In mid-April 2025, UnitedHealth Group (UNH) reported its 1Q25 operating results, including a modest shortfall in expected earnings and lowered its 2025 earnings forecast by 12%. The company blamed accelerating medical costs and federal policy changes for their most profitable service line, Medicare Advantage. Market reaction was swift and savage. UNH stock lost more than 22% in a single day. In May, United fired its CEO, Sir Andrew Witty and withdrew its earnings guidance for 2025, with the stock declining another 15%. Witty was followed out the door two months later by President and CFO John Rex, heir-apparent to longtime Chairman Stephen Hemsley.

Turns out, UNH’s market capitalization trajectory presaged the collapse in UNH’s 2025 cashflow. UNH’s projected cashflow from operations is now expected fall to be half of its 2025 forecast- a breathtaking $16 billion shortfall. In multiple investor calls, the new/old CEO Stephen Hemsley and his new crew have not come remotely close to explaining where the $16 billion went. Struggling UnitedHealth Group is one gigantic smoking black box.

2024 was a nightmare year for the company, beginning with the massive Change Healthcare cyberattack in February and concluding with the brutal killing of their senior health insurance executive, Brian Thompson, in November. It is clear in hindsight that business fundamentals for UNH’s health insurance and care delivery businesses deteriorated sharply during 2024, and its senior leadership were scrambling to repair the damage.

Health insurers across the country are experiencing record operating challenges. However, UNH’s business model enhanced their vulnerability. UNH had spent $118 billion in just five years (2019-2023) buying profitable smaller companies, almost all of which ended up inside of their enormous Optum subsidiary. These acquisitions included: multi-specialty physician groups, ambulatory surgery and urgent care, business intelligence/business process outsourcing and claims management companies.

These businesses are closely intertwined with United’s legacy health insurance business. In order to reach estimated $445 billion in total 2025 UNH revenues, one has to eliminate $165 billion in intercompany revenue flows (Examples- purchases of services by Optum Health from its consulting arm, OptumInsight, or purchase of health services from Optum Health by United Healthcare, UNH’s insurance business).

The company’s nearly fifty year old health insurance business had been a reliable 5.5-6% operating margin generator. However, in 2025, it will produce only a 3% operating margin. However, UNH’s incremental revenues and earnings growth for the past decade have not come from health insurance, but have been produced by Optum, whose revenues were growing much faster than its health insurance business.

Several pieces of Optum have also been far more profitable than United Healthcare itself. Optum Health grew into a $100 billion business (before eliminations), and used to earn an 10% operating margin. In 2025, that margin will be more like 2.5%. Optum Insight, a $19 billion business (before eliminations), which used to earn a sizzling 28% operating margin will be lucky to earn 8% in 2025. The complex interpenetration of Optum and United Healthcare’s businesses makes it impossible to gauge the seriousness of the company’s operating problems.

Optum Health appears to be a major source of the smoke, but it is impossible to tell from the skimpy disclosures where exactly the fire is.

This is Part 2 of Jason and Gigasheets’ investigation into the Capital Women’s Care vs UnitedHealthcare contract dispute in which (partially at my request) he expanded the investigation to look at other providers in the same market. Revealing stuff!–Matthew Holt

