Jason Prestinario is CEO of Particle Health. The company is best known for its current lawsuit against Epic, but behind that there is a real company delivering a set of products as on ramp for clients wanting to access health data. Particle was cut off from access to Carequality & Epic a couple of years back but is now both delivering services to its customers and separately suing Epic for being an abusive monopoly regarding its payer platform. I had written about this a couple of years ago but I used this chance to catch up with Jason, to see what the sate of play was. He explained that Carequality said that Particle was right in the original dispute, and why they were right and Epic was wrong. The court case continues. But it’s interesting to hear from someone in the middle of the new disputes about data. — Matthew Holt

Nabla — It’s been a rocketship

I met the Nabla management team two years ago. Two years later they have ridden the wave of AI scribing to be one of the leaders in the field. At HLTH this year, I caught up with CEO Alex Lebrun and COO Delphine Groll to check in on their growth (150 customers and 100K users) what the next little bit of ambient AI scribing will look like (more specialties, more integration) and whether they’re scared of Epic (no!).–Matthew Holt

Justin Schrager demos Vital.io

Justin Schrager is the CMO of Vital.io. Their technology sits in the hospital telling patients what is going on with their care while they are in the hospital, particularly in the ER. Justin showed a deep demo about the patient experience of using Vital.io which includes what the patient can expect and guides them through the confusing workflow. It allows the patient to make requests, and also lots of guidance about what is happening to them, or for example what lab results might mean. It goes as far as helping people book appointments for follow up with the right doctor. We had a great chat about the product and also about the realities of running a tech company that has to integrate with Epic and many other EMRs.–Matthew Holt

Epic’s “Emmie” Chatbot Enhances the Patient Voice – For Their *Real* Customers

By MICHAEL MILLENSON

A Rock Health write-up of this year’s Epic Users Group Meeting captured the artificial intelligence vibe with a play on the names of three new AI chatbots rolled out by the country’s dominant electronic health record firm. “Epic Goes APE (Art, Penny and Emmie),” read the headline, using the first letters of the names of chatbots designed for, respectively, clinicians, revenue cycle managers and patients.

Emmie does positive things for patients – more on that in moment – but at its core the chatbot is a B2B play, designed to address the needs of the hospitals, medical groups and others whose fees have built the privately held EHR firm into an estimated $5 billion business.

Emmie is not an agent of patient autonomy. Its purpose is to help Epic customers (health systems and physician practices) provide more and better services to their customer, the patient, as long as that patient remains a customer.

That context is important. Yes, in a way it’s #PatientsUseAI, but that use is analogous to the AI algorithms deployed by Netflix. While you may marvel at their power of personalization, they’re never going to tell you that the best movie for your particular interest is harbored over at Hulu and, by the way, even if you’re watching tons of programs with medical themes, you’re still a couch potato.

I wasn’t present at the gathering at Epic’s Verona, Wisconsin headquarters, but news accounts and LinkedIn postings suggest that, unsurprisingly for this type of meeting, there was more drama than details. Much of what was unveiled and hinted at – the company said it’s working on more than 200 AI applications – will be rolled out over the course of 2026 and beyond.

Here’s Epic’s introduction of Emmie and Art from its LinkedIn account:

Informed by their chart and connected devices, Emmie is designed to support patients between visits. Whether it’s explaining test results in easy-to-understand terms, suggesting next steps, or guiding patients through open-ended conversations about their health, Emmie makes it easier for patients to stay on top of their health and walk into the exam room with a clear picture.

On the clinician side, Art is gathering data from Emmie to get the doctor the information they need before the visit even begins. Art is designed to reduce administrative burden, help doctors better understand their patients, and offer context-informed insights. This can take the form of generating pre-visit summaries, taking real-time notes, and even taking actions like placing orders or verifying prior authorization requirements.

