By MATTHEW HOLT

There’s been a lot of discussion lately about whether digital health is a legitimate place for venture capital. There have been lots of huge failures, very few notable successes (and certainly no “biggest companies in the world” yet), while some real giants (Walmart/Walgreens/Amazon) have come in and then got out of health care.

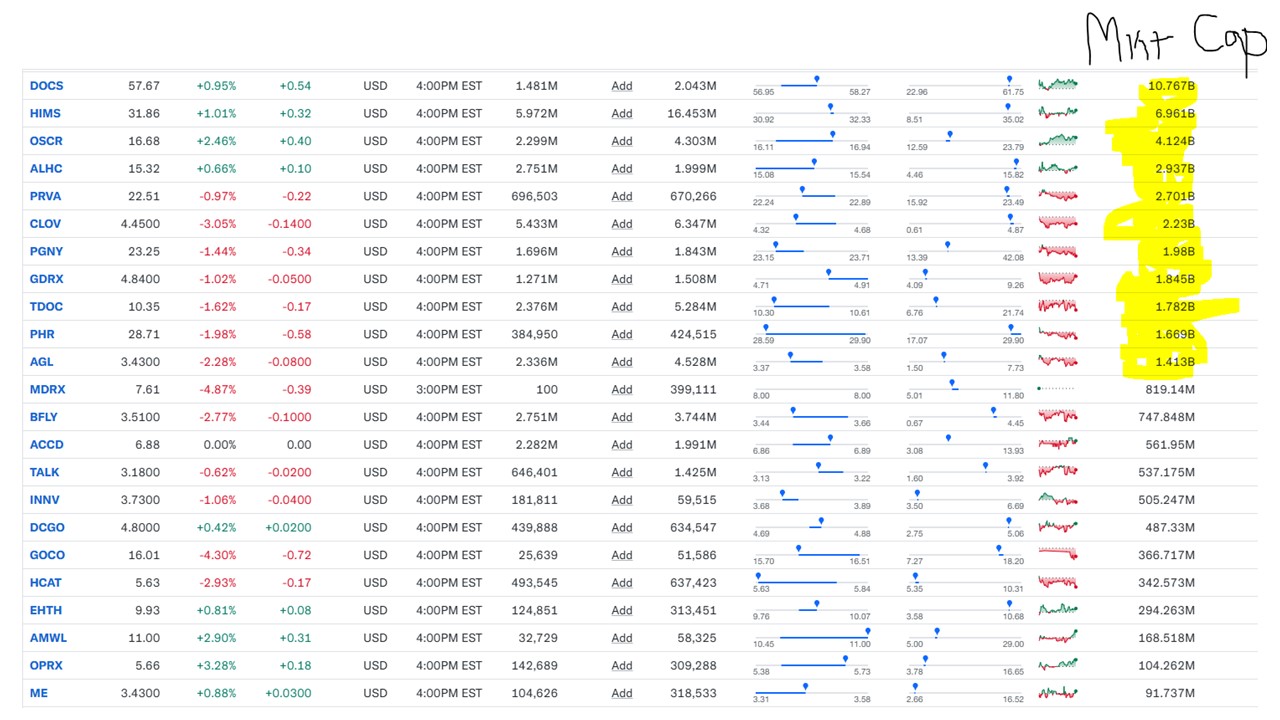

I don’t have to tell you again that most of the publicly traded digital health companies are trading at pennies on the dollar to their initial valuations. But I will. Look at that chart below.

Heck even Doximity– which prints money (45% net margins!)–is trading at well under its post IPO high. My quick overview is that there are not very many publicly traded companies at unicorn status. With really only Doximity, HIMS and Oscar being very successful. (We can have a separate argument as to whether Tempus and Waystar are “digital health”). And there are many, many that are well off the price they IPOed at. All that at a time when the regular stock market is hitting record highs.

Which makes it interesting to say the least that Define Ventures just came out with a report saying that in general digital health has done well as a venture investment and that it was likely to do even better, soon.

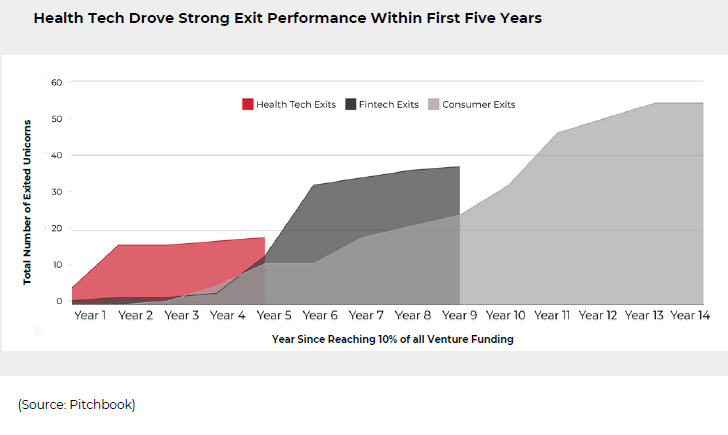

The report isn’t that long and is well worth a read but their basic argument compares digital health venture investments to those in fintech and consumer tech. Essentially it took digital health a lot longer to get to 10% of total venture investment than fintech or consumer tech, but it got there after 2020. Now more than 10% of all VC backed unicorns out there are health tech companies. Yes there was a retrenchment in 2022-3 but health tech investment fell less than other sectors in 2022-3 and is basically back in 2024.

The Define forecast forecast is interesting (it’s the chart below). Define posits that it took 4-5 years after the fintech and consumer tech sectors became 10% of VC dollars for them to start pumping out exits and IPOs. There are 30-50 each in those sectors now, but health tech was ahead of that with 18 exits already in the first 5 years after getting to 10% of VC dollars, and those exits were on average double the size of the fintech/consumer tech exits. (Although to be fair the health tech exits were when the market was higher after 2020)

In fact their analysis is that capital returned was about 10x investment. You might say, but hey Matthew didn’t you just show me a chart that most of those 18 companies were public market dogs? And you’d be right.

Continue reading…