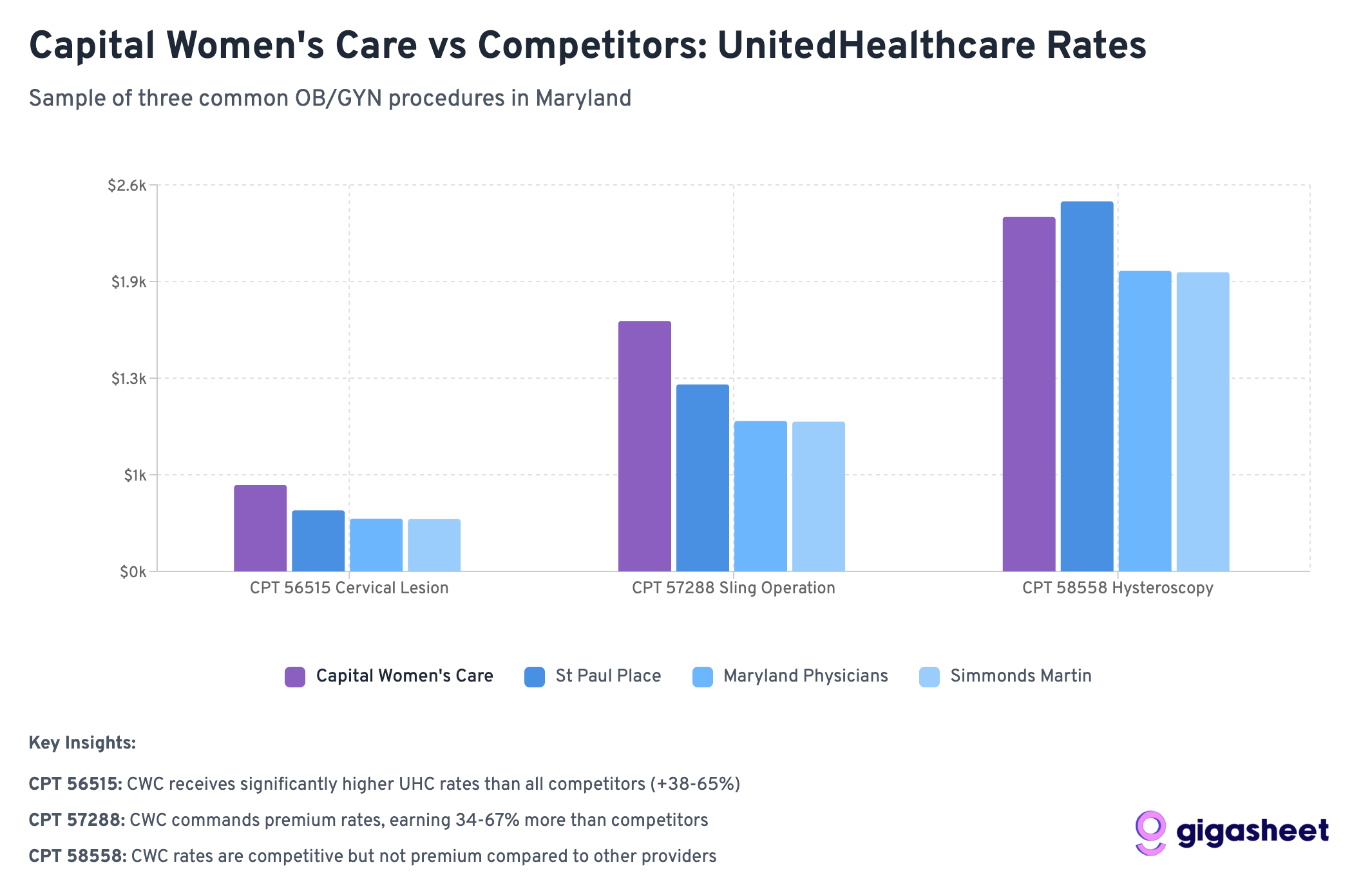

While Capital Women’s Care (CWC) battles UnitedHealthcare over contract terms, a deeper look at Maryland’s OBGYN market reveals a complex competitive landscape where negotiated rates vary dramatically across providers and procedures. By analyzing price transparency data from both UnitedHealthcare and CareFirst BlueCross BlueShield, we can see exactly what each insurer pays CWC’s competitors. The results are eye-opening.

The Players in Maryland’s OBGYN Market

Our analysis focuses on four OBGYN providers in Maryland that have contracts with both UnitedHealthcare and CareFirst. These four practices were selected as a representation of the broader market because they have published rate data with both insurers, allowing for direct comparisons. However, Maryland’s OBGYN landscape includes dozens of additional providers, from solo practitioners to hospital-based practices, each with their own negotiated rates that may follow different patterns.

The four providers in our analysis include:

Capital Women’s Care – The large practice at the center of the UHC dispute, with multiple locations across the region

St Paul Place Specialists (Mercy Medical Center) – Baltimore-based OBGYN practice with established market presence

Maryland Physicians Edge – Women’s health group with OBGYN services, now part of Advantia

Simmonds, Martin & Helmbrecht – Established OBGYN practice, also under the Advantia umbrella

The four-provider sample provides valuable insights into competitive dynamics among major market players and helps contextualize the CWC-UHC dispute within broader industry patterns.

