I was asked to see an unfortunate elderly man – Harry – one afternoon. He had multiple coronary stents placed for coronary disease over the course of the last ten years, and after presenting with difficulty speaking, was found to have a brain tumor. The neurosurgeon was hoping I could provide some reassurance about how healthy his heart was to undergo an operation. An assessment revealed him to be high risk for a coronary event, and I had a lengthy discussion with the surgical team, and the patient, who elected to proceed with the surgery. Three hours after the surgery, the nurse practitioner taking care of the patient messaged me to tell me his heart rate was slow – ‘in the 30’s’. I was driving to another hospital, and when stopped, messaged back asking for an electrocardiogram to be sent to me. A quick glance at the image on my screen had me turning around. There are three major arteries that feed the heart. One of Harry’s arteries had closed off.

Sure enough, on arriving at Harry’s bedside, he appeared mildly uncomfortable and had the same symptom that had preceded his other three heart attacks – left shoulder pain. This created a difficult situation – he needed his artery opened, but he had just had major brain surgery. Opening coronary arteries whether it be via catheter or with clot busting drugs requires significant thinning of the blood – a recipe for disaster in someone hours removed from major brain surgery. So I elected to do nothing, and had a long discussion while I still could with Harry about the predicament he was in and what to do in the event his heart were to stop beating. There is little that is unique about the decision faced here. This is what cardiologists do – weigh risks and benefits of procedures before recommending them. Interestingly, economists believe there are factors beyond medical appropriateness that are influencing these decisions.

