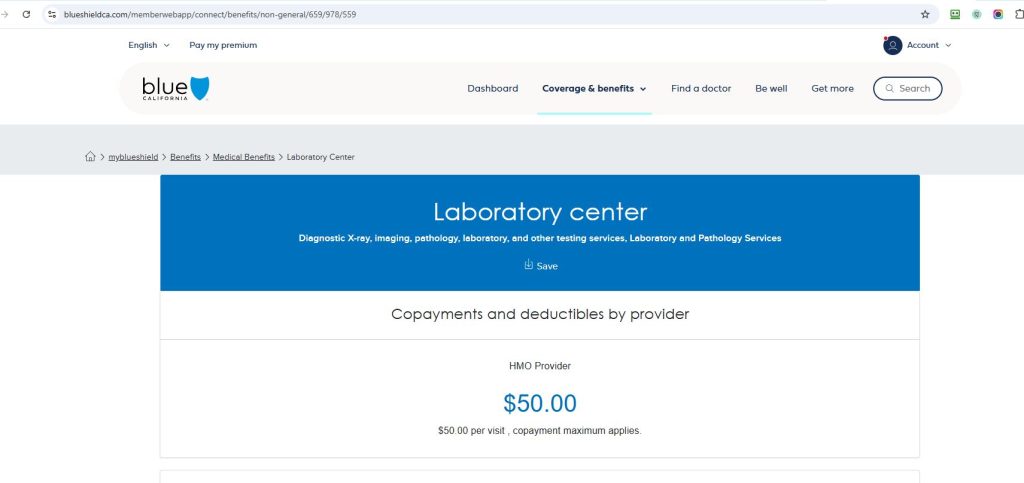

By MATTHEW HOLT

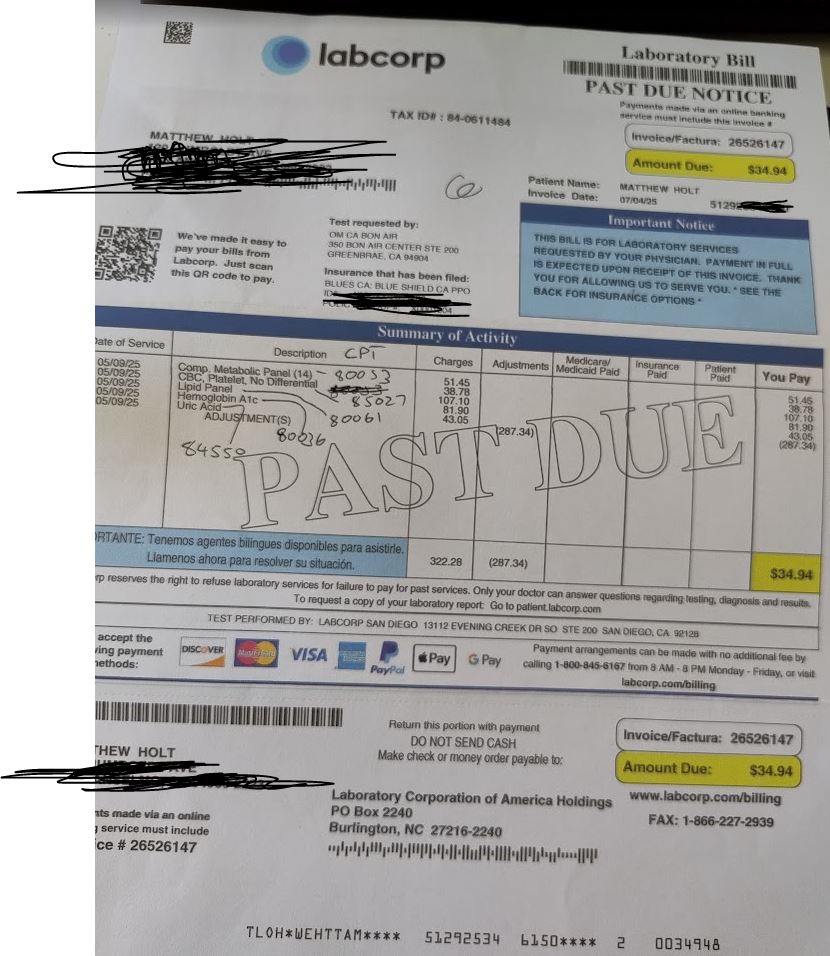

I know my many fans love me delving into the world of why we get seemingly incorrect trivial bills in health care, and what they all mean. The long telenovella of the $39.94 bill from Labcorp is as yet stalled with One Medical apparently resubmitting the original claim with the new preventative codes on it. But even though I am continuing and expanding my role as a difficult patient this year, there are still some blasts from the past that won’t quite leave.

This particular one concerns some rather unpleasant dermatology issues. For many years I had an nasty small sore/lesion on my leg that never quite healed. Then I started getting a few more that started as zits and never quite left. My wise PCP Andrew Diamond at One Medical told me to use some antibiotic wash and referred me to a dermatologist. Unfortunately the one I was referred to was out of network for the Blue Shield HMO I was in, but one request back to One Medical and I was both sent to a dermatologist in my network and got a pre-auth in the mail from Blue Shield to go see him!

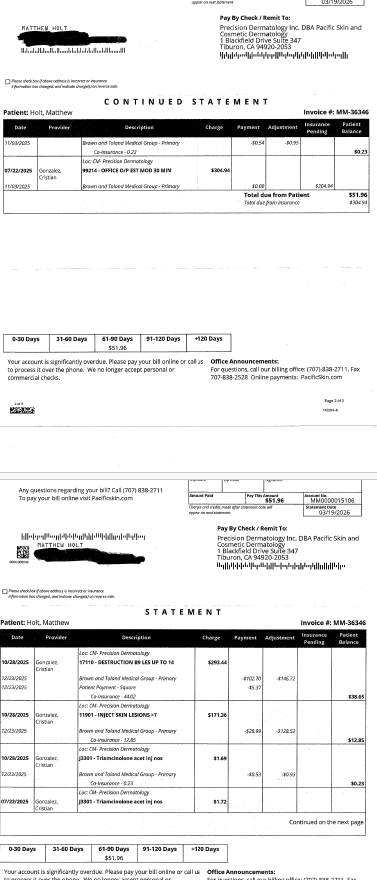

Dr Cristian Gonzalez took a quick look at my leg, decided what the problem was, and proceeded to inject, freeze and attack my various lesions. He then prescribed a cheap topical steroid for me to use, and basically after 4 visits over the summer and Fall, my legs went back to resembling a baby’s bottom–well more or less.

For each specialty visit Blue Shield had a co-pay of $85 per visit, which I handed over using my HSA card. One time the front desk said I had a balance, but when I asked them what it was for they told me it was a mistake. Until this week.

Some 4 months after my last visit I got a bill in the mail for $51.96

Given that I had made a co-pay of $85 each time, this seemed a little odd. So I took a look at my Blue Shield EOBs. (BTW they are back online, you may recall they vanished when Blue Shield cancelled and then changed my plan but the Internet never forgets….)

There a curious anomaly began to play out. Each visit generated three identical claims and three more or less identical EOBs.

Continue reading…