By MATTHEW HOLT

Since Saturday’s Nevada primaries, confusion seems to be reigning about how Bernie Sanders seems to be winning. Time (and not a lot more of it) will tell who actually ends up as the Democratic nominee. But the progressive side (Bernie + Warren) is doing much better than the moderate side (Biden/Butt-edge-edge/Klobuchar) expected, while we wait to see how the Republican side of the Democratic primary (Bloomberg) does in an actual vote. The key here is the main policy differential between the two sides, Medicare For All.

Don’t get too hung up in the details of the individual plans, especially as revealing said details may have hurt Elizabeth Warren. But do remember that there is one big difference between Sanders/Warren and the moderates. It comes down to whether everyone is in the same state-run single payer system (a modified and expanded version of Medicare) or whether the private employer system is left as it is, with expanded access to something that looks like Medicare (the public option) for everyone else. Note that no Democrat wants to stand pat on Obamacare “as is”. Everyone is way to the left of what Obama ran on in 2008 (or at least what he settled for in early 2009).

Why has this changed? Well there’s been a decade of horror stories. I’m not talking about the BS anti-Obamacare stories from people forced to give up their junk insurance, I’m talking about people with insurance being bankrupted or put through horrendous experiences, like this mother who was put through the ringer by various insurers when her 1 year old son was killed and husband injured in a road accident. Or this health tech CEO, who was an MD & JD and had to put $62,000 on his American Express card to get surgery.

About 3 years ago as the dust was clearing from the Obamacare implementation, the impact of this started showing up in the polls. In 2017 for the Health 2.0 conference, Indu Subaiya & Hiliary Critchley ran a poll on health policy with Zogby. To me by far the most remarkable feature was that even though Obamacare was by then more popular than not among the public, the support for single payer had gone up dramatically since 2009–in the depths of the recession.

In 2019 44% said they were utterly opposed to single payer (and 50% opposed overall). But by 2017 while the number strongly in favor had just edged up, 48% were in favor overall, with another 30% neutral or not sure. Now only 19% were strongly opposed.

Meanwhile, just a year later (October 2018) a lot of fuss was made about a poll from The Hill that had 70% of Americans supporting Medicare For All. This was the poll that had 52% of Republicans saying they were in favor of it. (Full data here). (Don’t forget that only about 30% of Americans identify as Democrats, while about 35% identify as Republicans and 40% say they’re independent). So if we are to believe that somewhere between 45% and 70% of Americans say they are in favor of single payer, almost all Democrats are. And in fact that is true. The Hill found 92% were and the Kaiser Family Foundation (KFF) shows 75%.

The issue of course is what “Medicare For All” means in reality. The KFF poll is very up to date and I can’t decide if it shows that the electorate is very confused or if the poll itself is a mess. (I highly recommend clicking though it). It basically says that Democrats want Medicare For All and want a public option while wanting to keep their own insurance (presumably many of them now have employer-based private insurance).

