Call it what you want, disruption or evolution, but when two of the largest for-profit hospital chains, HCA Healthcare and Tenet Healthcare, and one of the largest insurance intermediary services companies, Optum (part of UnitedHealth Group), invest billions of dollars in capital for building new care settings, everyone should take notice. From freestanding ambulatory surgery centers (ASCs), to urgent care centers, to retail pharmacy-sponsored clinics and employer co-located clinics, the disruption of care delivery is all around us.

How does General Community Hospital compete with Walmart, CVS and Walgreens (retail clinics)? How does it compete with Urgent Care Centers? How will it compete with freestanding ASCs? How does a hospital stop consumers’ desire for savings and convenience? How does it stop physicians’ own desire for convenience and efficiency? This is the disintermediation of hospitals in a very big way! General Community Hospitals can zero base care, but they need to have answers more in line with a consumer retail operation than those of a charity. How many product lines does a focused factory operate?

I joined Bill Simon, former CEO of Walmart, to learn more about the potential and continued disruption of the US Hospital industry. Hospitals and Walmart? Yup!

Simon underscored several key points about health care disruption and the potential impact of ambulatory surgery centers on US hospitals.He said, “The real learning is that in health care, as in the rest of the economy, when price matters, consumers respond.” Simon was the architect of Walmart’s $4.00 generic drug pricing initiative and introduced health care consumer initiatives as CEO. He went on to confirm that: “$4 Rx worked for most generics because the cost of goods is low. There were some economies of scale…and some supply chain benefits but the math works on its own. You have to zero base the equation.” He added.

We all have been tracking the migration of care for decades, yet now we are seeing surgically complex cases moving to the ASC environment. Most ASCs are now reporting on quality placing them in the center of the Value-based purchasing equation, especially due to an ASC’s lower rates of reimbursement (ASCs receive about 55% of what a similar hospital-based procedure is paid for the same service by Medicare). Can they further “zero base the equation”? Focused factories for routine care are the future of care delivery, yet every market is different and developing at different rates. The winners will be communities across America, and whichever provider wins in those markets will be determined by share.

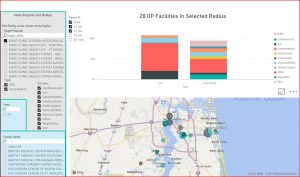

We used our FranklinBI™ platform to learn about market differences.

Summarized in visuals below are The Mayo Clinic’s Jacksonville, FL. and Phoenix, AZ. Markets. The markets are different in population size, with Jacksonville being about half the size of Phoenix, yet the service location mix is quite different for the same service lines in the two markets:

Each market has a unique story and the detail is found at the hospital and ASC level, by service line, one community at a time.

In the Top 50 largest U.S. markets there are three types of evolving markets:

1) Advancing markets where ASC penetration is well past the 60% of market share (n=14),

2) Converging markets representing the largest segment with penetration at 40-60% (n=23),

3) Opportunity markets where ASC share is below 40% and ripe for development (n=13).

As we evaluate markets across the country, we see many of the largest markets in 60/40 or 40/60 splits. These are Converging Markets or transitional. Opportunity knocks big or hurts hard depending on which side of that equation the ASC or Hospital-based provider rests. A swing of 20 points is big business especially in NYC where the 40% is the ASC share. There is empirical proof that the shift is setting new records. San Jose, Memphis and Ft. Worth are good examples where ASC locations break records for successful migration from hospital-based setting to freestanding ASCs; these are the Advancing Markets.

The Opportunity Markets are notable exceptions to the 60/40/60 in markets like Chicago, San Antonio, Detroit, Boston, and many more where the potential upside for ASCs and further hospital-based outpatient migration to ASCs is significant! These markets have patients getting care the old fashioned and expensive way. Whether a health system looking to lower costs or an ASC operator looking to grow share, these are the green fields of disruption.

The greatest insight for hospitals and ASC operators is that some of the largest hospital-based volume markets have very low ASC market penetration. While this may speak to the brand and relationship referral control hospitals have over physicians, these markets are also ripe for disruption on economics. Chicago, Detroit, Boston, Long Beach and Cleveland are a few prime markets for ASC operators to target for development. These same markets are “at risk” for hospitals depending on those elective service lines.

