By MATTHEW HOLT & ELIZABETH BROWN

Last year was a remarkable time for digital health. Obviously it was pretty unusual and tragic for the world in general as the COVID-19 pandemic continued to wreak havoc. We mourn those lost, and we praise our front line health workers and scientists. But for digital health companies, in almost no time 2020 changed from fear of a market collapse to what became a massive funding boom.

But no-one has reported from the ground what this means for digital health companies, of which there are perhaps 10-15,000 worldwide with maybe 6-8,000 based in the United States. Despite the headlines, most are not pulling down $200m funding rounds or SPACing out. So working with professional services firm Wipfli, we at Catalyst @ Health 2.0 decided to find out what digital health companies experienced in this most extraordinary year.

Between Thanksgiving 2020 and mid-March 2021, we surveyed more than 300 members of the digital health ecosystem, focusing on leaders from more than 180 private (and a few public) digital health companies. We asked them about their market, their experience during COVID-19, and what they thought of the environment. We also asked them about the mechanics of running their businesses. The results are pretty interesting.

The Key Message: COVID-19 was very good for digital health companies–on average. Most are very optimistic but, despite the massive increase in funding since the brief (but real) post-lockdown crash, most digital health companies remain small and struggling for funding, revenue, and customers.

We also heard from investors, and a bigger group we called “users” (mostly payers, providers, pharma, non-healthcare tech companies, e-patients & consultants). While these “users” also saw a big trend towards the use of (and, to a lesser extent, paying for) digital health tools and services, they were not as gung-ho as were digital health companies or investors, who were even more optimistic.

The summary deck containing the key findings is below and there is more analysis and commentary below the jump.

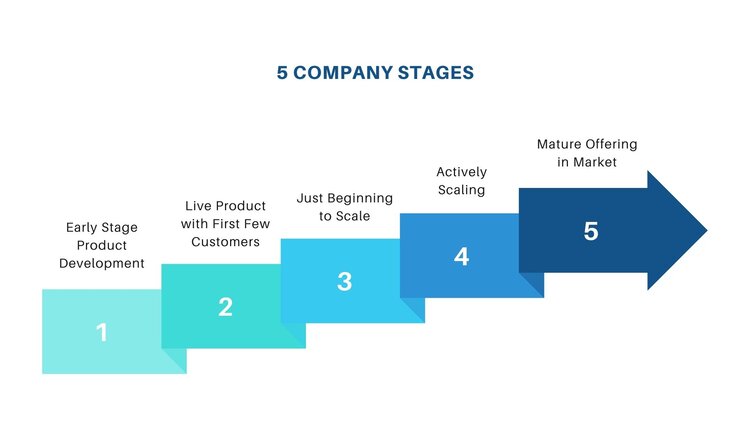

The Demographics: Most digital health companies are small startups. Given the ease of starting a company and the difficulty in selling to larger incumbents or getting a large number of consumers as users, that is not a surprise. In our sample, 49% of digital health companies had fewer than 20 employees, and 20% had fewer than 5. While we asked several objective questions about size, revenue & funding, we also asked companies to self-select as to their “scale”, in a way that matches our classification of startups. The five stages are:

It is only when companies are “Actively Scaling” that they start to really grow their employee base, with more than 50% of companies in this stage having more than 100 employees. Even so, a substantial portion (30%) of “Mature” companies still have between 50-99 employees

Customers & Products: Most digital health companies are targeting more than one type of customer. 60% were targeting providers with 57% targeting payers. Substantial minorities (33% & 34%) were selling to consumers and employers, respectively. And, of course, there are several commonalities–of the companies who said they were targeting employers, 75% also targeted payers. When looking at the products and service offerings companies are providing, almost all (86%) were selling software, with over half (55%) selling services–in fact more than half of those selling software were also selling services.

Revenue: We also asked explicitly about revenue–which, not surprisingly, irked some respondents! As you would expect in 2019, a majority of companies had either no revenue (33%) or less than $500K (21%) in revenue. But they had high expectations, with only 25% expecting to be below $500K in revenue by 2021 (this year!). In fact, while only 10% of companies had revenue over $30m in 2019, 16% expected to be at that level in 2021.

As you might expect the biggest changes were expected by those who described themselves as “Just Beginning to Scale” or “Actively Scaling”. 75% of the the “Just Beginning” group were at $2m or below in revenue in 2019 (in fact most were below $500K), whereas 65% expect to be above $2m in 2021. Only 14% of the “Actively Scaling” group were above $30m in 2019 but a full 48% think they’ll be there in 2021.

