By MATTHEW HOLT

For those of you waiting for the Labcorp, Blue Shield of California, Brown & Toland Physicians Physicians update, the ball has been moved a couple of years down the field.

If you want to catch up here is part 1, part 2 and part 3.

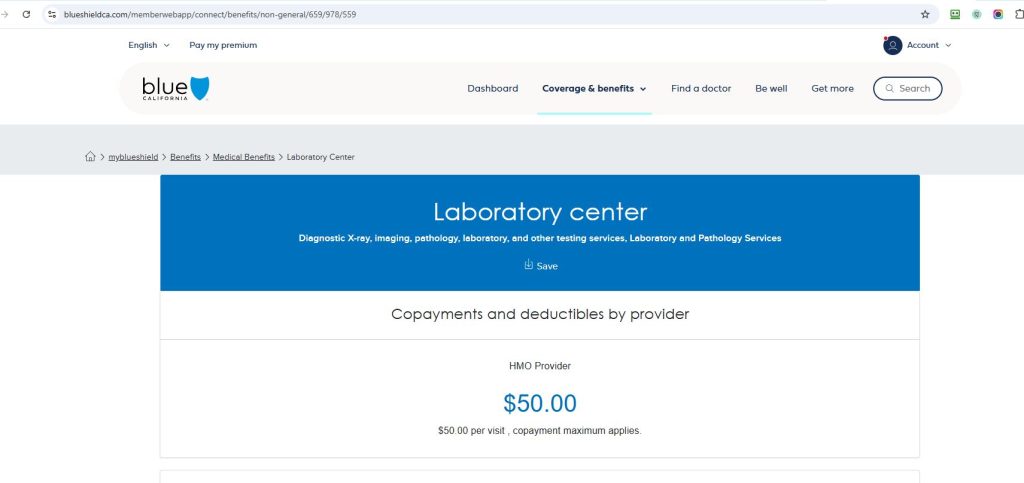

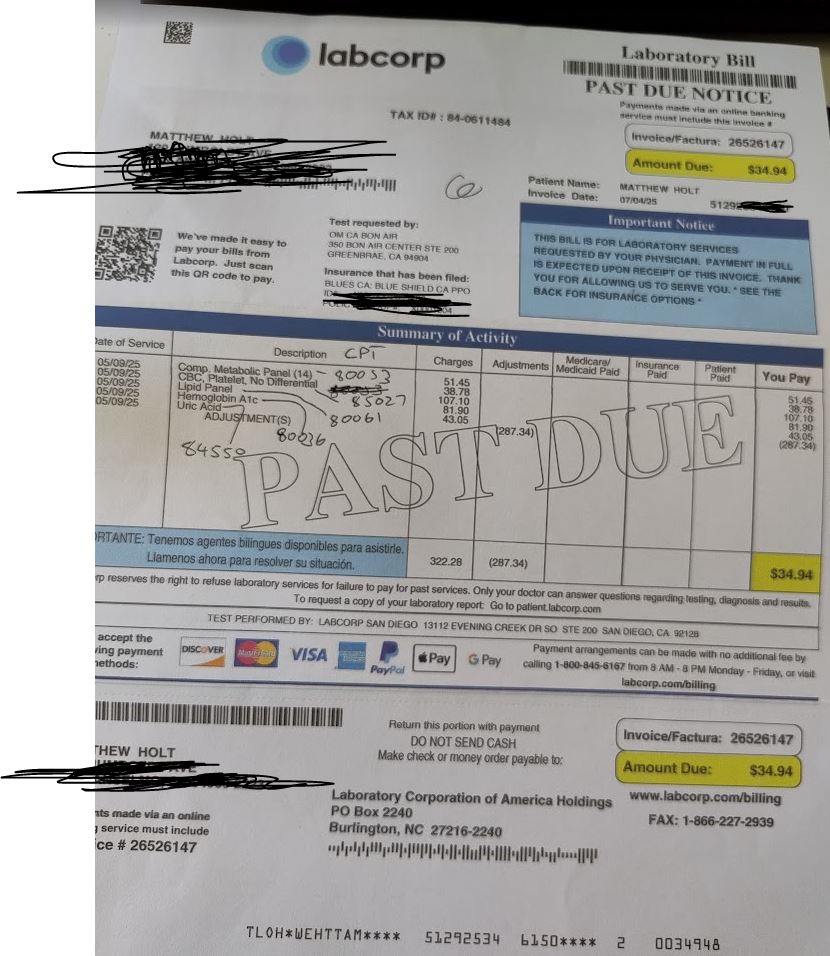

You’ll recall we left it with a mystery $34.94 bill which didn’t either fit the official $50 copay amount I have, nor the $0 patient responsibility in my EOB. I got a call from Rhea Fleming, an experienced customer rep at Labcorp, on whose virtual desk this has been dumped. We had a lovely conversation in which we agreed that the co-pay should either have been $50 or $0 but that it’s possible that the co-pay is the lower of $50 or the amount Labcorp was trying to collect.

She had previously called the Blue Shield of California provider line to try to figure this out. Blue Shield had indeed kicked this claim from Labcorp to Brown and Toland the IPA I am assigned to in the HMO product I bought. The charges from Labcorp were $322.28 and the response from B&T was that the contractual price (i.e. what they agreed to pay Labcorp for those tests) was $34.94, hence the “adjustment” of $287.34. However in Labcorp’s system the algorithm interpreted B&T’s response as saying 1) the agreed payment is the $34.94 according to the contract and 2) they were not going to pay so the patient owes the difference. When Rhea Fleming asked Blue Shield’s rep why the patient owed payment on this, the Blue Shield rep said that the procedure code and diagnosis code from my PCP (One Medical) did not count as preventative care. In other words Labcorp has not got paid at all for running these tests so far, because they are according to B&T “not preventative”. Although IMHO, CMS says that they are. And of course as it says my copay is $0 I’m interpreting Blue Shield of California’s EOB as saying that to me!

Hence Labcorp generated the bill for the $34.94 and sent it to me. Which started this whole telenovela.

