By MATTHEW HOLT

Given that I ran a health technology conference for many years, I tend to run in a circle of people who have some ambition to get rich in health care. After all, billions of dollars of VC money have been dropped in lots of startups over the last decade, and a few prime examples have done very well. For example Jeff Tangey of Doximity, Glen Tullman of Livongo, Chaim Indig of Phressia and many others did fine when their companies IPOed in the late 2010s. But the truth is that many, many more have either started a health tech business that didn’t make it, or were foot soldiers in others that died along the way (Olive, Babylon, Pear, etc, etc). Which has been leading me lately to thinking about whether that’s the right approach to take if you want to make money in health care. Hint: it’s not.

There’s still tremendously little transparency about which health care organizations have what amount of money and what people earn. There is though one sector that by law has to publish information about revenue, profits, investments and executive compensation. That is the non-profit hospital/health system sector. Nonprofits are required to file Form 990 with the IRS that has that information and more on it. Having said that, most hospitals are frequently late in filing them, and file them in a very confusing way. The wonderful journalism organization ProPublica maintains a database of all 990 filings and it’s instructive to look around in it.

Some health systems make it relatively easy. UPMC, the huge western PA conglomerate files one 990 for the whole group. Others, not so much. I know that Providence, the huge west coast system, has overall revenue of $28bn but only because Fierce Healthcare told me. Had I tried to piece that together from its 990s, I’d have started with its Washington filing ($6bn), moved on to its Oregon filing (~$5bn) and then started getting confused..

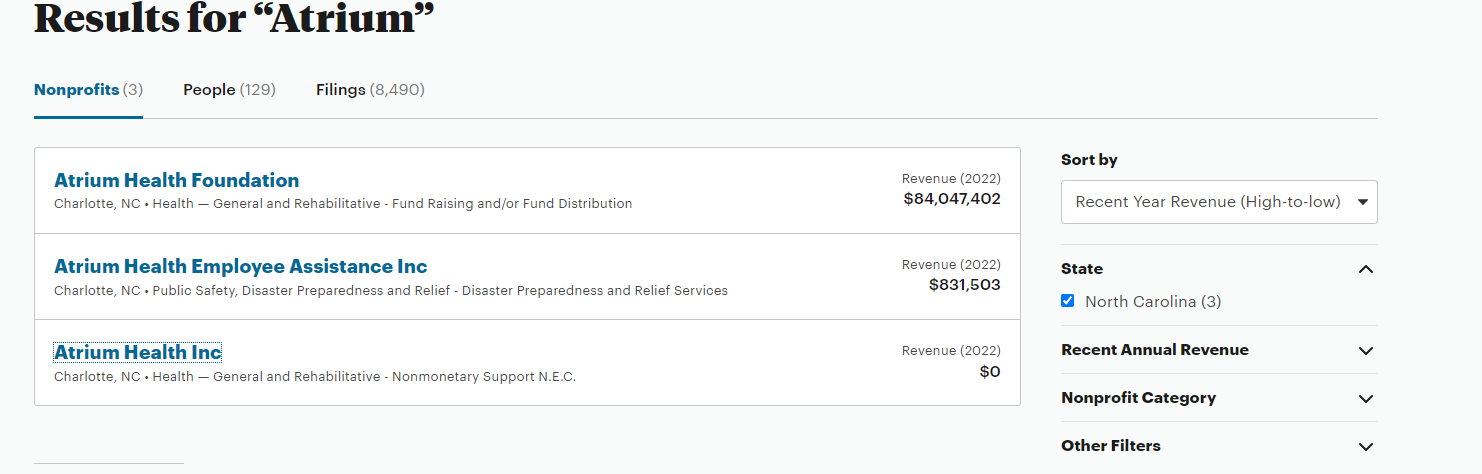

Let’s say you wanted to easily figure out Advocate, the system that was the merger of the huge midwestern system with Atrium, the North Carolina-based one. Good luck. You can find Advocate but Atrium’s seems to be missing. Ditto for Carolinas Health, its previous name. There is a page calling itself Financial Information on the Atrium website, but it doesn’t have any, and tells you to go to a website set up for municipal bondholders. In fact I couldn’t find any evidence of the IRS auditing any large system, or fining them for non-compliance in filing.

The good news is that last year the North Carolina State Employees plan, i.e. a pissed off purchaser, dug into all the N. Carolina hospital systems and found out that Atrium’s CEO pay went up nearly five-fold over six years. But even the state had real trouble finding out the truth:

“It is important to understand that these figures are significant underestimates for three reasons. First, a legal loophole denies the public the right to see how much publicly owned hospitals reported paying their top executives on their tax filings. This failure of oversight hides the tax filings of more than three in 10 nonprofit hospitals in North Carolina, including Atrium and UNC Health. UNC Health did not answer a public records request for executive compensation data until February 13, 2023, two days before this report’s publication and almost three months after its receipt of the request. UNC Health’s system wide data is therefore not included in this report.”