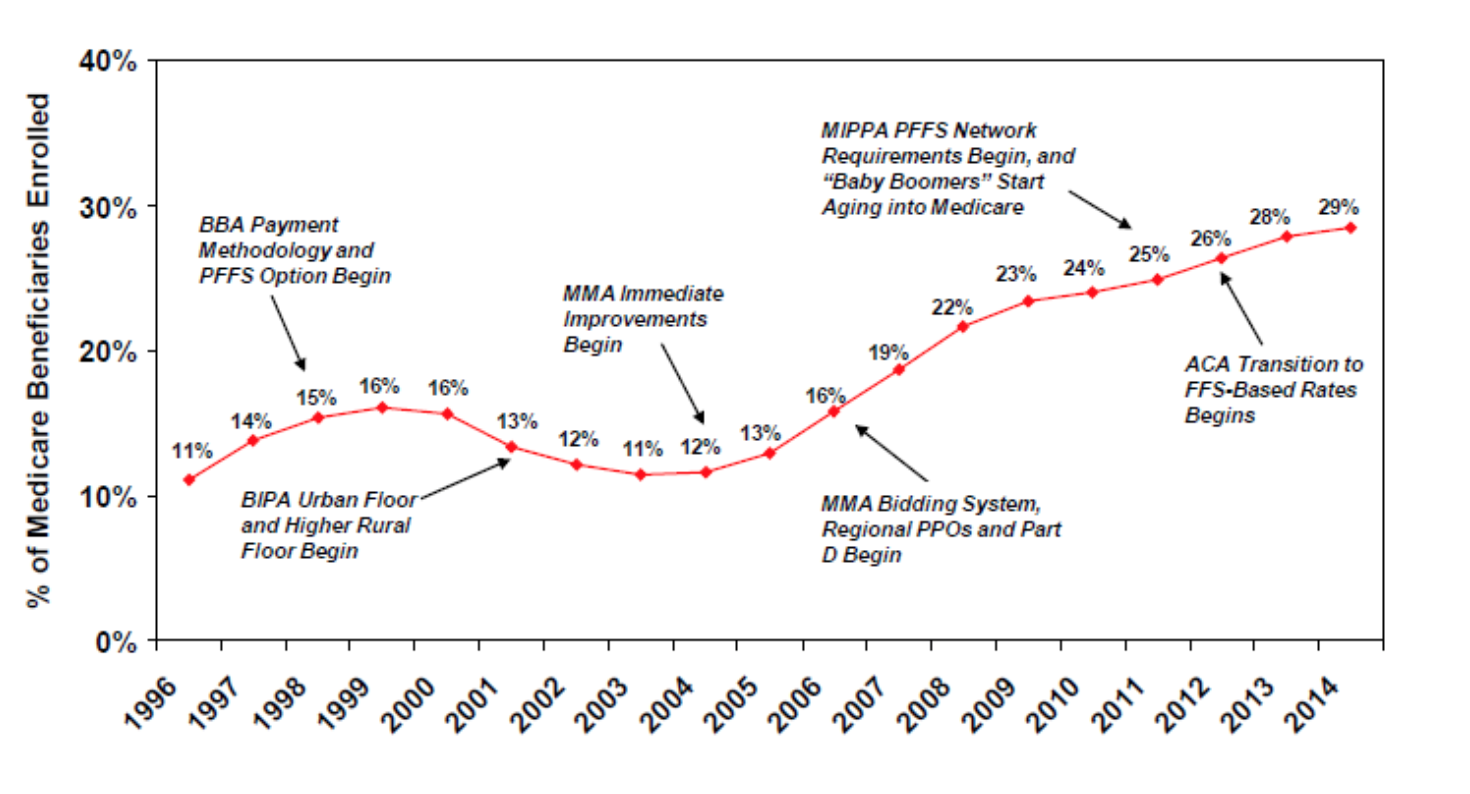

The theory arises, not surprisingly, far from Harry’s hospital room , and arises from an attempt to explain an unprecedented recent moderation in Medicare spending. Medicare spending per beneficiary is not just flat, but appears to have reduced from 2012 to 2014.

The explanation that appears to be gaining ground in academic circles driven by analysis of Medicare data is that cost moderation may in part be a result of increasing penetration of Medicare Advantage plans into local markets. For those blissfully uninitiated, Medicare Advantage (also known as Medicare part C) is the alternative to traditional Medicare for seniors. Medicare advantage means that private insurance plans are paid a fixed fee by the government per participating member. Unlike traditional fee-for-service medicare, the medicare advantage plans are somewhat more parsimonious in their payments to providers, and in theory cost saving accrue to the health care system as a result. The only problem with this story is that starting in 2003, MA plans get paid more by the government per member than traditional medicare. The higher payment coincided with an explosion in the growth of MA plans, and now about one-third of the medicare market belongs to MA plans.

The overpayment is not a small number – it is estimated that the overpayment in 2009 amounted to 11 billion dollars. While the overpayments have reduced more recently, even in 2014, the total estimated overpayment is 10.5 billion dollars (assuming 15.7 million MA enrollees, Overpayment 106%, 2014 per capita medicare spending $11,167). This is a particularly impressive number because patients in MA plans are generally healthier than traditional medicare, and actual MA plan outlays to health care providers per beneficiary are lower than traditional medicare.

Since the explosion in MA growth co-incides with the moderation in costs seen in traditional medicare, some seek to link the two by suggesting that growth in cost-efficent MA plans is actually creating a ‘spillover’ effect that causes cost slowdowns in traditional medicare.

Spillover theory holds that the efforts of MA plans to restrict growth by using restricted provider networks, forcing prior authorization for imaging, and not allowing payments for expensive treatments actually causes fundamental changes in practice patterns of providers. So a cardiologist that is forced to do a less expensive stress test on a medicare advantage patient will also start ordering less expensive stress tests on traditional medicare patients he/she happens to be seeing. Of course, you cannot prove this. But you can certainly try.