That Rock Health analysis suggested that the real significance “may be less the function and more the channel,” since consumers are far more willing to share health data with their provider – in this case through Epic’s MyChart – than with a tech company (such as an AI vendor). “By capturing patient questions, decisions, and symptom-checking,” Rock Health noted, “Epic gains visibility into information consumers might hesitate to share with a generalist tech company. The EHR giant has already signaled that this data will feed back into [its] tools.”

Or as Epic did not say, “We empower our customers. We empower patients. We empower ourselves.” Good intentions alone do not get your product into use by more than half of all acute-care hospital beds in America, according to a KLAS estimate of market share.

At Healthcare IT Today, veteran tech journalist John Lynn sniffed out the actual schedule for all Emmie’s promised pro-patient wonders. According to Lynn (presumably from Epic itself),

- proactive outreach and images is coming in March, 2026

- active engagement in November, 2026

- future screenings arrive sometime in 2026 (no month given).

Bill payment, scheduling abilities using SMS (texting) and a voice agent are all “coming in the future.”

As I commented on the Epic LinkedIn post, “How about patient-reported outcome measures [e.g. Proteus Consortium’s], whether from an app linked to Epic (i.e., like Twistle by Health Catalyst or others) or the patient’s own wearables?” I tagged Seth Hain, Epic’s senior vice president of research and development, who played a prominent role at the meeting, but got no reply. (To be fair, maybe he took some vacation time after an intense few weeks.)

In a recent STAT First Opinion that took up the topic of autonomy, I asserted that true informed consent means physicians should be obligated to inform patients what Epic’s Cosmos system says about the likely outcomes of treatment for individuals with their clinical profile. Those predictions come from a database drawing on a mind-boggling 15.7 billion patient encounters. But patients should be able to access that information about different hospitals’ results on their own.

At the Users Group Meeting, Epic announced a further refinement of Cosmos, with founder and chief executive officer Judy Faulkner proudly announcing that the company will be able to “predict the future” for patients. (For a deep dive into Cosmos, I recommend the posts of veteran medical informatics expert Mark Braustein.)

Faulkner did what any smart businessperson would do. She spoke about how her company’s product would enable an important segment of customers, clinicians and health systems, to provide better care. What those customers actually do (or don’t do) for their “customer,” the patient, with the Epic software? Evidently “Not my job.”

Michael L. Millenson is president of Health Quality Advisors & a regular THCB Contributor. This first appeared in the “Patients use AI” Substack

Can EHRs Expand to Become Health Systems’ “Platform of Platforms” (UDHPs)?

By VINCE KURAITIS & NEIL JENNINGS

In a previous post in this series, we discussed healthcare’s migration toward Unified Digital Health Platforms (UDHPs) — a “platform of platforms.” Think of a UDHP as healthcare’s version of a Swiss Army knife: flexible, multi-functional, and (ideally) much better integrated than the drawer full of barely-used apps most health systems currently rely on. We included a list of 20+ companies jockeying for UDHP dominance, including two familiar EHR (electronic health record) giants — Epic and Oracle. This raises the obvious question for today’s post:

Can EHRs level up into becoming UDHPs — becoming healthcare’s platform of platforms? Or are they trying to wear a superhero cape while tripping over their own cables?

We see good arguments pro and con, and like most things in healthcare “it’s complicated.” Some say EHRs are uniquely positioned to make the leap. Others believe the idea is like trying to teach your fax machine to run population health analytics.

Thus, we’ll lay out the arguments for differing points of view, and you can decide for yourself.

by Vince Kuraitis and Neil P. Jennings of Untangle Health

Here’s an outline of today’s blog post:

- A Brief Recap: What are UDHPs?

- Thesis: EHRs Can Expand to Become UDHPs

- EHRs Currently Own the Customer Relationship

- Many Customers Have an “EHR-First” Preference for New Applications

- Epic and Oracle Health are Making Strong Movements Toward Becoming UDHPs

- Antithesis: EHRs Can NOT Become Effective EHRs

- EHRs Carry a Lot of Baggage

- Customers are Skeptical

- EHR Analytics Are NOT Optimized To Achieve Critical Health System Objectives

- EHR Switching Costs are Diminishing

- Cloud Native Platforms Accelerate Innovation and Performance

- It’s Not in EHR DNA to Become A Broad-Based Platform

- Synthesis and Conclusion

This is a long post…over 4,000 words…so we’ve clearly got a lot to say on the matter. Hope you brought snacks!