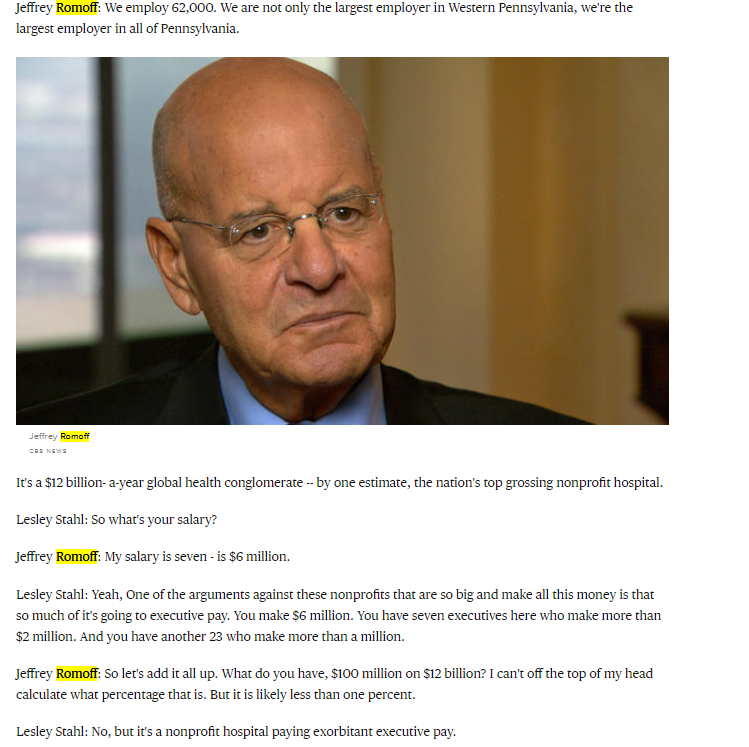

So the very top dogs are doing well. At UPMC it turns out that seven made more than $3m including the CEO Jeff Romoff –the same one who forgot on 60 Minutes whether he made $6m or $7m. Turns out he didn’t have to remember that number for long as by 2021 he was making $12m.

But the munificence is spreading down the executive ladder. To demonstrate, let me introduce you to Tracey Beiriger Esq. There’s almost no information about Tracey on Linkedin or anywhere else on Google other than it appears he or she is an IP lawyer at UPMC. So why do I bring them up?

Because in 2021–the last year for which UPMC filed a 990 –Tracey was the 118th highest paid executive at UPMC and had the misfortune to only make $499,446.

Which means that 117 executives working at UPMC made more than $500,000. It’s a little tricky figuring out the similar numbers at Providence because of the multiple 990s in 2021 but there are 38 in Washington (not including CEO Rod Hochman who made $9m in 2020 and then vanished from the 2021 990!), 18 in Oregon and another 21 in Southern California. So call it 80+.

I bring this up because $500,000 is a pretty decent individual income. When I asked ChatGPT it estimated about 1.2 million Americans earned that much or more. Given the workforce is 167m, that puts those several hundred hospital execs way into the top 1%.

Now I have no objection to people earning good money. I’m sure they have all worked very hard for it. But if you look at these organizations, they do not seem to be spreading the wealth very far.

Last year UPMC was accused by unions of suppressing staff wages. There is yet to be an outcome from that complaint to the DOJ, but last week there was one from a formal class action complaint about Providence shortchanging employees by rounding down their pay to the nearest half-hour, even though they were clocking on and off by the minute. Providence was fined $200m which probably isn’t much split between 33,000 employees but at least indicates that their senior management acts just like any other aggressive business in terms of cutting costs on the backs of their employees. And it’s not just their employees. They also just got fined $137m for aggressively suing patients.

Which leads me to two final points.

The first is, is it more likely you’ll make that $500K+ in a hospital system or in a tech startup? Blake Madden at Hospitology has been tracking systems that have more than $1bn in revenue. He’s found 113 so far. Second bottom of the list is Atlanticare in NJ, which has 16 execs making more than $500K. Which by my wild guess means that the average system has about 50 employees making $500k+ which rounds up to something like 5,000 hospital execs making at least $500K and many of them are making a whole lot more.

Compare that to a successful health tech startup that actually makes it. Take Phreesia, a VC-backed start-up that went public in 2019 having started way back in 2007. (I know the year because CEO Chaim Indig launched at Health 2.0 in 2008. He was nice enough to let me buy some stock at the IPO and I made a few bucks). Chaim made $300K the year it went public and as CEO of a public company that’s bounced around at being worth between $1Bn and $4Bn, he made $750K last year. No one else made more than $500K. Now yes, he owned 4% of the company at the IPO and got awarded more stock. He is doing very well, but the point is that there were dozens of companies launching at Health 2.0 in 2008 and the vast majority don’t get close to an IPO or making any money for the founders, let alone the staff.

My conclusion is, it’s not a rational bet to go the health tech route if instead you can find a regional hospital chain and brown-nose your way up into the exec ranks!

The second point is more fundamental. Remember UPMC and its 117 execs making $500K+? What would a comparable government agency be paying out? I looked at the state of California salaries.There look to be about 50 state employees making more than $500k a year, almost all working for the state investment fund CALPERS. But the top paying one only makes $1.6m a year. I’m not saying that CALPERS should be paying out that much even if it is competing with Wall Street, after all members of the Senate only make $205,000 a year and the state could just put the whole pension into an S&P index fund. But what I am saying is that we should be thinking about paying our big non-profit systems similarly to government employees because they essentially are government employees.

Beckers posted UPMC’s payor mix last year. I highly suspect you’ll find something similar at almost every big system.

- Medicare 48%

- Medicaid 17%

- UPMC as Insurer 11%–(60% of whom are Medicaid/Medicare patients)

- Commercial, Self Pay, Other 24%

More than 70% of the money comes from the government, and the rest from the suckers who have to buy their insurance on the “open market”–which includes those buying via the ACA exchange, receiving government subsidies, and government employees.

So while these huge systems act like Fortune 100 companies and reward their executives accordingly, almost all the money comes from the taxpayer.

I wish I could say we are getting good value for it.

And yes, I didn’t even mention the for-profits and the big insurers, but that will have to wait for another day….

Matthew Holt is the founder & publisher of THCB