Following our analysis in Part 1, we examined negotiated rates for three common gynecologic procedures:

Code 56515: Destruction of cervical lesion (treatment following abnormal Pap smears)

Code 57288: Sling operation for stress incontinence (surgical procedure)

Code 58558: Hysteroscopy with sampling (diagnostic procedure for abnormal bleeding)

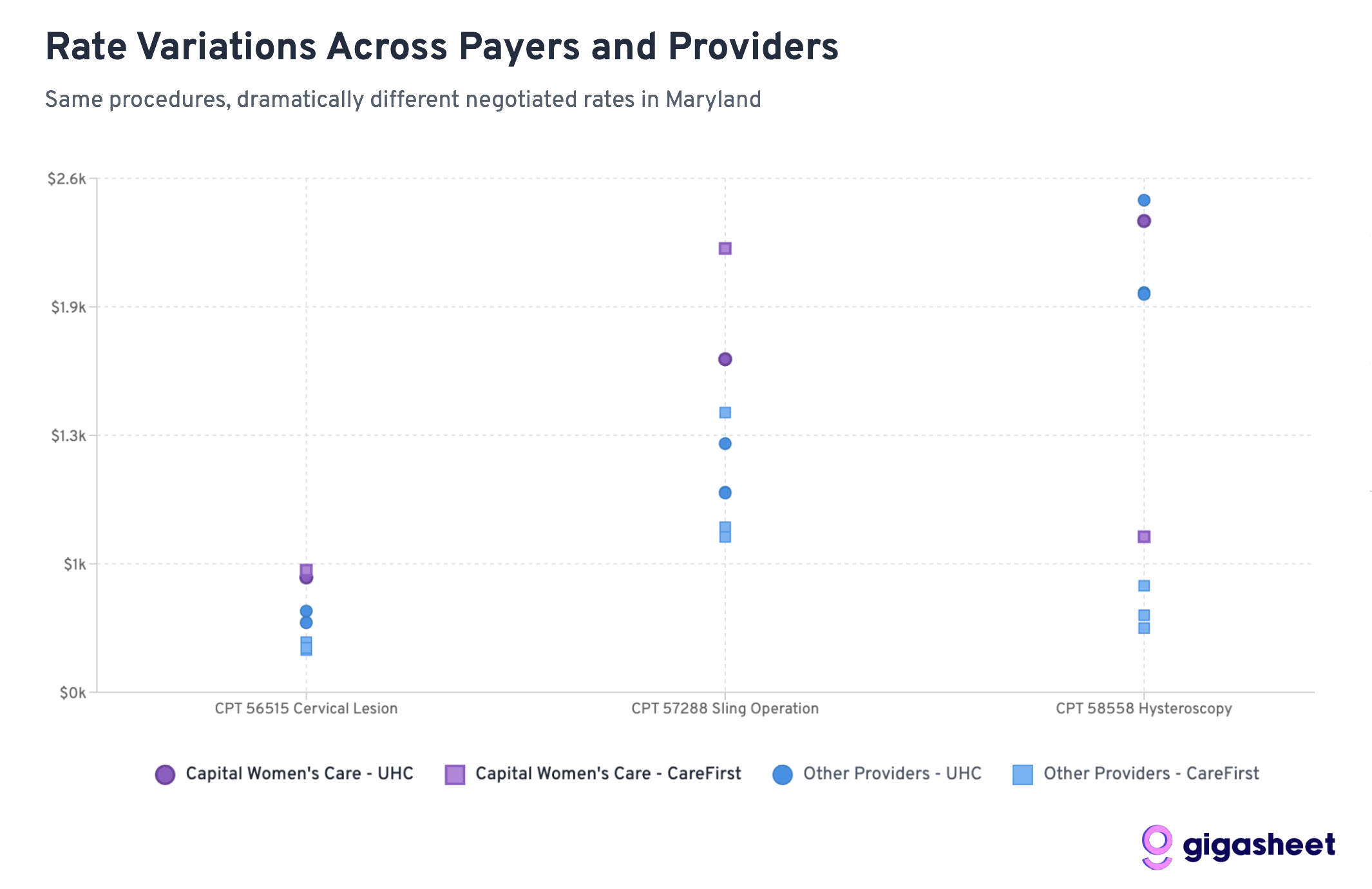

The Rate Comparison: UHC vs CareFirst

Rate variations in the price transparency data reveals a complex competitive landscape where UHC pays 200-500% more than CareFirst for hysteroscopy procedures across all providers in our sample, while Capital Women’s Care shows mixed positioning. Sometimes Capital Women’s Care commands premium rates from UHC (codes 56515, 57288), other times they’re receiving comparable rates to smaller competitors (code 58558). The data suggests both sides in the CWC-UHC dispute have legitimate arguments: CWC already receives competitive or premium compensation, while rate inconsistencies across procedures indicate room for negotiation.

Extreme rate variations (up to 519%) between UHC and CareFirst reveal market complexity, with Capital Women’s Care showing mixed competitive positioning that supports both sides’ arguments in their contract dispute.

Key Findings: A Tale of Two Insurance Strategies

UHC Generally Pays More Than CareFirst

Across 12 provider-procedure combinations, UnitedHealthcare pays higher rates than CareFirst 75% of the time. This suggests CareFirst has been more aggressive in negotiating lower rates across the Maryland market.

Hysteroscopy Shows the Most Dramatic Differences

For Code 58558 (hysteroscopy with sampling), the rate differences are staggering:

UHC pays 203-519% more than CareFirst across all providers

Average UHC rate: ~$2,200 vs CareFirst rate: ~$510

This represents the largest systematic difference across procedures

Capital Women’s Care Commands Premium Rates

CWC’s rates relative to competitors reveal why UHC may be resistant to further increases:

Code 58558: CWC’s UHC rate ($2,384) is already comparable to competitors, despite CWC’s larger scale

Code 56515: CWC gets slightly better terms from UHC ($581) vs competitors ($352-411)

Code 57288: CWC receives significantly higher rates from UHC ($1,685) vs most competitors ($1,008-1,258)

Wide Rate Variations