A Brief Recap: What are UDHPs? (Unified Digital Health Platforms)

In our previous extensive post on UDHPs, we described them as a new category of enterprise software. A December 2022 Gartner Market Guide report characterized the long-term potential:

The [U]DHP shift will emerge as the most cost-effective and technically efficient way to scale new digital capabilities within and across health ecosystems and will, over time, replace the dominant era of the monolithic electronic health record (EHR).

The DHP Reference Architecture is illustrated in a blog post by Better. Note that UDHPs are visually depicted as “sitting on top” of EHRs and other siloed sources of health data:

We noted that almost any type of large healthcare organization — health systems, health plans, pharma companies, medical device companies, etc. — had a need for UDHPs. However, today’s focus is more narrow — we limit the discussion to UDHPs in hospitals and health systems, primarily in the U.S. We use the term “health system” to encompass hospitals and regional health delivery systems.

In this post, we focus on the two largest EHR vendors in the U.S. — Epic and Oracle Health; they have a combined market share of 65% of hospitals and 77% of hospital beds.

In the remaining sections, we will lay out arguments on both sides of the issue of whether EHRs can (or cannot) expand to become UDHPs. The graphic below is our crack at a visual summary. The balloons represent the thesis – that EHRs can expand to become UDHPs; the anchors represent the antithesis – that EHRs can not expand to become UDHPs.

Thesis: EHRs Can Expand To Becoming UDHPs

Let’s look at the case for EHRs expanding to become effective UDHPs.

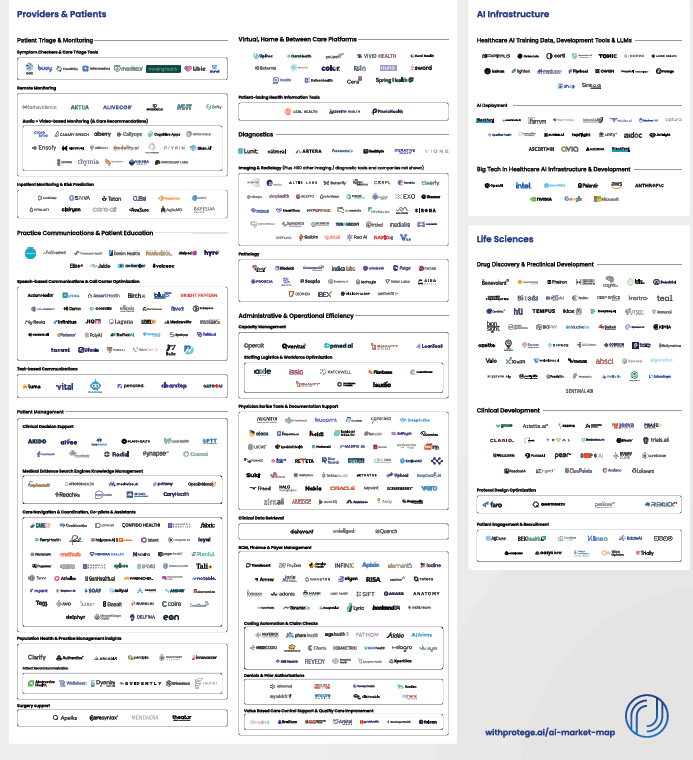

How to Buy and Sell AI in health care? Not Easy.

By MATTHEW HOLT

It was not so long ago that you could create one of those maps of health care IT or digital health and be roughly right. I did it myself back in the Health 2.0 days, including the old sub categories of the “Rebel Alliance of New Provider Technologies” and the “Frontier of Patient Empowerment Technologies”

But those easy days of matching a SaaS product to the intended user, and differentiating it from others are gone. The map has been upended by the hurricane that is generative AI, and it has thrown the industry into a state of confusion.