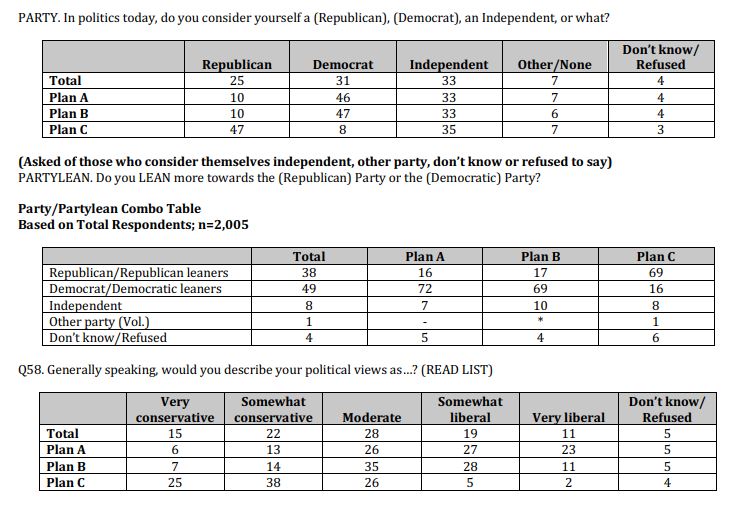

But luckily there was another recent poll done by Bob Blendon at Harvard (who I worked within the 1990s), and (as I told the KFF folks and Topher Spiro on Twitter) this poll was not a mess. In fact it was crystal clear in herding its respondents into one of three camps and thus very instructive for the Democratic primaries. (Details here) The poll gave people a straight choice between single payer, or extending the ACA, or the Republican “alternative”.

Basically when you tell Americans that Medicare For All means “Medicare for You too” (i.e. All Americans would get insurance from Medicare), but offer them a choice of an ACA expansion, roughly a third choose either alternative.

Somewhat more remarkably this split is not just along party lines. Democrats in the poll were also evenly split between Plan A (Medicare for All) and Plan B (expanding Obamacare) although few of them wanted the Republican alternative and, if you include independents who lean Republican, a third of them want single payer or extended Obamacare!

Americans’ Values and Beliefs about National Health Insurance Reform. July, 2019.

The inference is relatively clear. Almost all Democrats want Medicare (or something like it) “available” for All and about half of them (and about 1/3 of independents) are prepared to “mandate” Medicare For All.

How will that translate into the primaries? It’s relatively obvious that the most passionate and most progressive Democratic voters are a little more likely to vote in the primaries. I’ve cut some data from another poll from The Hill (Jan 15, 2020) that suggests that 58% of Democrats say they are certain to vote in the primary but 67% of liberals will, while only 50% of those who “lean liberal” will.

Which gets us back to the voting. Everything thus far is weird. Caucuses are stupid and unrepresentative, although they have elements of a good idea (2nd choice votes in multiple candidate fields). New Hampshire doesn’t look like America and neither does South Carolina. But with Sanders/Warren coming in at between 35% & 55% so far, and most more liberal and more activist Democratic primary voters favoring single payer, I suspect that we will see a majority of votes/delegates for Sanders/Warren by mid March assuming that health care stays the dominant and dividing issue.

That likely means that even if all but one of the “BBBKS” moderates drop out, there wont be enough moderate delegates to stop the progressives at the convention. (Worth noting here that Warren has been saying “Medicare For All after we fix Obamacare” which gives her a little slack).

If that’s right and Sanders is the nominee, then the Democrats face an interesting problem. If like 2018, they can run on how evil Trump and the Republicans are on health care, but not say too much about their own plan, then they’ll likely win. If Trump succeeds in making it all about single payer socialism making people fear the devil they don’t know, it’s likely to be a losing issue.

Matthew Holt is the publisher of THCB and likes to remind people now and again that he has a Political Science degree and worked for a pollster once!

Categories: Uncategorized

First, millions of low wage jobs are held by young people living at home with minimal expenses or while attending college. It’s their first rung on the workplace ladder and they learn valuable skills like being on time, working with others and taking constructive criticism. Second, automation happens when there is an economic incentive to make the investment. There will be a lot more incentive to invest in automation at $15 or $20 per hour than at $7.25. At any rate, let the states set the minimum at a rate that makes sense for them. There is a lot of difference in wages and living costs generally between NYC and NC and most other places for that matter. Let the minimum wage reflect the economic realities of each state or region.

Separately, do you know where the idea of a $15 per hour minimum wage came from? It came from some people at the SEIU kicking around the concept. They concluded that $10 was too low and $20 was too high and settled on $15 with no research on the potential impact on jobs to back it up. That’s no way to make important economic policy.

” What good is $15 per hour for those who work in restaurants that close or have to significantly cut back on employees or hours worked per week?”