The most extreme example: Simmonds Martin & Helmbrecht receives 519% more from UHC than CareFirst for hysteroscopy procedures (a difference of nearly $1,700 per procedure). These patterns suggest that while some procedures have established market rates, others (particularly diagnostic procedures like hysteroscopy) lack standardized pricing, contributing to the complexity of provider-insurer negotiations like the CWC-UHC dispute.

Rate variations reveal dramatic pricing inconsistencies across Maryland’s OBGYN market, with hysteroscopy procedures showing the most extreme disparities difference between the highest and lowest negotiated rates for identical services.

What This Means for the CWC-UHC Dispute

CWC Already Commands Premium Rates

The data reveals a key insight: Capital Women’s Care isn’t necessarily getting unfair treatment from UHC. In fact, CWC often receives higher rates than competitors from both insurers:

For hysteroscopy (58558), CWC gets comparable UHC rates despite being a larger practice that should theoretically have less negotiating leverage

For cervical procedures (56515), CWC receives 40-65% higher rates from UHC than smaller competitors

For sling operations (57288), CWC’s UHC rate ($1,685) significantly exceeds most competitors

This pattern suggests UHC’s resistance to further rate increases may be economically rational rather than punitive.

Industry-Wide Rate Fragmentation

The massive variations between UHC and CareFirst rates across all providers highlight fundamental pricing inefficiencies in healthcare. However, within each insurer’s network, CWC consistently commands premium rates, suggesting their market position is already strong.

Scale vs. Negotiating Power

Conventional wisdom suggests larger practices should receive lower per-unit rates due to volume efficiencies. The data shows the opposite: CWC often receives higher rates than smaller competitors, indicating they’ve successfully leveraged their size for premium pricing rather than volume discounts.

The Broader Market Dynamics

CareFirst’s Market Power

CareFirst BlueCross BlueShield appears to have leveraged its position as Maryland’s dominant insurer to negotiate significantly lower rates across the board. With roughly 50% market share in Maryland, CareFirst can drive harder bargains with providers who can’t afford to lose access to half their potential patient base.