For the past several months I have been trying to figure out who is going to do what in AI health tech. I’ve had lots of formal and informal conversations, read a ton and been to three conferences in the past few months all focused dead on this topic. And it’s clear no one has a good answer.

Of course this hasn’t stopped people trying to draw maps like this one from Protege. As you can tell there are hundreds of companies building AI first products for every aspect of the health care value (or lack of it!) chain.

But this time it’s different. It’s not at all clear that AI will stop at the border of a user or even have a clearly defined function. It’s not even clear that there will be an “AI for Health Tech” sector.

This is a multi-dimensional issue.

The main AI LLMs–ChatGPT (OpenAI/Microsoft), Gemini (Google/Alphabet) Claude (Anthropic/Amazon), Grok (X/Twitter), Lama (Meta/Facebook)–are all capable of incredible work inside of health care and of course outside it. They can now write in any language you like, code, create movies, music, images and are all getting better and better.

And they are fantastic at interpretation and summarization. I literally dumped a pretty incomprehensible 26 page dense CMS RFI document into ChatGPT the other day and in a few seconds it told me what they asked for and what they were actually looking for (that unwritten subtext). The CMS official who authored it was very impressed and was a little upset they weren’t allowed to use it. If I had wanted to help CMS, it would have written the response for me too.

The big LLMs are also developing “agentic” capabilities. In other words, they are able to conduct multistep business and human processes.

Right now they are being used directly by health care professionals and patients for summaries, communication and companionship. Increasingly they are being used for diagnostics, coaching and therapy. And of course many health care organizations are using them directly for process redesign.

Meanwhile, the core workhorses of health care are the EMRs used by providers, and the biggest kahuna of them all is Epic. Epic has a relationship with Microsoft which has its own AI play and also has its own strong relationship with OpenAI – or at least as strong as investing $13bn in a non-profit will make your relationship. Epic is now using Microsoft’s AI both in note summaries, patient communications et al, and also using DAX, the ambient AI scribe from Microsoft’s subsidiary Nuance. Epic also has a relationship with DAX rival Abridge

But that’s not necessarily enough and Epic is clearly building its own AI capabilities. In an excellent review over at Health IT Today John Lee breaks down Epic’s non-trivial use of AI in its clincal workflow:

- The platform now offers tools to reorganize text for readability, generate succinct, patient-friendly summaries, hospital course summaries, discharge instructions, and even translating discrete clinical data into narrative instructions.

- We will be able to automatically destigmatize language in notes (e.g., changing “narcotic abuser” to “patient has opiate use disorder”),

- Even as a physician, I sometimes have a hard time deciphering the shorthand that my colleagues so frequently use. Epic showed how AI can translate obtuse medical shorthand-like “POD 1 sp CABG. HD stable. Amb w asst.”-into plain language: “Post op day 1 status post coronary bypass graft surgery. Hemodynamically stable. Patient is able to ambulate with assist.”

- For nurses, ambient documentation and AI-generated shift notes will be available, reducing manual entry and freeing up time for patient care.

And of course Epic isn’t the only EHR (honestly!). Its competitors aren’t standing still. Meditech’s COO Helen Waters gave a wide-ranging interview to HISTalk. I paid particular attention to her discussion of their work with Google in AI and I am quoting almost all of it:

This initial product was built off of the BERT language model. It wasn’t necessarily generative AI, but it was one of their first large language models. The feature in that was called Conditions Explorer, and that functionality was really a leap forward. It was intelligently organizing the patient information directly from within the chart, and as the physician was working in the chart workflow, offering both a longitudinal view of the patient’s health by specific conditions and categorizing that information in a manner that clinicians could quickly access relevant information to particular health issues, correlated information, making it more efficient in informed decision making. <snip>

Beyond that, with the Vertex AI platform and certainly multiple iterations of Gemini, we’ve walked forward to offer additional AI offerings in the category of gen AI, and that includes both a physician hospital course-of-stay narrative at the end of a patient’s time in the hospital to be discharged. We actually generate the course-of-stay, which has been usually beneficial for docs to not have to start to build that on their own.