What good is a job at $7/hr and no health coverage? Automation in restaurants will happen no matter what, and as the income gap widens less people will be able to eat out anyway.

But, less eating out at fast food places can only improve health.

$15 per hour is probably still not enough to support a family of four in most places. I think liberals also underestimate the amount of automation that will be introduced in industries like restaurants if $15 per hour becomes the law of the land. Also, demand in that industry is highly elastic so as menu prices inevitably rise, many people either will stop going out to eat or at least eat our less often forcing many restaurants to close. What good is $15 per hour for those who work in restaurants that close or have to significantly cut back on employees or hours worked per week?

The last figures I saw pegged the U.S. fertility rate at 1.75 births per woman of childbearing age vs. 2.11 that it would take to replace ourselves. People across the economic spectrum are having fewer children than in the past.

Yes mortgage interest is still deductible at least on loans of $750,000 or less. However, there is now a $10,000 cap on state and local tax deductions. That’s a big deal in high cost states like CA, NY, NJ, MA, etc. Maybe not so much in NC. The property taxes on our pretty small, simple house are $10,500 per year. The top NJ marginal income tax rate is 8.97% on income above $500,000 and 10.25% above $5 million. Our governor wants to lower the latter threshold to $1 million. NY’s top rate is also 8.97%. CA’s is 13.3% With the $10,000 federal cap on SALT deductions, those state income taxes are, in effect, no longer deductible against federal taxes.

“For most employees, wages in high cost locations don’t come close to reflecting the cost of living.”

Yes, certainly for those at the $7/hr wage rate. But at least higher paid workers usually also get heath care subsidy from their employer. Cost of housing is a problem all over the U.S. (and in big city Canada). Those with mortgages at least get to deduct from taxes – even those with high incomes.

Housing equity is a big problem that maybe taxes could help alleviate.

“By the way, a $15 minimum wage in Canada translates to $11.25 in the U.S. at current exchange rates.”

Not sure of your point, those in Canada don’t live in U.S. and visa versa.

“Finally, I don’t think it’s realistic to expect every low skill job like flipping burgers at McDonald’s to pay enough to support a family of four on that income alone.”

No, not even one child, but lack of responsible economic education many low education/wage workers are delusional about what it takes to raise a child. However, the religious right oppose economic and educational access to birth control. That along with no real repercussion for male sperm donors helps trap people in low a wage economy.

Is $15/hr enough to support a family of four?

For most employees, wages in high cost locations don’t come close to reflecting the cost of living. My son’s former employee relocated from suburban Chicago to Boston following a merger. He chose not to relocate but if he did, his salary would have been essentially the same but the cost of a similar house to the one he owns would cost twice as much as is current house is worth. A retail clerk at Walmart could probably afford a modest apartment in rural AK but good luck trying to find one in Northern NJ, Westchester county, NY or Long Island.

The only people for whom wages might more fully reflect the local cost of living are those for which there is a national market as opposed to a regional or local market. Even there, many doctors willing to practice in rural areas can often make more than they could in expensive cities because not many doctors or their spouses want to live in a rural area unless they grew up there and liked it.

By the way, a $15 minimum wage in Canada translates to $11.25 in the U.S. at current exchange rates.

Finally, I don’t think it’s realistic to expect every low skill job like flipping burgers at McDonald’s to pay enough to support a family of four on that income alone.

Assuming if you live in high rent areas then your income will reflect that. Certainly attracting high wage employees means that companies don’t pay standard wages which do not reflect the local cost of living.

We’re not looking to tax the money left over due to frugal living, just the money you earn.

In Ontario Canada the minimum wage went to $15/hour. An acquaintance who owns a chain of local shoe stores (inherited from daddy) complained about the cost to his business – however his lifestyle did not change. So it IS not about lifestyle for the extreme wealthy, but improving lower wage earners basic life as they don’t have a “lifestyle”.