UHC’s Perspective Becomes Clearer

UnitedHealthcare’s position in the dispute gains context when viewed against competitor rates. UHC is already paying CWC premium rates compared to other Maryland OBGYN providers. From UHC’s perspective, further rate increases would create an even larger gap between what they pay CWC versus smaller practices.

The Economics of Provider Consolidation

The data illustrates a key tension in healthcare consolidation: large practices argue their size justifies higher rates due to quality and convenience, while insurers worry about paying premium prices for what should be commodity services. CWC appears to have successfully established premium pricing, making UHC’s resistance to further increases economically understandable.

Looking Forward: What This Means for Healthcare Costs

The Price Transparency Revolution

This analysis is only possible because of federal price transparency requirements that took effect in 2021. For the first time, we can see exactly what insurance companies pay different providers for the same services, revealing the massive hidden variations in our healthcare system.

Market Efficiency Questions

The data raises fundamental questions about market efficiency:

Why does the same procedure vary by 500% between insurers at the same provider?

Are patients getting better care when insurers pay more, or are some insurers simply paying inflated rates?

How can patients make informed decisions when rate variations are this extreme?

Regulatory Implications

These findings may attract regulatory attention, particularly around:

Whether rate variations this extreme serve any legitimate purpose

How to ensure patients aren’t penalized for insurance-provider rate disputes

Whether price transparency alone is sufficient to drive market efficiency

Conclusions: Both Sides Have Valid Arguments

The Capital Women’s Care vs UnitedHealthcare contract dispute becomes more nuanced when viewed through competitive rate data. Our analysis reveals that both sides can point to legitimate evidence supporting their positions:

Capital Women’s Care’s Case:

Rate Inconsistencies: For some procedures like hysteroscopy (58558), CWC receives similar UHC rates to much smaller competitors, despite CWC’s larger scale and presumably higher overhead costs.

CareFirst Comparison: CWC’s significantly higher rates from CareFirst for certain procedures (like sling operations at $2,245 vs UHC’s $1,685) suggest room exists for UHC rate increases.

Market Position Justification: As Maryland’s largest OBGYN practice, CWC can argue their scale, convenience, and comprehensive services warrant premium compensation.

UnitedHealthcare’s Case:

Already Premium Rates: Across multiple procedures, CWC receives higher rates from UHC than smaller competitors (40-65% higher for cervical procedures), indicating UHC already recognizes CWC’s value.

Economic Reasonableness: Further rate increases would create an even larger premium gap between CWC and other providers, potentially making UHC’s network economics unsustainable.

Mixed Performance: The inconsistent pattern across procedures suggests CWC’s premium positioning isn’t uniformly justified across all services.

The Complexity of Healthcare Negotiations:

Rather than a clear case of unfair treatment, the data reveals the inherent complexity of healthcare rate negotiations. Both parties can legitimately point to specific procedures and comparisons that support their position, while the overall picture remains genuinely mixed.

This analysis suggests the dispute reflects broader challenges in healthcare pricing: How do you fairly compensate scale and market position while maintaining reasonable cost structures? The competitive data shows there’s no obvious “right” answer; just different ways to interpret the same complex market dynamics.

The real insight isn’t that one side is clearly right, but that healthcare rate negotiations involve legitimate competing interests where reasonable people can look at the same data and reach different conclusions about fair compensation.

Jason Hines is CEO of Gigasheet which delivers AI-powered price transparency market intelligence.. This was first posted on their corporate blog

Note: This analysis is based on a sample of price transparency data filed by UnitedHealthcare and CareFirst BlueCross BlueShield, as mandated by federal regulations. The rate calculations are aggregations of data from multiple contracts and locations within each provider organization. To expand our rate analysis from Part 1, we resolved EINs to organization names using public data sources.

On August 1, 2025, Capital Women’s Care (CWC), one of the largest OB/GYN practices in the Mid-Atlantic region went out-of-network with UnitedHealthcare, affecting tens of thousands of women across Maryland, Virginia, Pennsylvania, and Washington D.C. The contract dispute between Capital Women’s Care (CWC) and UnitedHealthcare offers a fascinating case study in how price transparency data can illuminate the real dynamics behind these high-stakes negotiations.