We also do the same for nurses as they switch shifts. We give a nurse shift summary, which basically categorizes the relevant information from the previous shift and saves them quite a bit of time. We are using the Vertex AI platform to do that. And in addition to everyone else under the sun, we have obviously delivered and brought live ambient scribe capabilities with AI platforms from a multitude of vendors, which has been successful for the company as well.

The concept of Google and the partnership remains strong. The results are clear with the vision that we had for Expanse Navigator. The progress continues around the LLMs, and what we’re seeing is great promise for the future of these technologies helping with administrative burdens and tasks, but also continued informed capacities to have clinicians feel strong and confident in the decisions they’re making.

The voice capabilities in the concept of agentic AI will clearly go far beyond ambient scribing, which is both exciting and ironic when you think about how the industry started with a pen way back when, we took them to keyboards, and then we took them to mobile devices, where they could tap and swipe with tablets and phones. Now we’re right back to voice, which I think will be pleasing provided it works efficiently and effectively for clinicians.

So if you read–not even between the lines but just what they are saying–Epic, which dominates AMCs and big non-profit health systems, and Meditech, the EMR for most big for-profit systems like HCA, are both building AI into their platforms for almost all of the workflow that most clinicians and administrators use.

I raised this issue a number of different ways at a meeting hosted by Commure, the General Catalyst-backed provider-focused AI company. Commure has been through a number of iterations in its 8 year life but it is now an AI platform on which it is building several products or capabilities. (For more here’s my interview with CEO Tannay Tandon). These include (so far!) administration, revenue cycle, inventory and staff tracking, ambient listening/scribing, clinical workflow, and clinical summarization. You can bet there’s more to come via development or acquisition. In addition Commure is doing this not only with the deep pocketed backing of General Catalyst but also with partial ownership from HCA–incidentally Meditech’s biggest client. That means HCA has to figure out what Commure is doing compared to Meditech.

Finally there’s also a ton of AI activity using the big LLMs internally within AMCs and in providers, plans and payers generally. Don’t forget that all these players have heavily customized many of the tools (like Epic) which external vendors have sold them. They are also making their AI vendors “forward deploy” engineers to customize their AI tools to the clients’ workflow. But they are also building stuff themselves. For instance Stanford just released a homegrown product that uses AI to communicate lab results to patients. Not bought from a vendor, but developed internally using Anthropic’s Claude LLM. There are dozens and dozens of these homegrown projects happening in every major health care enterprise. All those data scientists have to keep busy somehow!

So what does that say about the role of AI?

First it’s clear that the current platforms of record in health care–the EHRs–are viewing themselves as massive data stores and are expecting that the AI tools that they and their partners develop will take over much of the workflow currently done by their human users.

Second, the law of tech has usually been that water flows downhill. More and more companies and products end up becoming features on other products and platforms. You may recall that there used to be a separate set of software for writing (Wordperfect), presentation (Persuasion), spreadsheets (Lotus123) and now there is MS Office and Google Suite. Last month a company called Brellium raised $16m from presumably very clever VCs to summarize clinical notes and analyze them for compliance. Now watch them prove me wrong, but doesn’t it seem that everyone and their dog has already built AI to summarize and analyze clinical notes? Can’t one more analysis for compliance be added on easily? It’s a pretty good bet that this functionality will be part of some bigger product very soon.

(By the way, one area that might be distinct is voice conversation, which right now does seem to have a separate set of skills and companies working in it because interpreting human speech and conversing with humans is tricky. Of course that might be a temporary “moat” and these companies or their products may end up back in the main LLM soon enough).

Meanwhile, Vine Kuraitis, Girish Muralidharan & the late Jody Ranck just wrote a 3 part series on how the EMR is moving anyway towards becoming a bigger unified digital health platform which suggests that the clinical part of the EMR will be integrated with all the other process stuff going on in health systems. Think staffing, supplies, finance, marketing, etc. And of course there’s still the ongoing integration between EMRs and medical devices and sensors across the hospital and eventually the wider health ecosystem.