Higher taxes are not about how it will affect one’s lifestyle. The cost of housing varies enormously around the country so $250.000 may provide a comfortable living where you live but it’s not a lot in NYC, SF and numerous other places. Besides, a lot of people like my wife and me live well below our means — small house (1700 sf), 15 year old car, etc. Does that mean I should pay more in taxes than someone with the same resources who spends most of it on a more lavish lifestyle?

The top 1% of the income distribution already pays 40% of all income taxes. I don’t think government in the aggregate meaning federal, state and local combined should be the senior partner in anyone’s life no matter how wealthy they are. For perspective, Bernie Sanders has proposed roughly $60 trillion in new federal spending over the next decade. Mike Bloomberg proposed $5 trillion in new taxes over the same period. Amy Klobuchar proposed $7 trillion, Elizabeth Warren proposed $10 trillion and Sanders proposed more than that but not nearly enough to pay for his proposals. For perspective, Hillary Clinton proposed $1.5 trillion in 2016. I support most but not all of what Bloomberg proposed and I would also go along with a VAT and a carbon tax.

Of course you don’t see the people who died prematurely from heart disease, cancer, etc. because doctors viewed their “biological age” as too old to even be offered surgery, chemo, etc. whereas in the U.S. it’s routine to offer it. Even if it’s marginally useful at best or even futile, if the patient or the family wants it, they get it. That accounts for a significant piece of America’s higher healthcare costs. So does the fact that doctors, nurses, and just about everyone else who works in the healthcare system makes 50%-100% more than their overseas counterparts.

I’ve been to Stockholm, plenty of well dressed citizens and expensive cars, nice housing no visible homelessness. All have state run healthcare. Outside of Stockholm, in the sea approach, there are islands and shoreline where many Swedes have summer homes and cottages. No, not everyone is “rich” but they live a pretty good lifestyle – from observation.

At least with a VAT you’re getting something for it – unless of course politicians choose to give it away for corporate welfare, where there are never questions of, “How are we going to pay for it?”

It’s about who can afford more taxes – certainly those at least above somewhere of $250,000. How would more taxes hurt the wealthy, keep that Escalade an extra year, maybe buy a 30 foot boat instead of that 36 foot, downsize to 4000 square foot home.

Taxes can and should go up on the wealthy, but what’s reasonable and how much money will that raise compared to what’s needed? I would support getting rid of the carried interest rule that benefits hedge fund and private equity moguls, the 1031 exchange rule that benefits real estate investors, raising the top marginal income tax rate back to 39.6%, taxing dividends as ordinary income as they were prior to 2001 and raising the capital gains tax rate back to 28% where it was back in 1986. That would include the 3.8% tax on investment income for couples who make more than $250,000 that was passed in 2013 to help pay for the Affordable Care Act. I don’t support a wealth tax or taxing unrealized capital gains. These proposals would raise my own family’s taxes significantly.

We will probably also eventually need a value added tax. The most broad based value added taxes in Europe raise about 0.4% of GDP for every one percentage point of tax rate. so a 20% VAT would raise 8% of GDP in revenue. We will probably also need to enact a carbon tax to combat climate change. A $50 per ton carbon tax would raise the price of gasoline by 45-50 cents per gallon.

I really get annoyed when I read how well a wealth tax polls. Any tax that the vast majority of people will never have to pay will poll well. It’s just another version of the famous Huey Long quote: “Don’t tax you, don’t tax me, tax that fella behind the tree.”

How will anything get paid for if we keep subsidizing the wealthy with tax breaks?

Matt, Of course it would be fairer to pay for long term custodial care with a broad based tax at the federal level. The problem is that money is a constraining resource. If there were a consensus in the U.S. raise taxes by $400 billion dollars per year ($4 trillion plus over a decade) to pay for long term care for the non-poor, we would have done it a long time ago but there isn’t.