There is no question, major markets have already moved. The pace is accelerating with hospital-based ASC median revenue up 41% year over year. The complexity of cases will continue to advance making further inroads into what was exclusively hospital-based delivery. Consumer and surgeon sentiment on price/convenience, along with economies of scale will continue to disrupt the US Hospital industry. Narrow insurance networks, high-deductible health plans and federal value-based payment programs will also lever local market migration. Can or will Optum, Tenet or HCA become the Walmart of the ASC industry? Can they or will they zero base the equation to further their own cause?

Change or be changed. This time the influencers are less about quality and more about convenience and cost. As WalMart’s Bill Simon said, when price matters, consumers respond. Economies of scale, supply chain efficiency, focused factories and retail thinking about price and convenience all apply to this evolving sector.

John R. Morrow is Managing Director of Franklin Trust Ratings, a business intelligence company helping health systems to grow by finding new opportunities in markets across the US.

Categories: Uncategorized

UNH is an insurer. That is the credit they deserve. They didn’t create ASC’s and they don’t treat patients. They are paid to take risk (an important task). That is it.

With respect to ASC’s, if more patients can SAFELY get their surgical procedures there instead of in a more expensive hospital, it certainly saves money for self-funded employer customers and can save money for patients if they have a tiered network that offers a lower copay or even a zero copay for going to an ASC instead of a hospital. Insurers are well aware that employers want to see the growth of healthcare costs and health insurance costs slow and so do individual patients who either buy their own insurance or are being asked to contribute more from their paychecks toward their ESI coverage. If UNH is successful in doing all that, employers and patients will save money, UNH will grow its market share and their shareholders will benefit too. The only losers will be hospitals which will lose some of their more profitable business. UNH is part of the solution whether you want to give them any credit for it or not.

“People don’t typically choose their healthcare.”

They certainly do. They choose doctors, when permitted to help them. When they are unhappy with what they hear and think there is a better answer they go to another doctor. Most of the times physicians are pretty good so patients generally follow their advice.

“Actually UNH is in the process of acquiring ”

Barry, that is correct. They are in the process of buying these ASC’s, not creating them but attempting to better monetize them for the benefit of their stockholders. They are doing very little innovation and not doing that much to save money for the taxpayer.

They are insurer’s. That is their role. They do not exist to save money and when they do that frequently means patients are being denied treatment.

Actually UNH is in the process of acquiring Surgical Care Affiliates, a chain of ASC’s and UNH already owns Med Express which is a chain of urgent care centers. It’s superior access to capital will help both chains expand faster than either could on their own. Moreover, the use of tiered networks which offer lower copays or none at all in exchange for using more cost-effective high quality providers helps to steer patients in a direction that mitigates healthcare cost growth. UNH has an innovative, entrepreneurial culture. It didn’t get to be as big and successful as it is without doing something right.

People don’t typically choose their healthcare. They rely on doctors to tell them what they need whether they have ESI or bought their own insurance policy. If you tell a patient you can have a $200K cancer treatment and have a good chance of sending the disease into remission or you can skip the treatment, save your $10K deductible and probably die within three months. Your choice, Mr. Patient.

Sure people can save on insurance premiums if they buy a plan with skimpier coverage which means not just a higher deductible but a narrower breadth of coverage as well. Suppose they decline the alcohol and drug abuse coverage or the mental health benefits because they think they don’t need either one but then need them later. Well tough. You made your choice and now you have to live with it.

Exactly. So simple. So powerful. Works in every domain…even complicated areas such as purchasing computers and financial services…(not to mention orthodontia and plastic surgery and lasik)…costs go down, innovation goes up and improves quality…. but our experts tell us it won’t work in health care!

“I think you overestimate the potential of high deductible insurance plans and fewer state coverage mandates to reduce healthcare costs.”

People have a vested interest in keeping their costs down. If it makes them feel good to pay more than necessary that is good as well. People spend money on less important things.

For some reason if the restaurant is free I don’t bother ordering the turkey hamburger for $10, I’ll go straight for the NY Strip steak at $60 with lobster as a side dish and some expensive wine. Why do you think that is not true in healthcare? In the early years when a lot of patients paid cash if I offered them the latter meal instead of the turkey hamburger they would walk out of the office. Yes, high deductibles would work fine to reduce prices. So would co pays on certain expensive treatments. But we need the individual to be purchasing their own insurance, not a third party doing so. I think most people would choose the lower priced insurance than my steak and lobster insurance at 8 times the price, don’t you? That might mean the most expensive care may be unavailable for free.

