By MATTHEW HOLT

I know you all care, so I am giving a 7th update on the telenovela about my Labcorp bill for $34.95.

The very TL:DR summary of where we are so far is that in May 2025 I had a lab test to go with the free preventative visit that the ACA guarantees, but I was charged for the lab tests and I was trying to find out why, because according to CMS I should not have been.

For those of you who have missed it so far the entire now 7 part series is on The Health Care Blog (1, 2, 3, 4, 5 & 6). Feel free to back and read up.

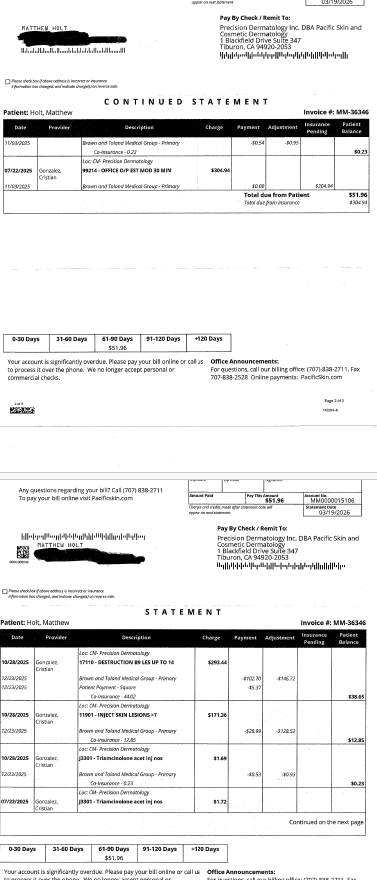

Where we left it last, Brown and Toland (the IPA between my plan Blue Shield of California and Labcorp) told me that on 8/29/2025 their benefits department had finished their review and reported that the original lab test wasn’t coded as preventative lab services by One Medical, so that the co-pay of $34.95 was correct. ($34.95 was the total agreed payment for all the tests, charged at a total of $322.28. And as it was less than my $50 copay, LabCorp only charges the patient for the total, not the $50!). That call was on December 18 and resulted in update 6.

I next (well about a week later later because life, etc) requested One Medical to resubmit the bill coding it as preventative. That happened on Dec 24, 2025 and someone called Alexis working for One Medical, while exhibiting terrible life skills, replied on Dec 25 and sent it on to their billing department asking them to recode it. I followed up on Jan 15 and Alexis at One Medical confirmed that the billing department had faxed the updated codes to Labcorp. I presumed that Labcorp would resubmit the claim to Brown and Toland and I would eventually get a $0 bill from them.

However, today (4/9/26) I called Brown and Toland about a different telenova — a coinsurance I had received for a dermatology office visit. While I had the rep on the phone, I asked about the Labcorp bill from May 2025. She told me that the benefits team at Brown and Toland had decided on December 18 — that’s right, before I contacted One Medical to ask them to resubmit the claim — that the codes should have been classified as preventative and that I don’t owe the $39.94. Of course Dec 18 was the last time I called Brown and Toland when they said that I had to have One Medical resubmit the claim to Labcorp. Sounds a little coincidental that very same day their benefits team re-reviewed the claim and decided that it should change to being preventative. But who am I to complain or raise a fuss!

Just to add to the complication, on Dec 29 someone within Brown and Toland (customer service?) received that message from the Benefits team and sent it over to the “Epic team” which I assume deals with outliers, with a request to reprocess it. As of today (April 9, 2026), that reprocessing had not happened.

As it happens they may not bother. Labcorp way back when agreed not to send me to collections, and I don’t know if they care enough to go after Brown and Toland for the $39.94, or have just given up on it. More likely if the claim is reprocessed, it will probably be tossed into the capitated amount they already got paid. Which is why the “payment” for my two subsequent lab tests was $0.

So I think we may be at the end of this series. (OK, if you read part 6 there are a couple of other tests Brown and Toland think I should be paying for but no one has sent me a bill for those yet and I may just let sleeping dogs lie).

But don’t worry, there’s always more stupidity in the way Americans deliver and pay for health care, so I’ll keep talking about it. Until we blow up the system and build one that works.

Mathew Holt is the Founder & Publisher of THCB