Other developed countries with comprehensive social safety nets pay for it by taxing the middle class very heavily. People in those countries are willing to pay much higher taxes than Americans are willing to pay because they think the value they get justifies the taxes they have to pay. There is more of a culture of solidarity and a level of social trust in the government to deliver these services efficiently that just doesn’t exist in the American culture. In Scandinavia in particular, the populations are small and comparatively homogeneous whereas the U.S. population is very diverse both racially and ethnically. As a result, we don’t all think the same way culturally.

With healthcare, we need to build on the system we have to get everyone covered in a way that works for us consistent with our culture and our values. That includes a significant role for private insurance companies to ensure that people have choices even if it increases costs associated with greater administrative complexity.

Mot cheap but again wouldn’t a broader based tax payment be fairer than either bankrupting state Medicaid budgets or causing unlucky individuals and families to have to pay?

One more thing. Sanders also wants to cover long term custodial care which Medicare currently covers only on a very limited basis following at least a three day inpatient (as opposed to observation status) stay in a hospital. The AARP estimates that family members now provide long term care for loved ones that it values at over $400 billion per year. If Medicare for All covers comprehensive long term care, people are going to come out of the woodwork by the hundreds of thousands to claim benefits. How will that be paid for?

I would like to address three aspects of Medicare for All that voters need to better understand. They are (1) the favorable view of existing Medicare, (2) risks and unintended consequences of Medicare for All and (3) how to pay for it.

Existing Medicare polls well. I think the main reason is that beneficiaries pay only a small percentage of its cost in premiums. Medicare Part A is financed by a payroll tax on wage earners, the Part B premium only covers 25% of Part B costs and Part D reinsurance for costs incurred by beneficiaries who enter the catastrophic coverage zone accounts for a significant portion of Part D costs. By contrast, those with private coverage nominally paid mostly by employers is actually paid for by employees in the form of lower wages than would otherwise be paid and people with individual market insurance are paying the premium themselves except for those who qualify for subsidies under the Affordable Care Act.

Most current beneficiaries with regular fee for service Medicare say it works well for them. Providers, by contrast, say Medicare’s payment rates don’t fully cover their costs. Hospitals resolve this by shifting costs to the large commercial insurance sector that exists today but would disappear under the Sanders and Warren versions of Medicare for All.

With respect to risks and unintended consequences, neither Sanders nor Warren have any idea how much utilization will increase once medical services are free to patients at the point of service and the currently uninsured and underinsured are brought under Medicare for All. They also have no idea how many older doctors will accelerate their retirement because they don’t want to accept a significant reduction in their income once higher paying private insurance is pushed out of the system. They have no idea how many aspiring doctors will decide not to go to medical school because the cost of their training in both money and time is no longer worth it financially. Finally, they have no idea how many hospitals will close because they can’t cover their costs from Medicare reimbursement rates or will at least eliminate some of their less profitable service lines. Who knows what will happen to wait times for non-life threatening care like hip and knee replacement surgery?

Finally, with respect to financing, Sanders and Warren think we can pay for Medicare for All mostly by drastically raising taxes on the, including a new wealth tax, and everyone else can have a largely free ride or, as Sanders claims, at least will save a lot of money by no longer paying premiums, copays and deductibles in exchange for a modest 4% payroll tax on income above $29,000. Yet all the other developed countries with universal coverage, whether they use insurance companies or not, pay for their comprehensive safety net by heavily taxing the middle class. France, for example, raises 18% of GDP from payroll taxes vs. 6% in the U.S. The European countries have value added taxes averaging north of 20% with rates as high as 25% in Scandinavia. We don’t have a value added tax (yet). Indeed, a typical middle-class person in these countries pays about 50% of gross income in combined income, payroll, value added and property taxes. At the Same time, Sweden taxes corporate profits at 19% and its top capital gains tax rate is 30%. There is no wealth tax there either. The financing proposals offered by Sanders and Warren are disingenuous, in my opinion, and unlikely to work without raising taxes significantly on the middle-class.