The Public Battle

Capital Women’s Care, with more than 250 physicians and healthcare professionals, confirmed that its agreement with UnitedHealthcare would lapse despite ongoing negotiations. The practice urged patients to contact UHC to voice their concerns about losing access to their providers.

UnitedHealthcare fired back with detailed public claims on their website, alleging that CWC “refused to move off its demands for double-digit price hikes” and is “significantly higher cost today compared to peer providers throughout Maryland and Virginia”. UHC provided specific examples, claiming that a vaginal delivery from CWC would cost “more than 120% higher – or over $2,600 more – than the average cost of other OB/GYN providers”.

But what does the actual price transparency data reveal about these competing claims?

What the Transparency Data Shows

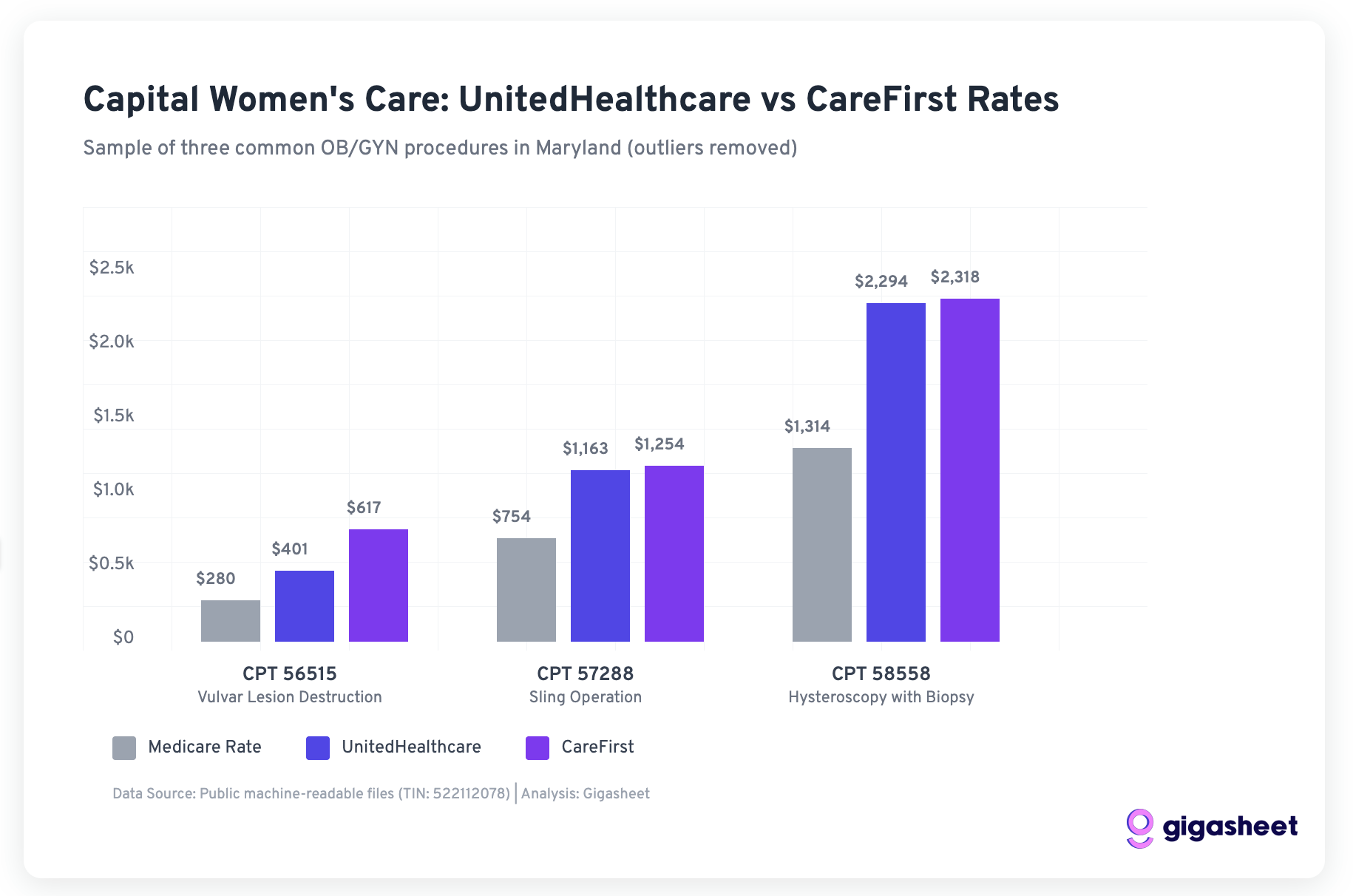

Using Capital Women’s Care’s negotiated rates from UnitedHealthcare’s own machine-readable files, we analyzed a sample of common OB/GYN procedures from Maryland rate data. While this represents only a subset of all procedures and focuses specifically on Maryland rates, it provides valuable insights into the real payment dynamics between these organizations. The data paints a more nuanced picture than either party’s public statements suggest.

Data Methodology Note: Our analysis examined negotiated rates for Capital Women’s Care from publicly available machine-readable files, focusing on Maryland providers and filtering out statistical outliers (rates below 50% or above 500% of Medicare). We analyzed rates for both UnitedHealthcare and CareFirst across three common OB/GYN procedures where both payers had sufficient data.

CWC’s Rate Position vs Other Payers

Our analysis of three common OB/GYN procedures in Maryland reveals that CWC’s rates with UnitedHealthcare were actually quite competitive compared to other major payers:

Negotiated rates for three common OB/GYN procedures show UHC was paying competitive rates compared to CareFirst

For the three procedures where both UHC and CareFirst have negotiated rates with CWC:

This sample data suggests UnitedHealthcare was already getting favorable rates from CWC compared to other major payers, calling into question UHC’s claims about CWC being “significantly higher cost.”

The Medicare Benchmark Reality

Both UHC and CareFirst were paying CWC rates well above Medicare in our sample:

UnitedHealthcare: 143-175% of Medicare rates

CareFirst: 166-220% of Medicare rates