Just think of Peter from this list. He even flew to India to get a better price on his surgery.

I think there is plenty of potential for practice patterns to become less testing-intensive if we got sensible tort reform that physicians perceived as objective, consistent across jurisdictions and fair to them.

Just as Steve2 says that I underestimate the role of money and profit in medicine, I think you overestimate the potential of high deductible insurance plans and fewer state coverage mandates to reduce healthcare costs. Can I prove it? No, Fee for service creates incentives to overtreat patients and capitation creates incentives to undertreat them. There is no perfect solution.

Barry, I was waiting for your reply. Since you didn’t I will tell you that United Healthcare might have helped reduce the hospital costs by reducing hospital days, but United Healthcare wasn’t the real cause.

The researchers and the physicians along with their investors were. The former set up the ability for the insurer to push people in a less expensive direction. United Healthcare didn’t set up out patient surgical centers. The physicians did and that benefited the bottom line of United Health who took advantage of less expensive costs.

The one area where these insurance companies pushed lower costs a trifle faster was in the hospital length of stay. However it was not that great a saving for they reduced the unnecessary days that were inexpensive. The expensive days remained and when that was done the prices of the expensive days had to rise. I won’t bother to go into all the costs that increased because of these actions. There is a good likelihood that these cost saving measures actually contributed to ever rising costs.

Barry, the point was that costs need to come down, but the treating physician’s component of those costs do not alter the problems we face. The overpayments being made come almost completely from somewhere else. Though some physicians are probably overpaid, lowering the over all physician reimbursement doesn’t solve problems. It creates them.

The problems start with the laws regarding healthcare that stimulate spending. Change those incentives appropriately and healthcare costs will rapidly fall.

Very unusual: you and I think alike with two disclaimers. 1. Our ideas about what to do about this differ and 2. Even if it was $0 I would not get excited about a colonoscopy!

Allan – I think you and Steve2 are focusing on a different question than I am. You and Steve2 are looking at a breakdown of costs that comprise our total healthcare system which now amounts to north of $3.2 trillion, I believe or just shy of 18% of GDP. The National Health Expenditure Data shows that the category called physician fees and clinical services comprise approximately 20% of total health care costs. In this context, as I understand it, clinical services include non-hospital owned imaging and labs, physical therapy and rehab. The NHE data also pegs hospital costs at around 31% of total costs, prescription drugs at 15% of total costs though drugs dispensed in hospitals get buried in the hospital category of expenses and insurer administrative costs at about 5% of the total.

The question I’m focusing on relates to the key drivers of health INSURANCE PREMIUMS paid by individuals, employers and government payers. As I noted previously, medical claims account for 80%-90% of the health insurance premium dollar with administrative costs and profit (if any) accounting for the rest. Any health insurance executive will tell you that their medical claims break down as follows: 40% for hospital based care including outpatient services with ER care and admissions under observation status counting as outpatient care; 40% for physician fees and clinical services, which includes non-hospital owned imaging, labs, and physical therapy and 20% for prescription drugs. The Medicare claims breakdown is roughly similar by the way but Medicaid is not because a large chunk of its spending is for long term custodial care.

If traditional health insurance doesn’t cover long term custodial care in a nursing home or assisted living facility, dental care, routine vision care, hospital construction, medical R&D financed by NIH and philanthropy, public health initiatives paid for by the CDC, etc. those costs aren’t relevant to the determination of health insurance premiums but they are quite relevant to the calculation of total healthcare costs across the economy.

I hope that provides some clarification. It’s frustrating to talk past each other.

The experience in my market is that anything a hospital owns is there to stifle competition and feed the main hospital beast. Prices go up in comparison to truly independent operators. I avoid any provider who has a connection to a hospital – but it’s getting harder and harder to find that.

Walmart’s $4 generic price is good, but it works because Walmart has lots of other stuff to sell you. Let me know when Walmart offers the $500 colonoscopy, then I’ll get excited.

Steve, your number differs from mine, but based upon the CDC, I see a 19.9%

https://www.cdc.gov/nchs/fastats/health-expenditures.htm

“ • Percent of national health expenditures for physician and clinical services: 19.9% (2014)”

I am not sure what encompasses clinical services. So I did another search and found the numbers all over the place, more around the number you suggest than the CDC. One of the lowest was:

https://www.jacksonhealthcare.com/media-room/news/md-salaries-as-percent-of-costs/

“ At eight percent of total healthcare costs, if physicians worked for free we would still have a serious cost problem,” said Richard L. Jackson, chairman and chief executive officer of Jackson Healthcare. ”

I don’t know how to justify the variety of figures so I have to conclude that the true number is somewhere between 8 and 20%. If you have a handle on these numbers perhaps you can add a bit more. Maybe the 8% represents the physician gross salary.