So this integration of data sets could quickly lead to an AI dominated super system in which lots of decisions are made automatically (e.g. AI tracking care protocols as Robbie Pearl suggested on THCB a while back), while some decisions are operationally made by humans (ordering labs or meds, or setting staffing schedules) and finally a few decisions are more strategic. The progress towards deep research and agentic AI being made by the big LLMs has caused many (possibly including Satya Nadella) to suggest that SaaS is dead. It’s not hard to imagine a new future where everything is scraped by the AI and agents run everything globally in a health system.

This leads to a real problem for every player in the health care ecosystem.

If you are buying an AI system, you don’t know if the application or solution you are buying is going to be cannibalized by your own EHR, or by something that is already being built inside your organization.

If you are selling an AI system, you don’t know if your product is a feature of someone else’s AI, or if the skill is in the prompts your customers want to develop rather than in your tool. And worse, there’s little penalty in your potential clients waiting to see if something better and cheaper comes along.

And this is happening in a world in which there are new and better LLM and other AI models every few months.

I think for now the issue is that, until we get a clearer understanding of how all this plays out, there will be lots of false starts, funding rounds that don’t go anywhere, and AI implementations that don’t achieve much. Reports like the one from Sofia Guerra and Steve Kraus at Bessmer may help, giving 59 “jobs to be done”. I’m just concerned that no one will be too sure what the right tool for the job is.

Of course I await my robot overlords telling me the correct answer.

Matthew Holt is the Publisher of THCB

Bevey Miner, Consensus Cloud Solutions

Consensus is taking fax data, received by rural clinics, post acute, substance abuse clinics, home health et al, and helping them put it into their systems of records–which are in general not FHIR-enabled. They allow those facilities & services to receive referrals from acute care hospitals. By 2027 many of these standards are going to need to be FHIR enabled. Bevey Miner, EVP at Consensus, is a health care veteran who is working on both a policy and technology level to improve access to care, and thinks a lot about what unstructured data means in a world where we are trying to use data for AI and more. Super interesting chat about the murky backwaters of health care data and services. As Bevey says, “Not everyone is going to be Epic to Epic to Epic”–Matthew Holt

Jonathan Bush, Zus Health

It’s always fun to chat with Jonathan Bush. You kids today may not remember that he was the first CEO to take a cloud-based (Health 2.0!) company public back in 2007! Athenahealth didn’t end up challenging Epic because a cosmically evil hedge fund took it (and him) down as it was on its way to try to do that, but Jonathan has moved on and is now building a clinical data integration company called Zus Health. We talked Zus, digital health, whether there will ever be value-based care and more. 20 mins of digital health gold right here–Matthew Holt

Aneesh Chopra talks Cancer Navigation Challenge & more

Aneesh Chopra is the former CTO of the US under Obama. He’s now head of strategy at Arcadia, but this week is one of the driving forces behind the new challenge called “Transforming Cancer Navigation with Open Data & APIs” . I caught up with Aneesh about why the need for this type of data exchange and why caner, and also more generally about interoperability, data analysis (his day job) and the impact of AI. Aneesh is an optimist but also about the most articulate person in health care explaining what is going on the ground and in policy with the regulations and actions of data exchange, and its uses. Pay attention–Matthew Holt

Lyle Berkowitz, Keycare

Lyle Berkowitz is an old friend and these days is CEO of Keycare, which provides a virtual care workforce, primarily for major health systems. It’s based on Epic taking advantage of Telehealth Everywhere, which means that patients can get to them from within their MyChart accounts and it can easily integrate its EMR data with its health system clients. It’s being used primarily for out of hours care, but increasingly primary care expansion for population health and patient outreach. I call Keycare dinosaur preservation, but Lyle tells me it’s expanding the balloon from within!–Matthew Holt