COVID-19’s Impact on Revenue: We tried to understand the impact of COVID-19 by asking about how companies’ actual revenue in 2020 compared to plan or expectation. 41% said that they were above expectation, with 29% saying they were slightly above (15-50% greater) and 12% saying they were significantly higher (50+%) than plan. Only 5% (50+%) were significantly below plan. Given how optimistic the startup forecasts I see tend to be, I think this shows that COVID-19 did boost revenue dramatically. Again, it was the companies who were “Just Beginning to Scale” or “Actively Scaling” who saw the most unexpected upside.

COVID-19’s Impact on Product Usage & Personnel Hiring: Revenue is all very nice, but what about actual usage? As you might expect, 65% of companies saw usage of their products or service offerings increase more than expected, with 15% saying it increased dramatically (50%+ above plan). Those with products in the market already, either “Just Beginning to Scale,” “Actively Scaling” or “Mature Offering”, saw the biggest uptake, with 29%, 37% & 27% respectively, saying that usage increased dramatically. This translated somewhat into hiring plans, with 29% of companies hiring more than planned, and, again, that deviation being concentrated in those “Just Beginning to Scale (31%),” “Actively Scaling (37%)” or “Mature Offering (36%)”.

Most companies (66%) added new products and services during COVID-19, as any casual observer could see. In fact, Catalyst @ Health 2.0 built an entire version of our SourceDB database showing all the new COVID-19 products we tracked. But, it is a reasonable conclusion that companies with products in the market mostly did better than companies just coming to market and starting their sales cycles.

Regulation & Data Security: Not unrelated to the fact that our sponsors at Wipfli provide business process, regulatory advice and data security certification, we asked a long series of questions about those issues and other business processes. Perhaps the most interesting result was that knowledge about applicable regulations was significantly lower in “Early Stage” companies, with 61% of them either “just getting educated” or having a “fair to medium understanding”. “Mature” companies had either in-house staff (45%) or a “strong level of understanding”. However, while 70% of digital health companies reported being asked about data security by (potential) clients, only 25% had been certified by an outside body like HITRUST–suggesting that more needs to be done.

Dealing with the “New Normal”: When asked about the actual mechanics of running their businesses during COVID-19, digital health companies were very positive. 45% said that the transition to “Work from home” was smooth sailing, and 24% believe productivity went up, versus only 12% who felt that it diminished.

More importantly, digital health companies are very optimistic about the impact of COVID-19 on their business. 47% said it would be net positive and 40% believed it would dramatically improve their prospects. Not one company said that COVID-19 would overall be a long-term problem for their business. The contrast here to many other sectors of the economy could not be starker. This is despite the fact that more companies saw sales cycles increase (44%) rather than decrease (25%).

Funding & the Investment Climate: In a time when there are several $100m fundings announced seemingly daily, the first thing worth remembering about early stage companies in general and digital health in particular is that the venture capital spoils are not divided evenly. More than 25% of our sample had raised under $500K and 53% less than $5m. While the mean investor funding amount amongst the survey’s digital health companies was over $40m, the median was less than $4m. Many earlier stage companies felt that the typical VC did not have time or interest in something new or small.

Nonetheless, the mood is overall very optimistic, with 62% saying the investment climate has improved compared with before COVID-19. However, the bigger and later stage the company, the more likely they are to think the climate has improved–those $100m rounds are in general going to companies already scaling very fast! And for what it is worth, ALL the investors we asked thought that the investment climate for digital health companies has improved, and almost all thought their valuations had gone up. But, surprisingly, none of those investors said that the time they needed to make a decision had gone down–presumably they were all operating at lightning speed already? (We are not sure every company desperately wanting a VC to answer their email would agree!)

Some Final Thoughts: There is no question that on basically any measure, digital health companies are in much better shape and much more optimistic than they were pre-COVID-19. Most companies believe that the business and investment climate is much better than it would otherwise have been, and that their revenue and their products’ usage is substantially higher than they expected pre-COVID-19. But, there are clearly going to be headwinds; probably the biggest for most is that sales cycles have actually increased. And for the early stage companies, the huge funding rounds (and the even bigger VC fund raises that are going with them) mean that it can be harder for them to get the relatively small amounts they need to prove themselves before they are ready to scale.

Matthew Holt is the Founder & Publisher of THCB and Co-Chairman at Catalyst @ Health 2.0. Elizabeth brown is a Program Manager at Catalyst @ Health 2.0

Categories: Health Tech, Matthew Holt