One additional source is Professor Reinhardt from Princeton. In a letter to the editor at the NYTImes he said: “If we somehow managed to cut that take-home pay by, say, 20 percent, we would reduce total national health spending by only 2 percent, in return for a wholly demoralized medical profession to which we so often look to save our lives. It strikes me as a poor strategy.”

http://query.nytimes.com/gst/fullpage.html?res=9B00EEDE163AF936A3575BC0A9619C8B63

Well outside of Philadelphia. Your summation is not totally unfair, but i think you underestimate the influence of money on medical decisions. Suing after something goes wrong is the traditional American way, but not my favorite. I would rather this shift to larger cases in ASCs be driven by physicians and patients as a way of providing better and or cheaper care, rather than by the for profit centers. Also, the Medicare supplement to Critical Access hospitals was cut with the Balanced Budget Act and many of them are in trouble.

Steve

A better metric I believe, is to look at how health care dollars are actually spent, rather than what insurers tell you. If you do that you see that physician pay accounts for about 7% of medical dollars (14% goes to professional fees, but half of that goes to expenses).

http://content.healthaffairs.org/content/35/7/1197.full?ijkey=n0Mmz2.8MzoLA&keytype=ref&siteid=healthaff

Barry, you can look at things anyway you want, but that doesn’t mean those numbers are meaningful. That is a big problem with your view of healthcare. You think an abstract number represents reality when it only represents a number contrived to produce a desired result.

I will go by Uwe Reinhardt’s number, 20% which I believe approximates a raw number. If you wish to make it a different number go ahead.

OK Barry, United Healthcare has had more success in reducing the number of bed days than other insurers. But, the question is are they really the force behind the reduction in the use of hospital beds or is there a more important cause? Let’s see if we can’t bring you from abstract numbers to reality.

Steve,

I don’t know what UBER disruptive healthcare will look like, but I agree with Allan it can’t come out of primary care doc reimbursement. It will not be another replication of insurers establishing/negotiating with docs in each region. It will likely include some combination of one or more of the following:

*some way to get out of covering the balkanized and corrupt (buying off state politician) state mandates.

*association plans.

*retail clinics (Walmart, CVS ???).

*direct primary care.

*elective surgery (knee etc) at regional centers…perhaps with travel expense reimbursement.

*reference pricing.

*a return of indemnity plans.

*a Nortin Hadler style plan that only pays for regimens established (via RCT or otherwise) to have net benefit for patients. see Hadler’s By the Bedside of the Patient for his latest ideas.

*Health Savings Accounts patients can use for non verified regimens or things like plastic surgery.

*some kind of significant tort reform.

*slimmed down insurer operations so the insurer can operate with less than 10% of medical costs (unlike the today common 12-14%).

*elimination of EHR mandates, ending the billions going to products not ready for prime time.

*others tbd.

The State commissions and the regional quasi monopolies that represent health insurance today are ripe for a disruption.

United Healthcare. They seem to have had more success in this area that competing insurers and standard FFS Medicare.

Medical claims typically consume 80%-85% of the health insurance premium dollar and they can approach 90% for some of the non-profit Blues. Physician fees and clinical services are 40% of medical claims. The same holds true for Medicare but not Medicaid for which long term custodial care is a huge part of that program. No patient can acquire a prescription drug, aside from samples, without a prescription from a doctor and patients don’t get admitted to the hospital, even for observation or imaging, without a doctor’s order. They drive virtually all healthcare spending paid by insurance and it’s a perfectly sensible way to look at it.

“It has steadily reduced”

Who is this it you are talking about. All of these things are eventually effectuated by physicians sometimes forced by their employers whether the employer be a government agency or private business. AS Kip Sullivan says in another thread you guys are always adding up one side of the equation and forgetting about costs on the other side.

The 20% represents the %costs of physicians plus some other non M.D. services such as naturopaths and probably dentists. While it may not represent the breakdown of insurers, insurers fund most of the physicians income. Whether the costs are paid by government or the insurer it is the taxpayer and patient that are ultimately paying the bill which is provided by M.D.’s and D.O’s. It is rather inane to look at things in the fashion you are doing for without the physician care is not provided.

