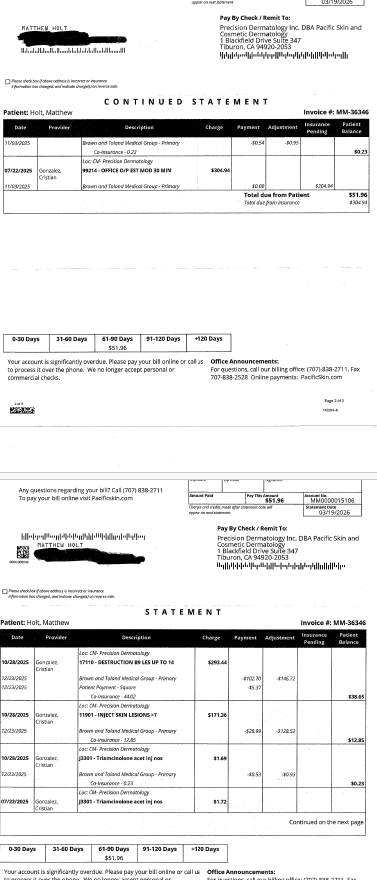

Adventures in health care billing. My $51.96 zit co-insurance

By MATTHEW HOLT

I know my many fans love me delving into the world of why we get seemingly incorrect trivial bills in health care, and what they all mean. The long telenovella of the $39.94 bill from Labcorp is as yet stalled with One Medical apparently resubmitting the original claim with the new preventative codes on it. But even though I am continuing and expanding my role as a difficult patient this year, there are still some blasts from the past that won’t quite leave.

This particular one concerns some rather unpleasant dermatology issues. For many years I had an nasty small sore/lesion on my leg that never quite healed. Then I started getting a few more that started as zits and never quite left. My wise PCP Andrew Diamond at One Medical told me to use some antibiotic wash and referred me to a dermatologist. Unfortunately the one I was referred to was out of network for the Blue Shield HMO I was in, but one request back to One Medical and I was both sent to a dermatologist in my network and got a pre-auth in the mail from Blue Shield to go see him!

Dr Cristian Gonzalez took a quick look at my leg, decided what the problem was, and proceeded to inject, freeze and attack my various lesions. He then prescribed a cheap topical steroid for me to use, and basically after 4 visits over the summer and Fall, my legs went back to resembling a baby’s bottom–well more or less.

For each specialty visit Blue Shield had a co-pay of $85 per visit, which I handed over using my HSA card. One time the front desk said I had a balance, but when I asked them what it was for they told me it was a mistake. Until this week.

Some 4 months after my last visit I got a bill in the mail for $51.96

Given that I had made a co-pay of $85 each time, this seemed a little odd. So I took a look at my Blue Shield EOBs. (BTW they are back online, you may recall they vanished when Blue Shield cancelled and then changed my plan but the Internet never forgets….)

There a curious anomaly began to play out. Each visit generated three identical claims and three more or less identical EOBs.

Continue reading…Ian Shakil, Commure

Ian Shakil is the Chief Strategy Officer of Commure, the AI platform being used by HCA, Tenet and others. He came to Commure via its acquisition of Ambient AI vendor Augmedix, and there are a lot other other new acquisitions within Commure (Athelas, PatientKeeper, Memora Health, Rx Health etc). We dived in not only about what Commure does but the big question of how does a client like HCA or Tenet decide what Commure does, vs what Meditech does, vs what Google does vs what they do internally. We also (sorta) looked into the various criticisms (basically all from Sergei Polevikov!) of what Commure and its main funder General Catalyst are up to and what is happening at Summa Health the hospital in Ohio that GC bought. He also says the good experience from AI will come to help patients this year, and I’ll be holding him to that!–Matthew Holt

Jason Prestinario, Particle Health

Jason Prestinario is CEO of Particle Health. The company is best known for its current lawsuit against Epic, but behind that there is a real company delivering a set of products as on ramp for clients wanting to access health data. Particle was cut off from access to Carequality & Epic a couple of years back but is now both delivering services to its customers and separately suing Epic for being an abusive monopoly regarding its payer platform. I had written about this a couple of years ago but I used this chance to catch up with Jason, to see what the sate of play was. He explained that Carequality said that Particle was right in the original dispute, and why they were right and Epic was wrong. The court case continues. But it’s interesting to hear from someone in the middle of the new disputes about data. — Matthew Holt

Mario Danek, QNovia

Mario Danek is CEO of QNovia, a behavior change platform focusing on smoking cessation product. Essentially the problem with smoking cessation nicotine products is that they don’t deliver the “hit” of a cigarette as quickly as a cigarette or a vape. Mario’s new vape-like product delivers a nicotine replacement therapy (think like Nicorette gum) just as quickly as the form factor it’s replacing. He is hoping that the device/drug/and forthcoming mental health support will be the engine to reduce the current smoking rate from the stubborn level it’s got stuck at. He told me about its likely time to commercialization–Matthew Holt

Preeti Bhargava, Arintra

Preeti Bhargava is CTO of Arintra. She is the living embodiment of my crack that the smartest people in the world spent the 2010s convincing people to click on ads and now spend their time figuring out how to bill payers more for providers doing the same work. Arintra is in the RCM business. It uses AI to read the medical chart and automatically generate claims using fewer human coders, and generating up to a 5% revenue uplift for one customer, Mercy Health. Of course those paying those claims may have noticed, so we had a chat about the emerging AI RCM arms race–Matthew Holt

Jesse Shoplock, Inbox Health

Jesse Shoplock is SVP of Business Development at Inbox Health. They are trying to help one of the messiest parts of American health care, figuring out both how much patients owe at the point of care and how to actually help the providers get paid. As of now 70% of patients don’t know what they owe, and in some cases those patients payments are 30% of total revenue and a bug chunk of that isn’t being collected. Jess told me how they are helping practices fix that. (And in the answer to my question Jesse didn’t know, they’ve raised some $55m so far)–Matthew Holt

Ratnakar Lavu, Elevance

Ratnakar Lavu is the Chief Digital Information Officer of Elevance, the holding company of Blue Cross and Blue Shield plans in some 14 states (usually called Anthem Blue Cross). We had a great chat about what the priorities are for Elevance, and Ratnakar’s goal is to use tech to make the member experience simple. They are leaning heavily on AI and chatbots to help members inform themselves, and to help providers speed up approvals for prior auth et al. We also discussed how they work with vendors and how they help them scale.–Matthew Holt