A number of studies have sought to validate this theory, and Austin Frakt of The Incidental Economist fame provides a great summary here. Most recently Ashish Jha from the Harvard School of Public Health published a paper in Health Affairs that supported the spillover effect by demonstrating that in certain counties, high MA growth was associated with lower spending growth in traditional medicare (TM). This paper is the latest in a series of papers supporting this, and there appears to be growing consensus among policy elites of the phenomenon. I was curious when I read this, because it strikes me as a theory that is easy to posit, but very difficult to prove. In an effort to understand how this seemingly herculean proof was accomplished, I decided to look at the evidence base for this more closely.

The recent paper in question by Jha et al., painstakingly divided all the counties in the United States into quartiles based on the baseline level of MA penetration, as well as the growth of MA penetration. Average baseline MA penetration ranged from 0-5.7% (quartile 1) to 17.2 -65% (quartile 4), and the average change in MA penetration over 7 years ranged from -45.4% – 4.5% (quartile 1) to 16%-35% (quartile 4). Increased Medicare advantage penetration was not associated with any significant decrease in traditional medicare costs. However, the paper was salvaged by analyzing the quartile with the highest baseline level of MA penetration – in this group, an increase of MA penetration by 10% was associated with a decrease of $154.20 in traditional medicare per capita costs. The theory is that you need a certain minimum amount of the market to belong to medicare advantage in order to have significant spillover to the rest of the market.

Of course, Quartile 3 (10-17% baseline penetration) was actually associated with higher costs in traditional medicare and just barely missed being defined as statistically significant in the wrong direction (p = .07 ). So we have one quartile that demonstrated a reduction in cost. The quartile with positive effect had the largest range – from 17.2% – 65%. An analysis within this range would have been interesting, but is not provided. If, for instance, the 35-65% group demonstrated no spillover effect, you would be left with only one range with the association that was sought. Similarly, the authors do not provide data for counties where MA penetration was reduced. Should spillover not apply in reverse? If physicians and providers are so impacted by the ubiquity of medicare advantage plans in their region, should lifting the weight of these plans not unshackle costs?

There are other limitations of the study that relate to contriving causation from observational studies. Perhaps, most importantly, the mechanism of lower cost stays opaque. The authors do meekly suggest that cost moderation may relate to utilization of lower cost providers in the market – and provide as support the higher number of primary care physicians per capita in quartile 4 counties. Of course, there were more total physicians in those counties as well. Unmoved by the strength of this study in isolation I moved on to examine some of the supporting papers cited.

One particular study illustrative of the body of supporting evidence is a study by Kevin Callison , a health care economist, who studied areas of high MA penetration with regards to patients presenting to a hospital with a heart attack. Callison found that high MA penetration was associated with a reduction in both costs and the treatment intensity of Medicare Fee For Service (FFS) patients presenting to hospitals with a heart attack. He came to this conclusion by using Medicare data and some mathematical models :

If this was a paper on climate science, I would have probably stopped reading at this point. I am a cardiologist, and we mostly stick to addition and subtraction, and very rarely indulge in multiplication. In this particular case, since my practice pattern is apparently encompassed in these models, I soldiered on, curious to know what the models said I was doing. The conclusions by Callison were that a 1% increase in MA penetration was associated with a 0.94% reduction in hospital costs for FFS patients. This was apparently due to a reduction in the intensity of hospital services. A 1 % increase in MA penetration resulted in a 2.4% reduction in the probability of a FFS patient receiving a stent. Fewer stents resulted in an increase in mortality of FFS patients by 1.8%. Remarkably, the patients within the MA program had no change in mortality, and the commercially insured patients studied also didn’t have any change in mortality noted. So we are supposed to swallow models which tell us that FFS patients have higher mortality with increasing MA penetration due to spillover, but that patients within MA plans, and commercially insured plans are immune to these effects.

I am also to believe a model that concludes my decision to recommend a stent to a patient having a heart attack is affected by the percent of patients in my region who have medicare advantage plans. Does it matter that my colleagues and I usually have no idea what insurance our patients have when making these decisions? Unfortunately, smug empiricists don’t care – some healthcare strategist some where will shake his head when I say this and cite Callison. Silly cardiologists, they know not what they do.