I know you like Uwe Rheinhardt so I refer you to an article he wrote for the NYTimes where he said pretty much the same things I am saying now. He is better at writing and he is considered an expert, but I don’t remember him ever saving the life of a patient.

The big challenge is to find ways to more efficiently manage care especially for the high utilizers and for those with chronic conditions like CHF, diabetes, asthma, COPD, and depression.

Hospitals are getting into the insurance business and traditional insurers are getting into the provider business. For example, United Healthcare has acquired its way into both the urgent care and ASC business and a number of years ago, it bought the Southwest Medical Group in Las Vegas.

It has steadily reduced its number of inpatient bed days per 1,000 members by moving more care from inpatient to outpatient and now it’s working on moving more care out of the hospital altogether. We’ll have to wait and see how it all plays out.

“Remember physician and certain non-physician costs contribute less than 20% to healthcare costs”

Allan, commercial insurers will tell you that their medical claims break down as follows: 40% hospital care (inpatient + outpatient combined); 40% physician and clinical services, and 20% prescription drugs. Moreover, as I’ve noted numerous times before, doctors’ decisions to prescribe drugs, order tests, admit patients to the hospital, refer patients to specialists, consult with patients and perform procedures themselves influence or drive virtually all medical care that shows up as medical claims to be paid by insurers, Medicare, Medicaid, VA, and out-of-pocket by patients.

The 20% figure that you cited, presumably from the National Health Expenditure data, includes dental care, long term custodial care, hospital construction, R&D, insurers’ administrative costs, etc. none of which factors into medical claims.

There are many other ways of reducing costs than just cutting your fees. Remember physician and certain non physician costs contribute less than 20% to healthcare costs. If physicians overhead is 50% (some suggest more) and they are taxed at 35% (perhaps more) that leaves 7.5% to play around with. The big money can’t possibly come from physicians which is the only group with the license to practice medicine.

Interesting question. Physician only practices dominate several areas of the country. The docs there make the same, as far as I can tell, as docs in areas that use the care team model. That said, there actually is a history, I know of several places, where in the past unethical docs found ways to “supervise” 8 or more rooms at a time to make a fortune. That is gone. At present there are clearly places that supervise at a 1:4 ratio to maximize income when they should be doing so at a lower ratio, or so I believe. (Overall, I think the choice to use the care team is probably more cultural than anything. That, plus lifestyle since I have done both.)

However, in the case of the surgicenter, there are ones owned by anesthesiologists and ones where they are also partners. That puts them in direct financial conflict also.

Of course they don’t want ambulances pulling up, especially at midnight. They wouldn’t have anyone there. It costs tons of money to have people just hanging around in case someone comes in.

Steve

The thing that stops selling across state lines is barrier to entrance. When that new insurance company wants to sell its insurance at half the cost of everyone else, it needs to actually sign up providers. We aren’t cutting our fees 50% just to help out a new company with no record of reliable payments.

While no system is perfect, my take after listening to this back and forth from those “in the trade” is as follows:

Shifting more procedures from hospitals to ASC’s or at least from inpatient care to outpatient care is good for payers and that trend should be encouraged to the extent that it can be without compromising patient safety. My sense is that most doctors in America are well trained, ethical, competent and they try to do the best they can for the patient in front of them. While there are bad apples in every profession, I don’t think doctors go into medicine to become wealthy. I believe they see medicine more as a calling and a chance to make a positive difference in patients’ lives. If they wanted to get rich, they could have gotten an MBA and gone to Wall Street or into real estate and made more money faster and with a lot less time spent in training.

If surgeons send high risk patients to ASC’s who should have their procedure done in a hospital, they could be sued if complications cause harm that could have been quickly resolved or at least mitigated in a hospital. Also, as word gets around, primary care doctors will stop referring patients to them.

The number of inpatient hospital beds per 1,000 of population has been in secular decline since the end of World War II and that trend is continuing. That’s a good thing. In theory, hospitals should be able to price their outpatient services at a level that’s competitive with non-hospital owned entities. High hospital costs relate primarily to the need to provide inpatient care and emergency room care around the clock seven days a week. Those services cannot be accessed elsewhere, especially in the middle of the night and they should command a premium price.