While CareFirst paid higher rates, UnitedHealthcare’s rates were still substantial premiums over government reimbursement, suggesting the “double-digit increases” CWC requested may have been attempts to align with market rates other payers were willing to pay.

The murder of UnitedHealthcare CEO Brian Thompson has drawn attention to Americans’ frustration with the for profit healthcare insurance industry. Change is possible but less likely if people don’t understand how we got here, the real issues, and how they might be fixed.

Health insurance wasn’t always run by big for profit corporations

According to Elizabeth Rosenthal’s book, An American Sickness (a must read), it all started in the 1920s when the Vice President of Baylor University Medical Center discovered that they were carrying a large number of unpaid bills. The goal wasn’t to make money. It was to keep sick people from going bankrupt while helping keep the lights on at not-for-profit hospitals.

Baylor launched “Blue Cross” as a not-for-profit and it offered one-size-fits-all coverage, one-size-fits-all pricing, and all were welcome. By 1939, Blue Cross grew to 3 million subscribers and health insurance might have stayed this way if it wasn’t for two important innovations that would change healthcare and insurance as we know it.

Before the late 1930s, there wasn’t a heck of a lot we could do for sick people. That all changed with two innovations: 1) the ventilator and 2) the first intravenous anesthetic. The ability to put people to sleep and keep them breathing opened the door to a whole array of new surgical and intensive care interventions. More interventions meant more lives saved. It also meant longer hospital stays, more expensive equipment and care. Insurance would have to evolve to keep up with medical innovation.

We probably could have solved that problem with direct-to-consumer private insurance (like car or life insurance). But World War 2 introduced a creative workaround to a labor shortage that gave employers an outsized role in determining our health.

Health insurance tied to employment

During World War 2, the National War Labor Board froze salaries and companies faced labor shortages. Employers figured out they could attract employees by offering health insurance. The government encourages this by giving a tax break to employers on health insurance spending.

The number of Americans with health insurance skyrockets. Between 1940 and 1955, this number increased from 10% to over 60%, with the not-for-profit Blue Cross dominating. It’s hard to believe nowadays, but at the time, an insurance company was one of the most beloved brands in America.