BTW Rhea’s conclusion was that as none of the tests were “preventative,” Labcorp billed me the $34.94 as that was the total it was contractually owed rather than the $50 copay I am supposed to pay for lab work. I actually checked back in my Labcorp account and found that last year I did in fact pay $50 so perhaps last year I had different tests or somehow they have changed the algorithm. I checked the EOB for that 2024 bill and the total charge was $445.20 of which Blue Shield paid $28.07. No I couldn’t find the Labcorp bill on their system, presumably because I have paid it! Given that I paid $50 for services from Labcorp on that date (yes, it took me 7 months to pay up!), it’s likely that the agreed payment was $78.07 ($50+$28.07) of which I unthinkingly paid the $50 copay. And yes that should have been preventative too. (Perhaps I should ask for that $50 back!!)

BRIEF UPDATE: Rhea from Labcorp looked into this 2024 bill and that is exactly what happened

Then, I had another thought.

It turns out that the lab results this year generated a further concern in my doctor’s mind. (Bear in mind I had the lab tests before the office visit so that we could discuss the results). It seems that my iron levels were a little low, so while I was in the doctor’s office he ordered some more tests specifically about that. As One Medical has techs on site they drew my blood then and there and shipped it to Labcorp.

According to my EOB, Labcorp’s charge for those new tests was $60.79 of which Blue Shield or rather Brown and Toland again paid $0 and created an EOB which again said my patient responsibility was $0. I asked Rhea to check that bill in her system and it turns out that I do NOT owe Labcorp anything on that set of tests. Maybe they were coded as preventative? I tried to find the bill on my patient portal at Labcorp but because I don’t owe anything I haven’t been sent an invoice and without an invoice number you cannot check the bill!

When Rhea ended the call with me, her next move was going to enquire of Blue Shield and Brown and Toland what the reason was for me owing $0 on that bill!

Meanwhile I await the result of the official Blue Shield investigation with interest. Of course this might just have come down to Amazon One Medical coding the tests incorrectly. But it’s all fun and games if you have unlimited patience in American health care.

And of course, this still isn’t over!

Here’s part 5