Medicare already pays rural critical access hospitals above normal rates so they can stay in business despite often very low occupancy rates if they are the only such facility for miles around. Subsidies could be provided on a more limited and selective basis in more heavily populated areas if necessary.

By the way Steve2, didn’t you mention in the past that you are an anesthesiologist and are part of a large group practice in the Philadelphia area?

“for profit ASC chains, to push larger surgeries out into ASCs. ”

Yes, that sometimes happens when we permit non M.D.’s or M.D.’s that are primarily businessmen to practice medicine. Aren’t ACO’s being created so that the primary patient responsibility of the physician will not include such decisions? Then the bean counters can make these type s of decisions without considering patient safety.

Steve, do you really think the surgicenters want to have ambulances pulling up to their doors? That would kill business so it is in their best interests financially to treat only those that can safely be treated in the OP center. Where quality falls we frequently see the same quality failures in the nearby hospitals.

Should M.D. anesthesiologists use nurse anesthesiologists in hospital operating rooms? They do so that M.D. anestesiologists can earn more money. Isn’t that correct? Isn’t that the financial gain you are so worried about?

Steve, I think I introduced the UBER analogy…and my example was 15 years ago. I still think it is pertinent…..things move in very very slow motion in health care system creative disruption. Should cross state line competition come to pass with ways to avoid state regulators it will accelerate….for better or worse (better in my opinion).

“Likening ASC’s to UBER as a disruptive force to a long established market and system”

You realize, I assume, that ASCs are not new. There is a lot more that can safely go out to them. A lot more that should. What you won’t know if you aren’t in the trade is that there is a big push going, especially among the for profit ASC chains, to push larger surgeries out into ASCs. In some cases that can probably be done quite safely. The larger ASCs, especially those adjacent to a hospital or on the same campus really aren’t that much different than a hospital in their capabilities. (Though you do need to be careful as the hospital may call it an ASC and still bill at hospital rates.) What is going on out here in the real world is the chains are now trying to push those larger procedures out into the smaller 2 OR ASCs. Not really the same animal, and there is a real lack of data on safety in these situations. With good patient selection it likely ends well, but what is really happening is that you have the constant push, I think every ASC administrator works at least partially on commission, to push the envelope on how sick a patient you can do at the ASC.

Steve

And you take these lap chole patients back to the ASC when they have problems at midnight? I don’t think so. I am not saying that docs are bad guys, just that this is profit driven. (What is the ROI at your ASCs? I know what it is at the ones we cover, at all of the hospitals in our network, and for every hospital within 30 miles. Guess which facilities have the best profit margins?) Most of this is probably good. I can’t think of a really good reason why any elective colonoscopy should ever done in the hospital given the cost difference. However, the more we push out to ASCs, the more we run into safety issues because of the money conflicts. It is nice that Allan’s consultants sent their sick patients elsewhere. It’s not like that everywhere.

” Stop making the physicians the bad guys.”

Ditto again.

Hospitals have abused patients for years. They charged extraordinary prices for outpatient care and expected the patient to pay. Radiology care at hospital outpatient departments originally were not limited what they could charge by Medicare. Many hospitals charged unbelieveable rates because Medicare would pay a fixed amount but the 20% co pay came off their actual billing rate. That caused outpatient radiology centers to grow in my area and the costs dramatically fell and patients weren’t left hours on stretchers. This competition caused the hospitals in my area to suddenly become more reasonable.

My consultants, despite owning a portion of the surgicenter, sent my high risks to the hospital. If they didn’t and thought of their own pockets first I would never send them a patient again.

The other area of concern in hospitals especially for Medicare patients were and still are consultants called in on emergency conditions; radiologists, pathologists (in the earlier years) and anesthesiolgists. They all had one thing in common. Not much face to face with the patient and the primary care doctor didn’t have much choice.

” My cardiologist sends patients outside of that system”

Your doctor is likely older, used to his way and recently bought out. He likely has a contract and his next step may be retirement or at least slowing down so he doesn’t have to worry too much about taking heat. The younger ones do.

Even if a surgeon has a financial interest in an ASC that is not owned by a hospital system, it seems that our very litigious society by itself should be a meaningful deterrent against knowingly sending a high risk patient to an ASC for a procedure that should be done in a hospital setting just so he/she can make more money.