The New York Times had an interesting profile this weekend about how Goodwill Industries is trying to revamp its online presence – transitioning from its legacy ShopGoodwill.com to a new platform GoodwillFinds — in the amidst of numerous other online resellers. It zeroed in on the key distinction Goodwill has:

But Goodwill isn’t doing this just because it wants to move into the 21st century. More than 130,000 people work across the organization, while two million people received assistance last year through its programs, which include career navigation and skills training. Those opportunities are funded through the sales of donated items.

Moreover, the article continued: “Last year, Goodwill helped nearly 180,000 people through its job services.”

In case you weren’t aware, Goodwill has long had a mission of hiring people who otherwise face barriers to employment, such as veterans, those who lack job experience or educational qualifications, or have handicaps. As it says in its mission statement, it “works to enhance the dignity and quality of life of individuals and families by strengthening communities, eliminating barriers to opportunity, and helping people in need reach their full potential through learning and the power of work.”

As PYMNTSwrote earlier this month: “Every purchase made through GoodwillFinds initiates a chain reaction, providing job training, resume assistance, financial education, and essential services to individuals in need within the community where the item was contributed.”

I want healthcare to have that kind of commitment to patients.

Healthcare claims to be all about patients. You won’t find many that openly talk about profits or return on equity. Reading mission statements of healthcare organizations yield the kinds of pronouncements one might expect. A not-entirely random sample:

Cleveland Clinic: “to be the best place for care anywhere and the best place to work in healthcare.”

Imagine a government program where private contractors boost their bottom line by secretly mining participants’ personal information, such as credit reports, shopping habits and even website logins.

It’s called Medicare.

This is open enrollment season, when 64 million elderly and disabled Americans choose between traditional fee-for-service Medicare and private Medicare Advantage (MA) health plans. MA membership is soaring; within a few years it’s expected to encompass the majority of beneficiaries. That popularity is due in no small part to the extra benefits plans can provide to promote good health, ranging from gym membership and eyeglasses to meal delivery and transportation assistance.

There is, however, an unspoken price for these enhancements that’s being paid not in dollars but in privacy. To better target outreach, some plans are routinely accessing sophisticated analytics that draw upon what’s euphemistically labeled “consumer data.” One vendor boasts of having up to 5,000 “certified variables for every adult in America,” including “clinical, social, economic, behavioral and environmental data.”

Yet while companies like Facebook and Google have faced intense scrutiny, health care firms have remained largely under the radar. The ethical issue is obvious. Since none of this sensitive personal information is covered by the privacy and disclosure rules protecting actual medical data, it is being deliberately used without disclosure to, or explicit consent by, consumers. That’s simply wrong.

But a more fundamental concern involves the analyses themselves.

Lost in the weeds of President Obama’s budget proposal is a 10-year, $11 billion reduction in Medicare funding for graduate medical education (GME). GME is the “residency” part of medical training, in which medical school graduates (newly minted MDs and DOs) spend 3-7 years learning the ropes of their specialties in teaching hospitals across the country.

Medicare currently spends almost $10 billion annually on GME. One-third of that is for “Direct Medical Education” (DME), which pays teaching hospitals so that they in turn can provide salaries and benefits to residents (current salaries average around $50,000/year, regardless of specialty; there are variances by region). No problem there.

The proposed cuts come from the Medicare portion known as “Indirect Medical Education” (IME) payments. Though IME accounts for two-thirds of the Medicare GME pie, it’s not easy for hospitals to itemize what exactly it is they provide for this significant amount of funding. Instead, hospitals bill Medicare based on a complex algorithm that includes the ‘resident-to-bed’ ratio, among other variables.

A 2009 Rand Corporation study commissioned by Medicare to evaluate aspects of residency training called on the government to tie IME payments directly to improvements in educational and hospital quality, lest the money be perceived to be going down a series of non-specific sinkholes. That idea has caught on, and legislators in both parties now see the healthy IME slice of Medicare education funding as a plum target for cost-cutting, as the direct benefits are difficult to enumerate, let alone quantify.

This has medical educators very worried that we will have to do more with much less (disclosure: I am one).