By TOMMY BEVERIDGE

Just like the Holy Roman Empire was none of those things, America’s health care system is neither health care, nor a system. Both are in fact decentralized commercial arrangements clothed in things that sound good, like Holy-Romanness, or Consumer-driven Health Care. Rather than health care, we have a patchwork of consumer products and government subsidies designed to pay a vast cadre of individuals and interests to perhaps incidentally provide health care. To even call it a system would imply something centrally coordinated, which no one in their right mind would do.

It feels hopeless. Health insurance is expensive, arbitrary, and capricious. It profits off of slices of an ever-growing pie, regardless of margins. The providers we cannot live without often charge whatever the market will bear. On top of this, the government, directed by laws written by politicians unwilling to upset powerful interests, has spent the past two decades pushing complex payment ideas with little result except a growing ecosystem of consultants specializing in gaming such incentives. Then there are the consultants— arms dealers in both sides of a war, selling hospital systems software that helps them bill as much as they can for their work, and health insurance companies software that helps them deny claims wherever they can.

We all know this. It’s the learned helplessness about it all that gets me. Sometimes a sob story about chemotherapy denied enters the zeitgeist, or the tale of a lone vigilante taking out a health care executive, but mostly we just take the 7 percent annual premium increases and deductible hikes with a stiff upper lip. Meanwhile, few of the players: payer, provider, government, or software slinger, put American’s health at the top of their agendas. Customer satisfaction? Maybe. Public ire? Occasionally. Shareholder value? Certainly. But our actual health?

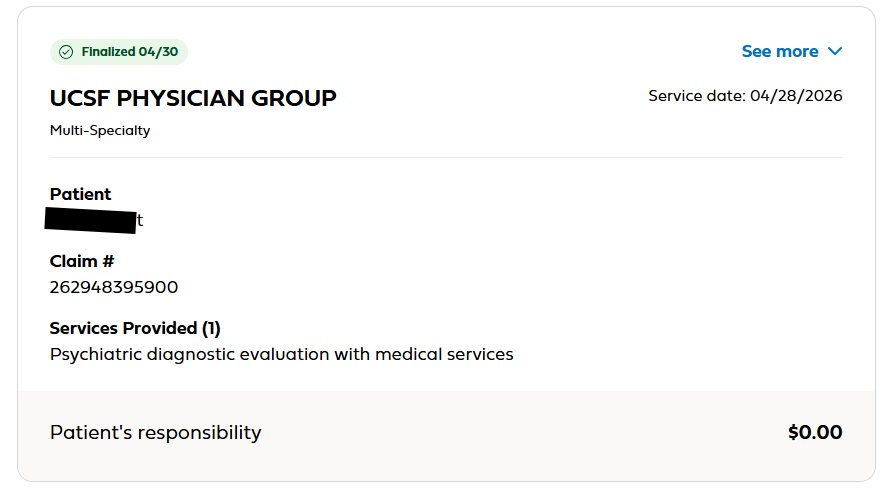

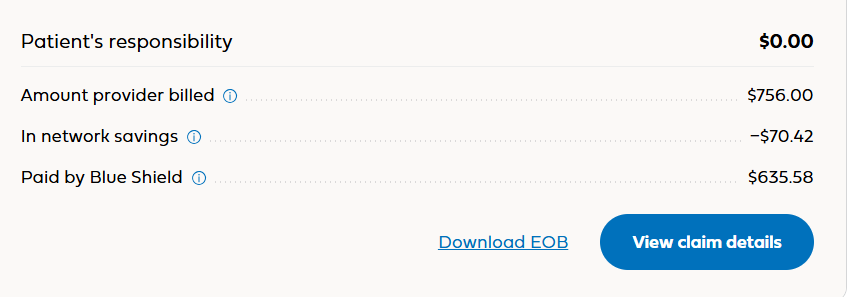

Something that isn’t health care or a system can’t be a health care system. Not when this how we pay for care:

Continue reading…