As I’ve experienced first-hand since my cardiologist’s small group practice was sold to a hospital system in NYC several years ago, the hospital exerts considerable pressure on all of its salaried doctors to keep as much care as possible within its own system. My cardiologist sends patients outside of that system for surgical procedures all the time when he thinks they would be better served by a more experienced surgeon who is affiliated with another hospital system whether he is in independent practice or not. He takes heat from the administrators for doing it but he does it anyway. He did it for me when I needed an ablation in 2015 and I’m grateful that he did.

To this day, Medicare’s payment system is basically designed to reimburse for costs. That’s why it pays hospitals more than ASC’s and independent doctors and independent imaging centers for everything including primary care visits, simple cardiac stress tests and CT scans even though the potential for complications is presumably not an issue of concern.

Finally, even if all of the simple and low risk surgeries that can SAFELY be done outside of a hospital are done in an ASC, it’s a good thing if it saves money for the healthcare system and for payers including individual patients. If well run hospitals are struggling financially after that happens due to either a too low occupancy rate or a poor payer and case mix or all of those and it would be desirable to have the hospital continue in business instead of downsize or close, the state or federal government or both could subsidize it. Likening ASC’s to UBER as a disruptive force to a long established market and system is appropriate and it’s needed, in my opinion.

Ditto etchory. Takes me back 15 years when I was on the Board of a Blue and a corporate executive. The orthopedists in town were proposing an ASC and the Hospitals and the Blues were opposing it. I argued at the Blue meeting how can you advocate for the Hospitals when the ASC’s were going to charge more than 50%-60% LESS for the same procedure/condition?…..the same old arguments about the fact Hospitals use the huge profits in this area to fund money losing areas (like soaring glass and marble lobbies?….no, I didn’t really say that back then…kind of wish I had). This episode is when I learned the insurers were originally set up as a mechanism to fund hospitals and that they still act this way. ASC’s were and are a kind of mini UBER….disruptors. We need more to drive a focus on value and efficiency in our medical spending.

I am in awe of your clarity that physician ownership is responsible. Full disclosure, as a 63 year old surgeon who invested in a joint ownership PSC with a hospital that is now my employer my naive eyes were opened when I started to receive dividend checks. From my perspective the hospitals have made enormous profits for years on the work of physicians who admit and care for patients. The fact that the fee for an elective cholecystectomy is $17,000 at the hospital and $9,000 at the PSC is driving this more than physician greed. Stop making the physicians the bad guys.

Just to be clear, this is not being driven by pt demand, but rather by physician ownership of these facilities since they make money off of these places. I think there is a lot that can be done at ASCs and we can see cost savings. However, as bigger and bigger cases are being done at these places I see many safety concerns. You are placing the profit motive up against what is safe for the patient. Depending on who owns the surgicenter and how much money is involved often determines what is done rather than what is safe. (Unfortunately a lot o the literature being generated on ASCs and safety comes from “surgicenters” attached to or on the same grounds as the hospital. Not really that applicable to so many of the 2 and 3 OR ASCs.)

On the flip side, I am still not sure what this does to hospitals. If all of the cheap and easy cases are going to the ASCs, that leaves the expensive and difficult ones for the hospitals, yet they aren’t seeing increases in reimbursement.

How many doctors who operate in ASC’s also operate in hospitals? If the doctors also have an ownership interest in an ASC, they will presumably steer as many patients there as they can at least if those patients are low risk and have good or at least satisfactory insurance.

To the extent we can safely drive care out of hospitals or at least from an inpatient to an outpatient setting, we should do so to lower costs without sacrificing quality of outcomes or patient safety. Payers, for their part, should adopt site neutral payment so hospitals and doctors owned by a hospital system are paid no more than payment rates for doctors in independent practice doing the same work and ASC’s and independent imaging centers providing similar services, tests and procedures.

The economics of hospitals are driven primarily by occupancy rates since they have high fixed costs. They should command a premium price for care that can only be safely provided in a hospital setting but as technology advances, the number of inpatient beds per 1,000 of population needed to serve the marketplace should continue its long term secular decline and that will be a good thing in my opinion.

No! No! No! Haven’t you heard the decades old mantra: “health care is different and can’t respond to normal market economics”! ….we need legions of bureaucrats and policy experts and price setting bodies and regulators to manage the whole thing….don’t we?

Health Savings Accounts and the development of ambulatory surgery centers show that slowly, but surely, if we can remove the artificial barriers we can unleash market forces to enhance accessibility and quality and price.