The mathematical model used here may have a nice heavy, substantive feel to it because of the number of assumptions and variables it contains, but it is unbearably light when it comes to appropriately modeling the reality of practice. I realize I am picking on one paper here. There are many other studies cited as supportive, but almost of them are proofs via the same attempted mathematical modeling of clinical behavior. Paragraphs are written about techniques used to account for unmeasured variables, but at the end of the day these all remain firmly in the category of observational data which generates interesting theories. Consider that there are fewer stress tests and fewer revascularizations being done in this decade compared to the last. This may be related to the larger conversation of cost that animate any number of campaigns-du-jour to do fewer mammograms, fewer PSA tests, and fewer diagnostic imaging. In this context, how can one confidently tease out the possible role of spillover from MA plans? It is entirely possible that the rise of Medicare Advantage plans and Accountable Care Organizations are outgrowths of a cost-conscious era, serving as bystanders in an era of cost-downshifting rather than actual drivers of cost reduction. This observation could be wrong, but to suggest that opposing arguments carry more weight because of observational studies supported by unverifiable mathematical models is a form of earnest chicanery.

Evidence should carry weight when it is weighty. Proposing a theory based on an observed correlation is reasonable. Supporting it with mathematical models is interesting, and the stuff academic tenures are made of. But taking these correlations and unproven, unvalidated mathematical models to then propose fundamental changes to healthcare policy that affects millions is a feat of considerable hubris.

When it comes to MA plans, we know that the federal government pays more per enrollee than traditional medicare. We also know that MA plans then turn around and pay out less per enrollee than traditional medicare. The overpayment by the federal government to MA plans has been a target of the Obama administration, and is a subject of intense political lobbying from insurance companies. It should come as no suprise then, that Marilyn Tavenner, the current head of America’s Health Insurance Plans (AHIP), and the former director of CMS has wasted little time in touting Dr.Jha’s study to support continued overpayments to MA plans. In a high stakes game played between health policy researchers, politicians and insurance plans, I get the sinking feeling patients and the physicians that care for them will end up losers.

Anish Koka is a cardiologist in Philadelphia.

Categories: Uncategorized

Thanks Anish. The thing I wonder about is what would happen if virtually everyone ultimately had a Medicare Advantage plan. As their market share grows, at some point the risk profile of the MA and FFS populations should converge. No?

I suspect but don’t know for sure that there is less fraud in MA plans. The plans also claim that they have significantly fewer hospital inpatient bed days per thousand members. Some of that could be due to a healthier population but some could also be due to better care management through more intensive case management.

Thx paul

I have a post coming on EOL care – I find that to have been relatively inelastic. With the sea change in practice, the one place I haven’t found folks doing much different is in those last months. As to risk adjusted premiums..https://thehealthcareblog.com/blog/2016/01/18/ask-not-what-you-can-do-for-medicare/ scroll down to the section on risk adjustment in MA plans

To what extent have you seen changes in patient driven choices for end of life care over the last five years or so and what effect, if any, has that had on Medicare’s per capita costs regardless of whether patients have FFS Medicare or an MA plan?

As for MA plans, insurers generally target a pretax profit margin of 5% of revenue and they provide some additional benefits as well. If MA plan patients are healthier on average than FFS plan members, shouldn’t that be reflected in the risk-adjusted premium that the insurer is paid for each member?

Very smart very well educated folks torturing data and torturing sound research design to support their preconceptions and cloak it all in pseudo science…..so they can impose their ideas on everyone. It undermines confidence in sound science and rationality.

Thank you for uncloaking the details of how this is being done.

I would commend to everyone Trudy Lieberman’s new Harper’s article “Don’t Touch My Medicare!” Is the beloved program on its last legs?’

http://harpers.org/archive/2016/11/dont-touch-my-medicare/?single=1

Paywalled, but everyone gets one free read.